Capstone Investments is making the call none of the other Wall Street firms want to make:

LinkedIn (NASDAQ:LNKD): Initiating Coverage with a ‘SELL’ and $45 price target – Price isn’t the Only Risk

– The 18 pg note accuses the online recruiting firm of creative accounting, lower-than-advertised user base, high fixed cost business model and poor corporate governance.

All this they say, comes with a bubbly valuation not seen since 1990’s. According to Capstone, their Street low $45 price target could prove to be too optimistic as the company fails to execute its ambitious business plan & insiders start dumping the shares. IPO lock-up expires in November 2011.

‘… LinkedIn is an online professional identity and recruitment tool. Sprinkle on the “social media” moniker and in the Internet Bubble 2.0 you can price an IPO at $45per share, or 34% higher than the price talk midpoint, and the watch the stock rise to $94.54 – although it has been as high as $122.70 and as low as $60.14 over the sex weeks since LinkedIn’s stock offering – to give this break-even business a $93.4 billion market cap. … ‘

Paul Meeks, CFA at Capstone

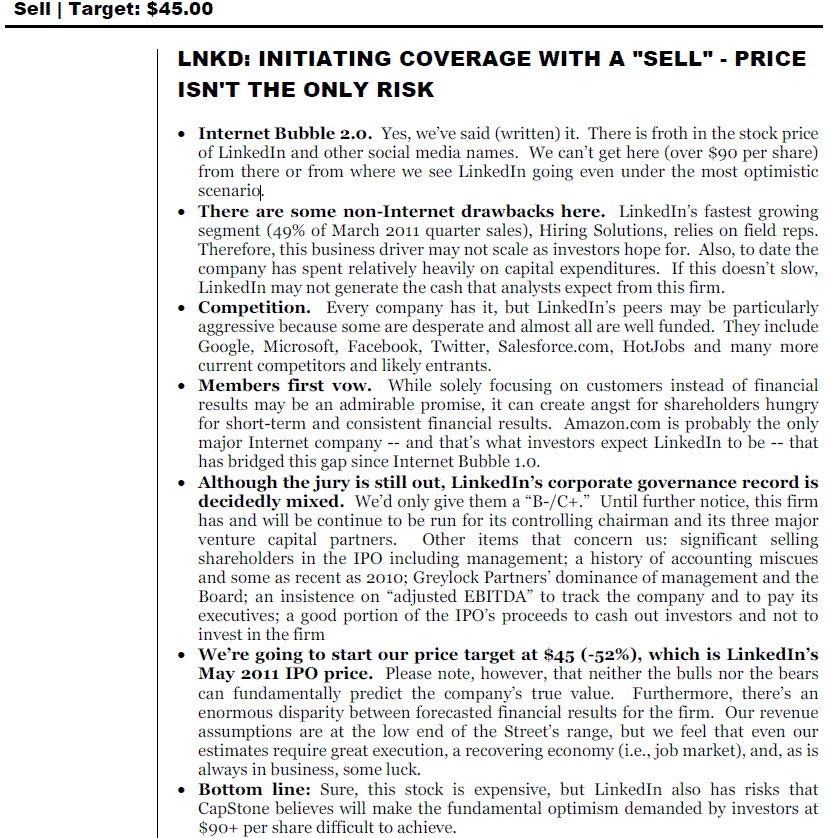

The PDF file is copy-locked so I can only show you the Summary page of the note:

(click to enlarge)

Notablecalls: There are two reasons why LNKD has only Buy ratings from major Wall Street firms:

– Merrill, JPM, Morgan Stanley & UBS were the underwriters. They need to keep their clients (both sides) happy.

– Facebook. The biggest IPO in recent memory is expected some time in 2012. Everyone wants a piece of the action and they are not going to get it by issuing Neutrals (or god forbid Sells) on other Social Media names.

That leaves the door open for Capstone to come in with a seriously scary story and a price target that should send people selling at least in the n-t.

I expect LNDK to trade down today, possibly to the tune of 5-10%, putting $89-85 levels in play.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply