Rick Perry teed this up. I’m amazed at how much traction this has gotten. Clearly both sides of this issue are stirring the pot.

I’ve looked up a few definitions of what a Ponzi scheme is. This one is from an excellent source. The Securities and Exchange Commission defines a Ponzi as:

A Ponzi scheme is an investment fraud that involves the payment of purported returns to existing investors from funds contributed by new investors.

Does Social Security constitute a Ponzi based on that definition? I think it does.

There are two ways to look at this:

I) If there are no changes in the current laws regarding Social Security does the projected future financial results support the conclusion that it is a Ponzi?

II) If changes are made to Social Security will the consequence of those changes result in the conclusion that it is still a Ponzi?

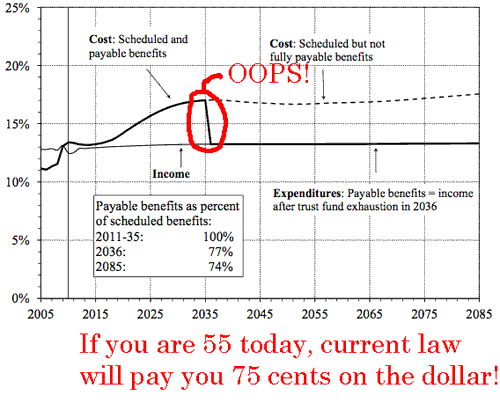

(I) is easy to answer. Based on the SEC definition, Social Security is a Ponzi. If you want proof of that go to the Social Security Trust Fund May 2011 report to Congress. On page 10 (of the report) you find the following chart. Somewhere around 2036 (I think much sooner) SS benefits will be cut by 25%. That is the law as it is written today.

Conclusion: Anyone under 45 today is paying for something that they should expect to get 75 cent on the dollar. Clearly a Ponzi.

To answer (II) requires that one make some assumptions regarding what changes to SS are coming. I rely on the recommendations from a variety of sources. Both Republicans and Democrats (including the President) have supported the recommendations made by the Fiscal Commission report. SS has it’s own set of recommendations. “Independent” private groups have made their thoughts public. While it is not clear what (if any) changes are coming at SS, the following covers the options that are being given serious consideration:

1) Gradually raise the age limit to 70.

2) Gradually increase FICA taxes.

3) Change the formula that indexes SS benefits to inflation. The consequence would be to slow the current projected growth rate of SS payouts.

4) Gradually increase the cap on incomes subject to FICA. (Currently $106,500).

Of all of these options the one that has had the most support is to gradually increase the age limit to 70. What does that do for SS on the charge that it is a Ponzi?

Assume I am 65 and getting $2,000 a month from SS. On paper I should die at age 77. By the numbers I will get 12 years of benefits.

Now assume that the age limit is extended to 70. Assume further that this will be effective is 15 years. Based on what we know today the average life expectancy of a 65 year old male will be 13 years in 2026.

This means that a person who reaches age 65 in 2026 will not get benefits for another 5 years (70). That same person will die at age 78. They will get benefits for only 8 years while I get mine for 12. I will get benefits for 50% longer than they do.

Conclusion: Anyone who is under 50 today is getting screwed when that age limit goes up. For those folks, SS meets the definition of a Ponzi.

Raising FICA makes things worse. Not only would younger workers pay more into the system as a % of their income, they will get benefits for a shorter period of time.They pay more for less when taxes are raised

Conclusion: Increasing FICA taxes is a solution that forces the conclusion that a Ponzi is afoot.

Changing the COLA formula has lots of support from the “deep thinkers”. I agree that if this were done it would have a very significant consequence to SS over a 30-40 year period.

The desired effect is to reduce the inflation adjusted cost of benefits. I get $2,000 a month. We know what that buys today. In 30 years a retiree will get $4,000 a month, but because of the changes to COLA that $4,000 will have a purchasing power equal to only $1,000 today. This is the objective of the proposed changes.

Conclusion: Changing the COLA formula devalues future benefits versus those receiving them today. Anyone under 40 is going to feel the full brunt of this. For them, SS is a Ponzi.

Increasing the wage cap is just another way of increasing the current tax burden on workers. Yes, this increase will be targeted to those who make a decent buck, so this is a popular approach. The consequences will be felt by about 10% of all workers.

Conclusion: For those in this group the consequences of #’s 1,2 and 3 are just magnified. I don’t feel sorry for those high-income earners but it’s certain that this group is facing the biggest Ponzi of them all.

SS is, and always will be, an inter-generational transfer of wealth. By itself that does not have to mean it is a Ponzi. If the total population were symmetrical across all age groups the inter-generational impact would be both fair and reasonable. But that is not what we have in America today. We have a stable population that is rapidly aging. Given that dynamic anyone who is under 55 (and especially those who aspire for a high lifetime income) are going to get hit with the biggest inter-generational wealth transfer in history. For all in that group, SS is a Ponzi. They will pay in more than they get back. The extent that each age group is impacted varies. Those who are not yet born are the ones who will feel this the most.

I’m not sure if Rick Perry is crazy or just crazy smart. There are 50 odd million Americans who are getting SS checks. That’s a hell of a lot of voters. That’s why SS is called the third rail.

But if Perry asked himself, “How do I win this election?” He could well answer with a strategy that relied on young people who would cheer/support him. He could also look to all those swing voters under 55 who pay a fortune in SS and will not get their fair share back. It’s an odd political alliance. But it just might work. Mr. Romney seems to be doing well with the seniors. But he falls flat when he gets to a campus. The base that Perry is chasing after is the same one that got Obama elected.

Note: In my definition of a Ponzi there has to be intent to defraud. I’m not sure that this condition has been met. Every year for the past five the SS Trust Fund has told Congress that significant changes must be immediately implemented. SSA has not mislead anyone, so no fraud from them. The deciders who looked at these reports and chose to ignore what has been written are probably not guilty of fraud either. But they sure were remiss in their responsibilities.

Leave a Reply