Morgan Stanley is downgrading Google (NASDAQ:GOOG) to Equal-Weight from Overweight with a $600 price target (prev. $645).

– Google is spending to innovate in social / local, retain talent, and to drive user adoption of key products, but those investments have uncertain ROI / payback periods. Morgan Stanley is reducing their PT to $600 (from $645) and C2012e EPS to $34, below consensus of $40.

Details:

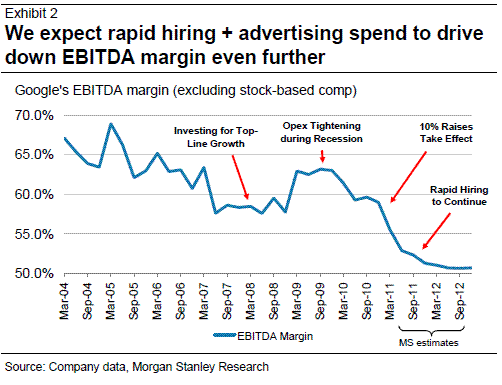

Debate #1: Will margins decline from here? Yes. Given Google’s aggressive hiring plans, rising compensation expense, and significant advertising spend on Chrome & other Google products, we expect EBITDA margin to decline in C2011 / C2012.

Google is now hiring at a blazing pace (1,900+ net hires in CQ1) and is likely to attain its goal of making 2011 its “biggest hiring year in company history” – per Alan Eustace, Google’s SVP of Engineering & Research“. As a result, we believe the company is on track to hire 7,000 employees this year (an increase of 19% from year-end C2010), up from our prior estimate of 4,000 net additions.

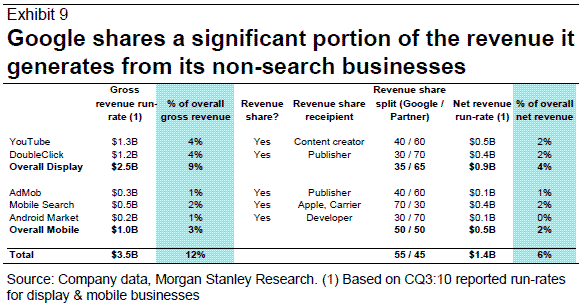

Debate #2: Will “newer” businesses drive near-term revenue outperformance? No. We believe the consensus is too optimistic on the net revenue contribution of newer businesses, such as DoubleClick, YouTube, AdMob, Android Market, and mobile search. In 2011, we expect search & contextual ads to contribute ~90% of Google’s net revenue.

Debate #3: Will investments in local eCommerce and / or social pay-off? Too early to tell. We are encouraged by early progress of Google Plus and Google Offers, but Google faces stiff competition from incumbents who have first mover advantage. The pay-offs of such endeavors may be longer-term.

Google’s approach to capturing markets is to grow users / market share first, and monetization (profitability) second. We expect them to take a similar approach with Google Offers and Google Plus, which should limit near-term financial contribution even if both products prove successful. Further, these businesses appear to be scale businesses whereby the highest margin profile accrues to the market share leader. If Google is not able to capture a leadership position in the market, it may not enjoy EBITDA margins as high as in its core business.

As a Result, We Are Reducing Our Estimates

We are reducing our profitability estimates (now significantly lower than consensus) due to the following: 1) Google’s aggressive hiring plans, 2) rising salaries due to a competitive hiring environment, and 3) increased advertising spend to drive usage of new / existing products.

Our new CQ2 / C2011E EBITDA estimates are $3.44B / $14.5B, roughly 4% / 5% below consensus estimates. Our revised CQ2 / C2011E operating EPS estimates are $7.45 / $31.44, approximately 5% / 7% below consensus.

Notablecalls: Morgan Stanley has been a Google Bull since 2008. So that makes the call potentially a significant one.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply