I was in Washington DC last week, arriving right after the earthquake and getting out of town just before Irene, to attend a conference on commodity markets at the Commodity Futures Trading Commission. Here are some of the remarks I made at the conference on the role of speculation and fundamentals in recent oil price movements.

Solid line: Price of West Texas Intermediate using near-month NYMEX futures price in dollars per barrel (left scale). Dashed line: Long positions in oil futures contracts of commodity index funds as inferred using the methodology of Masters (2008) (in numbers of contracts or equivalently thousands of barrels, right scale). Source: Singleton (2011).

The diagram above displays the relation between crude oil prices (solid line) and one estimate (dashed line) of the total number of crude oil futures contracts held by funds that are trying to replicate the Goldman Sachs Commodity Index or the separate Dow Jones-AIG index. One of the issues discussed at the conference was some of the problems associated with these estimates of commodity index fund investments.

But a separate issue I wanted to raise is that someone following such an investment strategy was buying not just crude oil contracts, but a variety of other commodity futures as well. For example, a fund following either index would have a long position in natural gas futures. The graph below compares the price of crude oil with the price of natural gas. Although these once sold for about the same price per Btu, they now differ by a factor of 4. Why hasn’t index fund buying pushed up the price of natural gas along with crude oil? The answer is obvious to all of us. The surge in natural gas production within the United States has put irresistible downward pressure on the price of natural gas, a reality that completely swamps any purported effect that commodity index buying could conceivably have.

Black line: Monthly spot price of West Texas Intermediate in dollars per barrel (data source: EIA). Green line: six times the U.S. natural gas wellhead price in dollars per thousand cubic feet (data source: EIA).

Here’s another example some people like to give, comparing the price of crude oil with that of rhodium, with the latter scaled so that the two prices were comparable in 2005. The price of rhodium shot up spectacularly relative to crude oil over the next few years. That, too, had nothing to do with index fund investment buying. Neither GSCI nor DJ-AIG includes this commodity– in fact, to my knowledge it is impossible to buy a futures contract in rhodium.

Black line: Monthly spot price of West Texas Intermediate in dollars per barrel (data source: EIA). Turquoise line: price of rhodium in dollars per ounce divided by 30 (data source: Kitco).

These two examples highlight that fundamentals of supply and demand can be far more important than any effects of speculative purchases in futures markets. Although it’s a well known story, it’s worth restating the contribution that those fundamentals have made for the oil market in particular. The graph below plots global oil production since 2002. A key fact that brought us where we are today is that global oil production basically stagnated between 2005 and 2009.

Total global oil production, in millions of barrels per day, annual 2002-2010 (data source: EIA).

But over these same 5 years, world real GDP increased by 17.2% logarithmically [that is, ln[y2009] – ln[y2004] = 0.172 for yt world real GDP in year t]. If there had not been significant increases in the price of oil over this period, we would have expected to see a big increase in the quantity demanded globally.

How big an increase that would have been depends on the income elasticity of oil demand. Academic studies suggest we might use an income elasticity of around 0.5 to describe the U.S. today but a value closer to 1.0 for emerging economies. The emerging economies account for about 70% of the growth in world petroleum consumption since 1998, so I would be inclined to use a value closer to 1 than to 0.5 if we want to talk about total world demand. The illustrative calculations below assume a world income elasticity of 0.75, which implies that, if the price of oil had not risen, the 17.2% increase in world income would have been expected to lead to a (0.75)(17.2) = 12.9% increase in oil consumption. The red line in the graph below plots the level of oil demand predicted on the basis of the observed world GDP for each year since 2002 if one uses this income elasticity of 0.75 and if the price of oil had not changed over this period. Steve Kopits has used a similar graph, derived from a different set of assumptions, to make the same point. The recession in 2009 would have been expected to produce a small dip in consumption that year, but despite the recession, oil production today is about 10 million barrels a day below the value that I would have expected to be associated with a stable oil price.

Black line: total global oil production (same as in preceding figure). Red line: global oil production in 2002 times (yt/y2002)0.75 where yt denotes global world GDP in year t as reported by IMF World Economic Outlook, April 2011, Table A1.

