The U.S. Federal Reserve, European Central Bank, and central banks of Canada, England, Japan, and Switzerland today announced a coordinated monetary action that could provide added assistance to interbank lending in the event of a further deterioration in global financial markets. Here I offer some thoughts on what the action signifies.

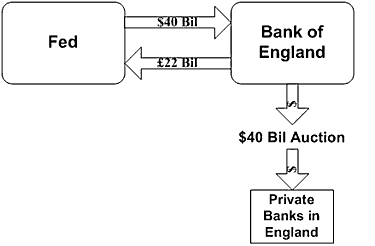

First, a little background. U.S. monetary policy has gone through two distinct phases in trying to deal with the economic and financial challenges since 2008. The first phase was intended to address the breakdown of what in normal times were very liquid markets for short-term interbank loans or commercial paper. One of the tools that the Fed used for this purpose was the Term Auction Facility, which was created in December 2007 to provide an additional channel for U.S. banks to borrow from the Fed. The Fed lent almost $500 billion through the TAF in March of 2009, but the TAF has not been used since April 2010. Another emergency tool was the Commercial Paper Lending Facility, which began operations in October 2008 and lent as much as $350 billion in January 2009 before being closed in February 2010. A third tool used during the height of the crisis was currency swap agreements. As an example of how these work, the Federal Reserve might give the Bank of England 40 billion dollars in exchange for 22 billion pounds, with an agreement to swap the currencies back at some future agreed date. In the mean time, the Bank of England could use the funds to extend dollar-denominated loans to banks in the U.K. This might help ease some of the pressure on the interbank Eurodollar lending rates as reflected for example in high term LIBOR rates.

Source: Macroblog

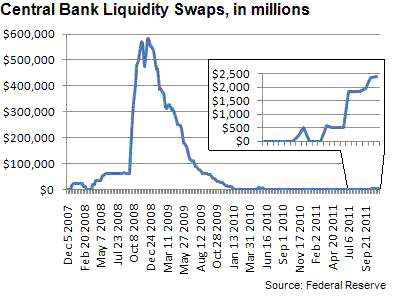

The Federal Reserve’s holdings of currency swaps reached almost $600 billion in December 2008, though since January 2010 have been less than a few billion.

Source: WSJ

Measures like the Term Auction Facility, Commercial Paper Lending Facility, and currency swaps were phased out because liquidity returned to these markets and the facilities were no longer needed. Over the last two years, the Fed has instead been in a second phase of actions, purchasing huge volumes of mortgage-backed securities and longer term Treasury securities in an effort to keep longer term interest rates low.

The Fed’s announcement today indicates a renewed concern that financial conditions could again deteriorate and measures like those used in the fall of 2008 could again be needed. The basic concern is that losses on sovereign debt loans could put banks in jeopardy, and uncertainty about the situation could significantly disrupt financial markets. The TED spread, which measures the difference between the yield on 3-month interbank loans of Eurodollars and the U.S. T-bill rate, has been climbing back up, though it is still far below values seen in 2008. Currency swap operations like the one described in the schematic above could be used to respond to further pressures on this spread.

But, as I mentioned last weekend, even more dramatic are the spreads on term interbank loans denominated in euros. Thus there is a new feature to the coordinated central bank measures announced today:

As a contingency measure, these central banks have also agreed to establish temporary bilateral liquidity swap arrangements so that liquidity can be provided in each jurisdiction in any of their currencies should market conditions so warrant. At present, there is no need to offer liquidity in non-domestic currencies other than the U.S. dollar, but the central banks judge it prudent to make the necessary arrangements so that liquidity support operations could be put into place quickly should the need arise.

An accompanying document from the Federal Reserve adds these details:

These swap lines are being implemented as a contingency measure, so that central banks can offer liquidity in foreign currencies if market conditions warrant such actions. These lines provide the Federal Reserve with the same ability to provide foreign currency, should the need arise, as foreign central banks currently have through the existing dollar swap lines with the Federal Reserve to provide dollar liquidity in their jurisdictions….

There has not been a decision to activate the foreign currency liquidity facilities. If the Federal Reserve were to decide to offer liquidity in foreign currencies to U.S. financial institutions, the details of the operations would be determined at that time in light of the prevailing circumstances.

If the Fed decides to open a new Term Auction Facility, this time for extending euro-denominated loans to U.S. banks, it will once again find itself needing to distinguish between the problems of solvency and liquidity. No action by a central bank can solve the problem of a debt that’s not going to be repaid. But central banks can help avoid the added economic damage that is caused when markets for all loans, good or bad, get disrupted by the uncertainty. In the fall of 2008, the Fed successfully figured out how to navigate that fine line. Let’s hope they have the wisdom to do so this time as well.

Or better yet, let’s hope the new facilities don’t need to be used at all.

Leave a Reply