Solar stocks have been a terrible investment over the past few years. Some of the big public names have been hammered.

FSLR – First Solar = -65%

LDK – LDK Solar = -88%

ESLR – Evergreen Solar = -100%

SPWR – SunPower = -88%

Bloomberg had a story today on this. The bottom line:

The solar-equipment industry is beginning a consolidation that’s already the biggest in at least two years as plunging prices for photovoltaic systems force weaker companies to team with competitors or close shop.

From personal involvement I can add a bit of “color” to the story. Both China Inc. and Euro Inc. solar panel manufactures are willing to provide 100% of the financing (including “soft” costs) for a viable project. What better evidence could you find that there is a very big imbalance of supply and demand?

The fundamental issue is that solar panels are a low tech. commodity product. It’s very difficult to make a buck when that is the case.

These points all lead me to wonder about a big company in this space, Solyndra. This is a private company. I don’t have any financials to look at as a result. Neither do you. But you should, this company is heavily indebted to Uncle Sam.

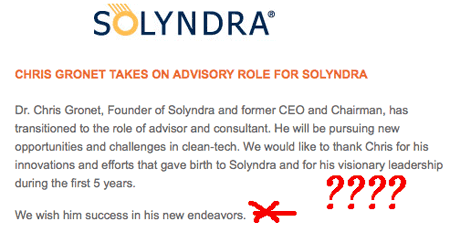

There was a big announcement at Solyndra the other day. I think that this is a sign of some problems. This from August 19th:

Mr. Gronet was the CEO and Chairman of Solyndra. He was also the founder. He is Ex AMD. When he left in 2005 he had money in his pocket. That (and some VC money) was the capital that got Solyndra going.

It sure strikes me odd that he would be leaving right now. There has been no replacement named. That strikes me odd too.

As I said, there are no current numbers to look at. Solyndra tried to go public back in June 2010. There was a “Red Herring” stock prospectus that was circulated. There was no interest in the deal so it got pulled (“Unfavorable market conditions” was the excuse given) The SEC registration statement (S-1) for the proposed deal was also pulled from the public.

What was in the prospectus wass, no doubt, the real reason that investor chose to take a ‘pass’ on the deal. There were revenue/expense numbers for the nine months preceding the proposed deal:

Revenue: $58.8mm

Cost of Goods Sold: $108.0mm

That is an absolute complete disaster. This is a low margin business to begin with. At Solyndra they were losing 84 cents for every dollar of sales. Adding in SG&A and CapEx the losses and cash drain had to be very heavy.

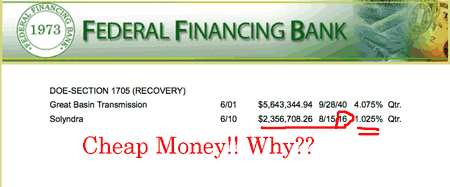

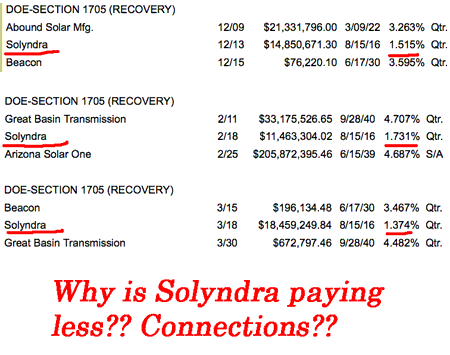

Of course, that’s just me guessing. I repeat, there are no numbers on this company. And that is the crux of the problem. There should be numbers available to the public. After all, the company has been financed by the Department of Energy for years. To make it worse, the funding has come from the Treasury Department’s own private bank. The Federal Financing Bank. Solyndra’s out-standings with the FFB/DOE as of July totaled $530 million. The rates for these advances are clearly subsidized. Consider the interest rate on this $2.5mm loan.

The pattern of subsidized financing is also clear from the FFB reports from January through June 2011.

You would think that with all this money and all these question marks someone in D.C. would be looking into all of this. There actually has been an effort to uncover some facts. But it went no place at all.

On June 27th the House Energy and Commerce Committee held a hearing. On top of the agenda was Solyndra. Jeffrey Zients (Office of Management and Budget Deputy Director) failed to show for the hearing to discuss OMB’s role in the Solyndra DOE Loan Guarantee process. He sent a letter saying he had a scheduling conflict. A scheduling conflict? Give me a break!

On June 27th the House Energy and Commerce Committee held a hearing. On top of the agenda was Solyndra. Jeffrey Zients (Office of Management and Budget Deputy Director) failed to show for the hearing to discuss OMB’s role in the Solyndra DOE Loan Guarantee process. He sent a letter saying he had a scheduling conflict. A scheduling conflict? Give me a break!

Of note were the comments by the Chair of the committee, Cliff Stevens (R-Fla) who said that if the OMB refuses to comply in the coming weeks he would issue a subpoena to force disclosure. While I’m not holding my breath for this to happen, a showdown on Solyndra is coming. Keep in mind that the Boss/Owner (Pictured with O) just took a powder a few days ago.

Side Notes:

The loan guarantee, the administration’s first for a clean energy project, benefited a company whose prime financial backers include Oklahoma oil billionaire George Kaiser, a “bundler” of campaign donations. Kaiser raised at least $50,000 for the president’s 2008 election effort.

In one of those “twist of fates” you hear about; back in April of 2008 Senator Hillary Clinton exposed the Kaiser/Obama connection while she was battling the big O in the Arizona primary. Obama was running an ad that said:

“I don’t take money from oil companies or Washington lobbyists”

The Clinton campaign made a big deal of this and pointed squarely at George Kaiser and the fact that he was raising big bucks for O’s campaign.

Solyndra told their employees this AM that they are declaring bankruptcy, ch 11.

What is the heading for the fourth column? If it is the due date for the loan, then it makes sense that a 5yr loan has a lower interest rate than 30yrs.