The reason we’re not consuming 97 mb/d is because the price of oil didn’t stay constant. Let’s next ask how much the price would have to go up to keep the quantity demanded equal to the amount currently being produced. The answer to this question depends on the price elasticity of oil demand, a number for which there is a range of estimates. For illustration, if we assume a price elasticity of 0.1 and if we treat the base price in 2005 as $50/barrel (in 2010 dollars), then in order to reduce the quantity of oil demanded by 10.79% [this is the logarithmic gap between the black and red curves in the graph above for 2010], the price would have had to go up to $147:

In other words, if you believed that an income elasticity of 0.75 and price elasticity of 0.1 were the right numbers to apply to this 5-year period, you’d think we should be paying about $147/barrel today.

Now such calculations are extremely sensitive to the price elasticity that you assume. If for example you thought that demand was twice as sensitive to price as assumed above (that is, the price elasticity should be 0.2 instead of 0.1), then you’d expect the price of oil today to be more like $86/barrel:

Or you might believe that the short-run price elasticity is about 0.1, but given more time to make adjustments such as the kind of cars we drive, the longer-run elasticity is closer to 0.2. In that case, you would have expected to see the price temporarily go up to $147/barrel, but by now to have fallen back to about $86. Which, it turns out, is exactly what happened.

I do not mean to defend these rough calculations as the literal description of how the world works. But I do think they illustrate that there is really nothing all that mysterious about the behavior of oil prices over the last five years.

If you want to repeat these calculations with your own favorite parameters, be my guest. If, for example, you believe the price elasticity is more like 0.25, then you’d conclude the price of oil today should only be $77, and you could claim that any current excess over that number must represent the effects of speculation. I’m not going to try to talk you out of such a view, but instead would invite you to answer Paul Krugman’s question in reference to the diagram below. The horizontal axis measures the number of barrels of oil physically produced or physically consumed. Assume whatever you like about income and price elasticities to derive the value P0 that you maintain is the price that would be justified by the true underlying fundamentals, whatever you conceive that number to be.

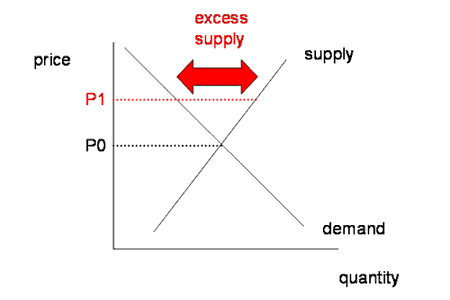

Now, if you further maintain that financialization of futures markets has caused the dollar price of a physical barrel of oil to be some value P1 higher than P0, that higher price should mean that quantity demanded is lower than it would have been at a price of P0. Where, then, is the extra oil going? Or, to put it another way, if you believe that we’re currently in balance at a price of P1, how could we still have enough to satisfy the extra demand that would arise if the price fell to P0?

Granted, if supply and demand are relatively insensitive to price over the short run (so that both curves above are very steep), the price could be off for some time before there is much evidence of inventories piling up or being drawn down. In this respect, it is conceivable to me that speculation could have some real effects. But the conditions under which a theory of commodity financialization could essentially ignore fundamentals– namely, the assumption of a very low price elasticity of demand– are precisely the conditions under which a fundamentals-based interpretation would say that what we have just experienced makes perfect sense.

Although I remain open to evidence on a possible short-run contribution speculation may have had, one aspect of the debate over this issue worries me. The plots above of oil production over time in my mind highlight what has been a significant economic challenge over the last few years and very possibly an even bigger challenge in the years ahead. I would like to see more consensus on what seems to me to be a very clear statement of fact, which is, stagnating global production is by far the most important reason for a rising price of oil.

Insofar as discussion of commodity futures speculation causes some people to ignore this critical reality, I fear that it may be doing us a significant disservice.

OPEC, Libya and the laws of supply and demand are not responsible for high gasoline and oil prices. The oil price is dictated by the fraudulent “round-trip” trades of the “dark pool” trading in the Intercontinental Exchange (ICE) in Atlanta. The international Big Oil/big banking cabal owns ICE. ICE operates outside of US law. The Commodity Futures Trading Commission has no jurisdiction over ICE, bribed by Big Oil. ICE’s energy traders and speculators can ratchet-up the oil price anytime they feel like it, for their own profits and on the behalf of Big Oil, through the use of “round-trip” trades. Google the “Global Oil Scam.” ICE is a super Enron. Oil is too critical a resource to be controlled and manipulated by greedy refiners, greedy corporations, greedy traders and greedy speculators.