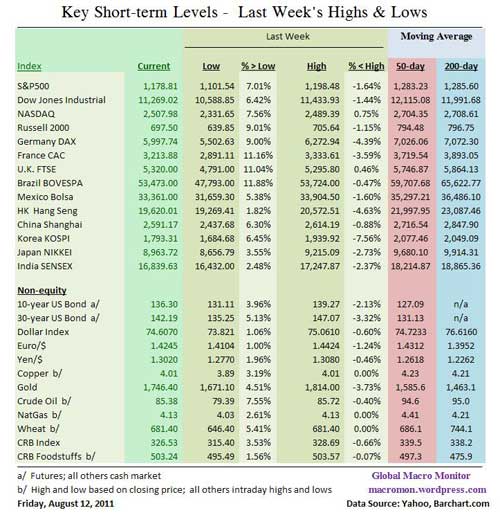

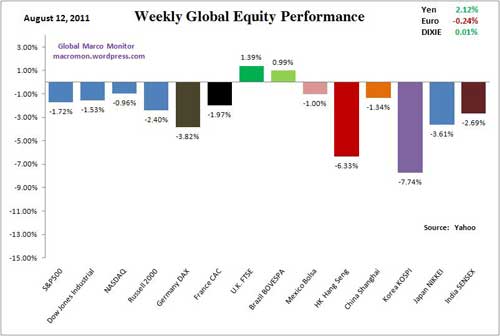

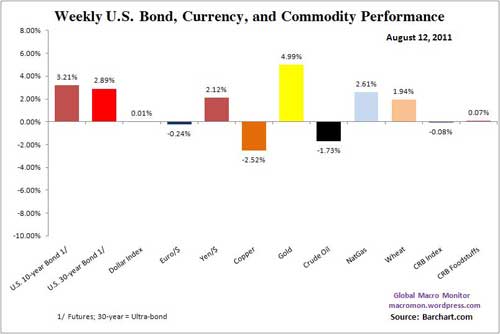

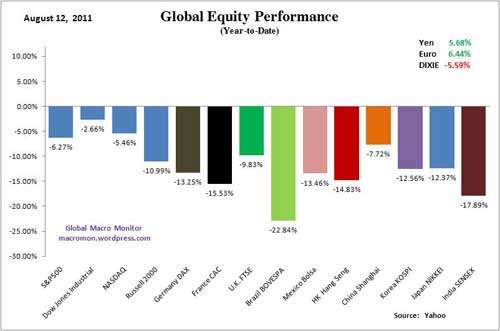

What a week. What a year. Who would have predicted that U.S. bonds, even in foreign currencies and a sovereign downgrade, would be outperforming the BRIC equity indices and copper by several hundred basis points in mid-August? Stunning and a lesson from W.B. Yeats: “The best lack all conviction, while the worst are full of passionate intensity.” Longevity in markets demands that discipline trumps conviction.

We have no idea where this is all headed as we are like the falcon that cannot hear the falconer but our sense is the markets will continue to turn and turn into widening gyre until it is clear the center of Europe can hold. Furthermore, Toto has pulled back the curtain on the Wizard of Oz and the loss of confidence in American and European leadership is another led shoe that will continue to weigh on markets. All this, combined with uncertainty and worries over global growth makes it’s difficult to argue for a sustained equity rally anytime soon, or, let us say, we lack all conviction for a sustained rally.

Nevertheless, which ever way the market leans in the short-term, many with little tolerance for pain will be caught off guard and sent scrambling to cover or dump positions keeping volatility relatively high, in our opinion. And don’t forget the Battle of the ‘Bots. Last week’s performance shows what happens when capital stampedes like buffalo with absolutely no idea where to go. On a positive note, Apple remains very well bid and bounced nicely off its 50-day moving average.

One last point, if everyone is piling into the Swiss Franc due to worries over a European banking crisis, have they not looked at that country’s bank asset to GDP ratio? Just askin’.

Leave a Reply