Forget about the S&P downgrade, which has had ZERO impact on the global equity markets. The downgrade was supposed to mean that it would be more likely that the US government would not be able to pay its debt than previously assumed. IF the markets took this warning seriously, then they would have attached a higher risk premium to US government bonds. Of course, the opposite occurred. US bonds soared in price. In other words, investors, both here and abroad, voted with money as loudly as possible that they view the US government debt as a very safe haven in a time of financial turmoil

So if it wasn’t the S&P downgrade which caused this downward cascade in the global equity markets, then what was it? By far, the most important factor currently driving the market’s bear trends is Europe or, more specifically, the future of the euro and the European Monetary Union. Systemic risk has migrated across the Atlantic to the euro zone.

And after yesterday’s joke of a summit between German Chancellor Merkel and French President Nicolas Sarkozy, it appears yet again that Europe’s policy makers have comprehensively blown it. Their persistent reluctance to get ahead of the looming systemic ticking bomb at the heart of the euro project has reached the point where it is likely to doom the euro’s existence. Their repeated “rescue plans” (and equally fatuous statements about new committees and “euro solidarity) can no longer mask the central problem, which is that countries with very different economies are yoked to the same currency in the absence of a fiscal transfer union which would otherwise facilitate growth, not ongoing economic depression and political turmoil.

Rather than attempting to stave off a double-dip recession by easing fiscal and monetary policy, the European Central Bank (ECB) has gone careening off in the opposite direction. The euro project is consequently being turned into a Hooverian instrument of economic torture from sado-monetarists, such as Jean-Claude Trichet, who see each bailout as a way for irresponsible nations to offload their liabilities onto their fitter neighbors, rather than considering the flawed institutional structures which created the need for these stop-gap measures in the first place. Interest rates have been raised, and member states have been forced into self-defeating austerity programmes which, by destroying growth, have made underlying debt dynamics even worse. It is hard to imagine a more tragic and self-defeating type of policy mix. It is 1937 writ large.

How long will voters in rich countries stand for this? Perhaps not much longer as the Germans in particular appear to have no stomach to withstand the costs required to save the currency union. So what is this problem at the heart of the euro project?

Let’s go back to first principles: it is important to recognize the difference between sovereign and non-sovereign currencies. A government with a non-sovereign currency, issuing debts either in foreign currency or in domestic currency pegged to foreign currency (or to a precious metal, such as gold), faces solvency risk. However, a government that spends by using its own floating and non-convertible currency cannot be forced into default, unless they willingly choose to do so (such as the US Congress almost prepared to contemplate during its recent debt ceiling negotiations). It is why a country like Japan can run government debt-to-GDP ratios that are more than twice as high as the “high debt” PIIGS, while enjoying extremely low interest rates on sovereign debt. A nation operating with its own currency can always spend by crediting bank accounts, and that includes spending on interest. Thus, there is no default risk in terms of a capacity to pay (as opposed to political WILLINGNESS to pay).

But as has been noted by many critics of the common currency project, the relation of member countries to the European Monetary Union (EMU) is more similar to the relation of the treasuries of member states of the United States to the Fed than it is of the US Treasury to the Fed. A country like Ireland is more like New York within the EMU than a sovereign state. This means it has little domestic policy space to use monetary or fiscal policy to deal with crisis. The upshot has been that in the face of the first large negative demand shock to hit the region, the nation states have quickly found they cannot use fiscal policy in a responsible way to protect its economy from rising unemployment and collapsing income. In a normal federation, the national government can always ensure the solvency of the constituent parts via fiscal transfers. In the legal design of the EMU, there is no such role specified and attempts by the member states to cushion the demand collapse quickly raised the ire of the Euro elites with the ECB leading the charge to impose austerity on errant governments.

In the US, states have no power to create currency; in this circumstance, taxes really do ‘finance’ state spending and states really do have to borrow (sell bonds to the markets) in order to spend in excess of tax receipts. Purchasers of state bonds do worry about the creditworthiness of states, and the ability of American states to run deficits depends at least in part on the perception of creditworthiness. While it is certainly true that an individual state can always fall back on US government help when required (although the recent experience of the debt ceiling negotiations makes that assumption less secure), it is not so clear that the individual countries in the euro zone are as fortunate. Functionally, each nation state operates the way individual American states do, but with ONLY individual state treasuries.

The euro dilemma, then, is somewhat akin to the Latin American dilemma, such as countries like Argentina regularly experienced during the time that they operated currency pegs. Given the institutional constraints, deficit spending in effect requires borrowing in a “foreign currency”, according to the dictates of private markets and the nation states are externally constrained. That’s why Ireland and Latvia are in a mess and suffer from solvency issues. It’s also why California suffers from a solvency issue or Italy or Spain. Not the US or Japan, which explains why the latter has been able to borrow money at around 1% for the past two decades, despite a public debt to GDP ratio about twice the US or the euro zone.

At this juncture, however, there isn’t enough time to create a “United States of Europe”, which is why the ECB has resumed its bond buying operations to put a floor on the bonds and alleviate concerns about the solvency issues of the individual nation states. The ECB has received a lot of criticism for this. In one sense, the criticisms are legitimate: The ECB is in effect playing a “fiscal role” for which they are ill-suited. They buy time by buying the bonds. But the bond buying attacks the symptoms, rather than the underlying problems. And it’s fundamentally undemocratic: In taking up this role – by way of the ad hoc bailouts and secondary bond market purchases the ECB has become a sort of fiscal tsar unanswerable to any national electorate.

The hope is that by backstopping the bonds, the ECB can persuade the markets that countries like Italy and Greece are not insolvent and that these countries will resume funding them. Clearly, with credit spreads blowing out again, this has proved to be a fatuous hope because the scale of the purchases have not been large enough to be credible, especially now that the contagion is spreading into core countries such as France. Europeans still have to get the institutional arrangements right and the ECB, as the sole issuer of euros, is the only instrument that today can play this role, albeit imperfectly, but there is a better way.

Immediate relief can be provided by the ECB, which should be directed to create and distribute several trillion euros across all euro zone nations on a per capita basis. This would not constitute a “bailout” as such as Germany (with the largest per capita economy) would be the largest recipient. Each individual eurozone nation would be allowed to use this emergency relief as it sees fit. Greece might choose to purchase some of its outstanding public debt; others might choose fiscal stimulus packages. While this might sound much like the current bail-out, in which the ECB buys government bonds in the secondary markets from banks (assuming the risk of a default by Greece, for example), the emergency package outlined here (first proposed by Warren Mosler www.moslereconomics.com ) would be under the discretion of the individual nations.

Hence, the ECB would finance current government operations if national governments chose that course of action. And if they found that a country was abusing the privilege (for example, Greece being deficient in tax collection), it could withhold the payments until compliance was achieved. In effect, the sanction would be more credible as it would constitute the ECB withholding carrots, rather than beating up fiscally stressed countries with a stick and seeking compliance with a country already in dire economic straits. More significantly, the revenue sharing proposal would address the contagion impact, as the ECB could continue the distributions to other countries, even as it punished the “recalcitrant problem children”.

We emphasise that this does not address the problem of deficient aggregate demand, but does address the solvency issue, which is the main systemic threat to the euro zone right now (indeed, to the entire global economy). By persuading the markets that most of the euro zone is creditworthy, the risk of the markets shutting these countries down diminishes considerably. As these countries fund themselves on credible terms in the private markets, they can begin to grow again.

Of course, putting the problem in this context and putting out a figure that has a trillion euro handle on it, makes it harder to believe that it will be politically palatable to the ECB or its stronger creditor nations such as Germany. Which is why we think that our earlier suggestion (link) might be the more likely endgame:

“The likely result of a German exit would be a huge surge in the value of the newly reconstituted DM. In effect, then, everybody devalues against the economic powerhouse which is Germany and the onus for fiscal reflation is now placed on the most recalcitrant member of the European Union. Germany will likely have to bail out its banks, but this is more politically palatable than, say, bailing out the Greek banks (at least from the perspective of the German populace).”

The question remains: do the Germans ultimately quit the euro to save Germany or do they take the view that their fate is too intertwined with the common currency and that departure imposes an even greater economic and political cost.

If the latter, the Germans have to be made to understand that core problem at the heart of the euro zone is NOT a problem of “Mediterranean profligacy”. Many people, particularly in Germany, express the view that the Italian, Greek or Portuguese governments (and by association their people) are to blame for this crisis – accessing cheap loans from Northern European banks, not paying enough taxes, not working hard enough, etc (this also seems to be a common view amongst readers of this blog).

One thing is clear from the remarks that continue to emanate from Europe’s main policy makers. They do not understand basic accounting identities. They fail to see any kind of relationship between their own export model and their trading partners.

For example, it is ironic (and more than a touch hypocritical) that Germany chastises its neighbors, like Greece, or its trading partners like the U.S., for their “profligacy”, but relies on these countries “living beyond their means” to produce a trade surplus that allows its own government to run smaller budget deficits.

It’s even more extreme within the euro zone in the context of the global economy. The European Monetary Union bloc as a whole runs an approximately balanced current account with the rest of the world. Hence, within Euroland it is a zero-sum game: one nation’s current account surplus is offset by a deficit run by a neighbor. And given triple constraints — an inability to devalue the euro, a global downturn, and the most dominant partner within the bloc, Germany, committed to running its own trade surpluses — it seems quite unlikely that poor, suffering nations like Greece or Ireland could move toward a current account surplus and thereby help to reduce its own government “profligacy”.

What about the issue of laziness, corruption, poor tax collection, all of the charges usually hurled against the so-called “PIIGS” countries? To this we would simply ask, even if the “Club Med” countries are lazy and don’t pay taxes, why did this crisis come now? As Bill Mitchell has noted, these countries didn’t just become “lazy” when they joined the EMU. Why didn’t, say, the Italian government face insolvency prior to joining the EMU? The point is that it might be sensible if the Italian government could get the high income earners to pay more tax and it might be sensible to raise productivity but, as Mitchell has argued, none of these things are intrinsic to their crisis.

No, the problem is the Euro and it is a shared problem across the Euro zone. And this is what is beginning to dawn on the markets, as the contagion spreads from the periphery into the core.

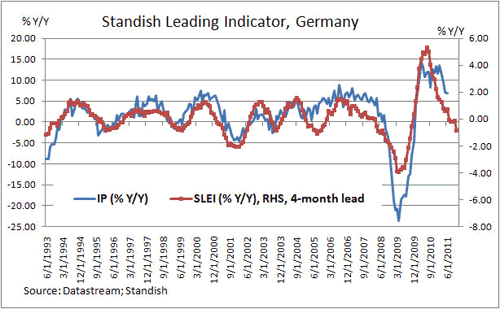

Consider the chart constructed by the economist, Rebecca Braeu, of Standish Management:

The red line refers to Germany’s leading economic indicators – order books, exports, etc., and point to dramatically slower growth in the months ahead. Germany is in effect also a passenger on the Titanic, as Italian Finance Minister Guilio Tremonti recently noted. It might be in the first-class cabin, rather than steerage (or Irish stowaways, as the Germans no doubt view the former “Celtic Tiger”), but when the boat hits the iceberg, all passengers are affected.

Until now, the Eurocrats have either remained in denial about the mounting stress fractures within the system, or forced weaker countries to impose even greater fiscal austerity on their suffering populations, which has exacerbated the problems further. And there has been a complete lack of consistency of principle. When larger countries such as Germany and France routinely violated spending limits a few years ago, this was conveniently ignored (or papered over), in contrast to the vituperative criticism now being hurled at the Mediterranean profligates. The EU’s repeated tendency to make ad hoc improvisations of EMU’s treaty provisions, rather than engaging in the hard job of reforming its flawed arrangements, are a function of a silly ideology which is neither grounded in political reality, nor economic logic. As a result, a political firestorm, which completely undermines the euro’s credibility, is potentially in the offing.

And to judge from the flaccid statement that accompanied the conclusion of the Merkel-Sarkozy summit yesterday, it appears that even at this late stage, policy makers don’t get it, or just cannot summon up the political will for the huge conceptual leap forward required to save the euro. The Germans are paralysed politically and things are moving too fast for their policy makers to respond quickly. And their political leadership has neither leveled with the electorate in regard to the magnitude of the problem, nor the costs associated with ongoing punishments of the profligates. Whenever a German political leader opens his/her mouth it is to announce bad news, like the recent statement by German Finance Minister Wolfgang Schauble that the German government was opposed to any increase in the EFSF’s resources, or the creation of a euro bond, even though such a move is essential for the medium-term stabilisation of financial markets!

At this juncture, then, it seems more likely that the Germans will try to save themselves by pulling out of the euro zone (and then they recapitalise their own banks, as they did following German reunification). They take the Benelux countries with them (which have already closely converged with Germany’s economy) and have a “Greater DM” bloc and buy the rest of Europe on the cheap with their newly reconstituted DMs.

The Club Med, such as Greece, Italy, and Spain countries are saved because the euro plunges and they get to export their way out of this. The euro becomes a soft currency country again and these countries go back to living with higher inflation, higher exports and probably a generally more comfortable way of life.

Interestingly enough, the country which really gets screwed in this type of environment is France which is neither a true “Club Med” economy, but has yet to undertake many of the structural reforms of its German counterpart which it is seeking to emulate. Its economy is more akin to that of Italy, but should it seek to become part of the “greater DM bloc”, then its industrial base will likely face a huge competitive threat from Italy.

In any case, there appear to be no happy outcomes here (although as my friend, Tom Ferguson always reminds me, “If you want to have a happy ending, go see a Disney film”). We appear to be entering most dangerous time for Europe since World War II.

Leave a Reply