It is hard to find much optimism by looking at the Italian economy today: Low growth, high government debt, limited confidence of financial markets and no government. Pick a random newspaper or economics blog today and the tone will be on a range from mildly pessimistic to catastrophic. I will not repeat their arguments and instead I will do my best to be a contrarian and argue that maybe it is not as bad as it looks. Or maybe it is, but Italy has managed to live with such a bad situation for years so there is some hope. This might not be enough to turn you into an optimistic but at least it provides a perspective to how similar episodes ended.

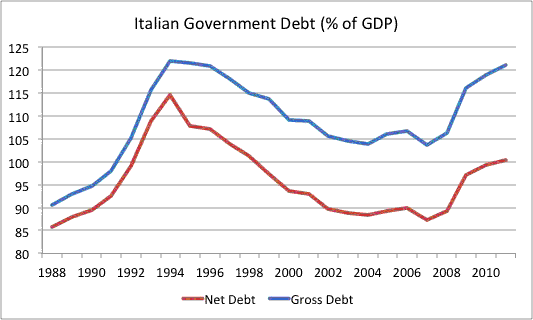

Below is the Italian government debt expressed as % of GDP. There are two lines, the gross and net values of government debt. Net debt is a more appropriate measure as it takes into account some of the financial assets that the Italian government owns and it is equivalent to what is referred to in the US as “government debt held by the public”. I include gross debt as well because the “net” measure is noisy and some times unreliable so some prefer to focus on gross debt.

When we look at gross debt we see that Italy is now back to where it was in 1994. If we focus on net debt the current level of debt is significantly below what it was in 1994. So Italy has seen similar or higher levels of debt before.

We can then argue that those times were different, that Italy had its own currency (although it was heading towards the Euro) and that a combination of high inflation and fast growth allowed them to stabilize that high level of debt.

Certainly it was not growth what saved them. GDP growth in Italy has been low during this period of time: the average growth rate for the period 1994-2007 was 1.6%, clearly below the growth in other Euro countries (France grew at 2.6% and Spain at 3.6% during the same period of time).

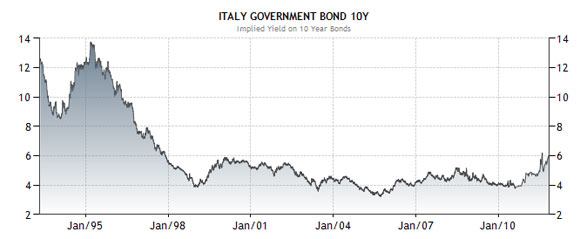

What about interest rates? Maybe the government of Italy did not face the high interest rates that they face today? Below is a chart of the 10-year interest rate for Italian government bonds.

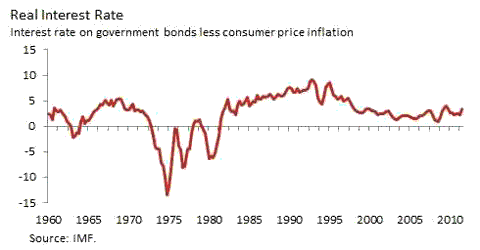

As it is clear from the chart, financial conditions back in 1994-1995 were extremely difficult for the Italian government with nominal interest rates as high as 12%. Much higher than the current levels of 6-7% that look as unsustainable. Of course, what matters is not nominal rates but real rates (what really matters is the difference between interest rates and growth but I do not have that chart ready in my computer). Below is a chart with real rates that confirms that interest rates today remain low compared to the ones faced by Italy in 1994-95.

Here is what I learn from the previous three charts. To my surprise, and the surprise of many, Italy has managed to sustain a very high level of debt even when facing high interest rates by generating large enough primary surpluses. And it has done so with a political environment that has been volatile and in some cases driven by very poor choices. Does it mean that they can keep going like this forever? No, there might be a sense of fatigue and maybe the end of what it looks like an unstable model. But, at the same time, it is interesting to see when we look back at history that a similar episode did not automatically lead to default even with poor economic policy choices. And if you want to be even more optimistic, there is some hope that this crisis is not wasted and the future Italian government finds an even better way to manage a very difficult situation.

Leave a Reply