The economy is growing very sloooooowly. It’s growing for sure, but at a pace that frustrates pretty much everyone. The Federal Reserve has just announced that it notched down its internal forecasts, which private sector forecasters have also done. What does slower economic growth mean for banks? There are implications for asset quality, loan growth and equity valuations.

Bank Asset Quality and Lower Economic Growth

Banks are gradually working through their problem loans. In some cases they are writing off loans, foreclosing on properties, selling their REOs. In other cases their clients are slowly able to work their way into better condition. All of this would go faster with better economic growth. The workout process will continue even with slower growth, but the timelines will be longer. The destination is the same, but the speed at which we approach the destination has been lowered.

Bank Loan Growth Will Continue To Be Weak

All bankers have been frustrated by the lack of credit-worthy lending opportunities. Many real estate deals do not pencil out with current vacancy rates, rents and construction costs. A stronger economy will lower vacancy and push rents up, with relatively little impact on construction costs. Slower economic growth will limit net absorption of properties, delaying those occupancy and rent increases. Thus, it will be even longer before new projects pencil out.

Commercial and industrial lending will similarly be slow to rebound. The three usual triggers of C&I lending are capital spending, inventory increases and accounts receivable increases. All three of these result from stronger sales. Slower economic growth will delay companies’ need for external funds.

Bank Profitability Will Not Improve

Banks are already seeing non-interest income slide, and between regulatory change and fee consciousness on the part of customers, no improvement is in sight.

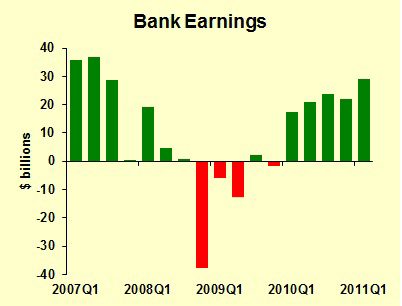

Deposit growth should continue, and may even improve thanks to the lagged effects of the Federal Reserve’s second round of quantitative easing, dubbed QE2. However, extra deposits don’t help if loan demand if absent. For many banks, the yield they earn parking their deposits at the Fed is lower than the FDIC assessment, so additional deposits actually hurt the bank. Combining these factors with flat loan growth and slower workouts, bank earnings are unlikely to improve significantly.

Bank Equity Valuations Have Already Fallen

The stock market is not waiting for bank earnings to hit that lower trajectory. As it has become obvious that earnings growth will not as strong as expected at the beginning of the year, bank stock prices have fallen. The KBW Bank Index has dropped 12 percent since the first of the year.

Bank Risks Are on Both the Upside and the Downside

There is good news possibly coming, but first let’s remember the potential bad news. The European debt crises are not behind us and could yet trigger a recession on the Continent. If that happens, there is a fairly good chance that the United States would also fall into a recession, albeit a short, mild one. Businesses in all industries should do some contingency planning for this possibility.

However, most of the potential domestic bad news seems to have been priced into bank stocks already. Any positive surprise will help valuations. There is good reason to expect that the current economic malaise will prove temporary. Part of the manufacturing weakness of recent months was driven by lack of parts, thanks to the Japanese earthquake and tsunami, as well as supply constraints from Chinese vendors working at full capacity. Both of these supply issues are being resolved now.

Some consumer spending was limited by lack of availability of cars. That applies not just to imports, but also to Japanese nameplate cars made in America, and even American-branded cars that use foreign components.

The Fed’s QE2 stimulus is nearing completion as of this writing, but there is a significant time lag between cause and effect. Milton Friedman famously said that the time lags in monetary policy are “long and variable.” A rough rule of thumb is to expect 12 months between Fed action and an impact on the economy. That implies a stronger economy in the fourth quarter of this year and the first quarter of 2012.

Bank Management Trumps Small Changes in the Economy

The economy clobbered most banks in the United States, even many that were very well managed. However, aside from huge economic shifts, management is more important than the economy. The ability of a bank to serve its customers, acquire additional customers, and operate efficiently is more important than the change in the economic outlook under discussion. Be aware of the economy, develop contingency plans for alternative economic scenarios, but keep focused on running a great bank.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply