Zach Goldfarb’s profile on Treasury Secretary Timothy Geithner ignited a firestorm among bloggers with the money quote:

The economic team went round and round. Geithner would hold his views close, but occasionally he would get frustrated. Once, as Romer pressed for more stimulus spending, Geithner snapped. Stimulus, he told Romer, was “sugar,” and its effect was fleeting. The administration, he urged, needed to focus on long-term economic growth, and the first step was reining in the debt.

Wrong, Romer snapped back. Stimulus is an “antibiotic” for a sick economy, she told Geithner. “It’s not giving a child a lollipop.”

Reactions on the shift to a deficit-reduction strategy come from Ryan Avent, Felix Salmon, and Mike Konzcal, among others. The general view is that Geithner has pushed the Administration into an economically dangerous position, guaranteeing millions remain unemployed, for absolutely no good reason. The yield on the 10-year Treasury is mired at 3%. Where is this loss of confidence that is so feared in Washington?

Salmon gets to the heart of Geithner’s thinking here:

Geithner cut his teeth in a world of bond vigilantes, an era when James Carville said that he would like to be reincarnated as the bond market, because then he could intimidate everybody. And after that, Geithner dealt with a series of international sovereign-debt crises where countries found themselves hammered by enormous bond spreads.

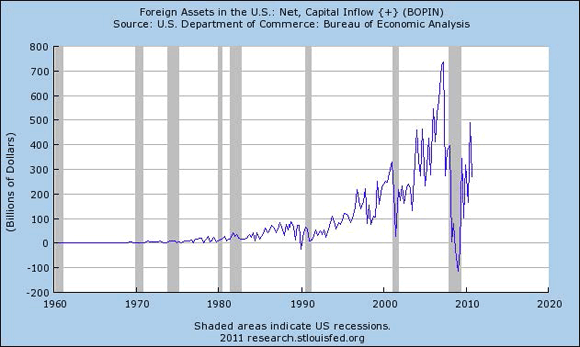

I suspect – guessing, really – that Geithner is very much concerned the US is uncomfortably close to a currency crisis. Indeed, I think that we were closer to such a crisis in 2008 than many realize:

That kind of shift in asset flows is sort of difficult to dismiss as irrelevant. The only thing that pulled us out of the fire was the willingness of foreign central banks to accumulate dollar assets to compensate for private outflows, no strings attached (of course, those banks arguably had no choice, as their accumulation of Dollars helped support the imbalances that made a currency crisis possible). If the IMF had been called upon, they surely would have wanted strings attached, and one such string would almost certainly have been a deficit reduction program.

Crazy, you say? Look to Greece.

That’s all ancient history. Now, the goal is to prevent it from happening again. And that is where Geithner is trying to engineer what a massive expenditure switching program. That program was thoroughly described by New York Federal Reserve President William Dudley in a speech that was lost in excitement surrounding Federal Reserve Chairman Ben Bernanke’s latest assessment of the US economy. Greg Ip gives the short version:

To get the federal deficit from its current 10% of GDP to a more manageable 3% will require America to generate additional consumption, investment and net exports equal to 7% of GDP. Since it already consumes too much, that leaves business investment and net exports.

Monetary policy can help achieve this by accommodating the shift in relative prices that rebalancing requires. Mr Dudley notes that surging EME growth has driven up prices of both commodities and their own exports as domestic wages rise. That has driven up headline inflation in America. But Mr Dudley makes the crucial point that this represents a deterioration in America’s terms of trade and thus its standard of living. It is not a generalised inflation problem unless it leads to second-round wage and price catch-up, of which there is no sign. Not only does such a terms of trade shock not call for tighter monetary policy, it is essential to rebalancing. As foreign prices rise relative to American prices, America will export more and import less.

(Note also that Yves Smith linked to the Dudley topic even sooner). I have tended to think in similar terms – that, over time, the US economy needs to shift away from reliance on consumer spending toward nonresidential investment. Absent the US consumer, where, you ask, will the demand come from to support such investment? Increased exports and import competition, both of which are facilitated by a weaker Dollar.

Would such a decline become disorderly? That is probably what Geithner fears, and his response is that it is less likely to occur, and more easily managed should it occur, if the US fiscal position is stabilized, the sooner the better. Others, particularly China, must participate as well – hence the push to revalue the yuan.

Obviously, the conundrum here is that this process involves structural adjustment, which involves – you guessed it – structural unemployment. Which, understandably, raises the ire of left-leaning economists and bloggers. And we go full circle – how can we accept high unemployment when interest rates are so low?

I am a bit stuck on this issue. Most mornings I wake up and think the Administration’s focus on deficits is insane. There have been predictions of a Dollar collapse for a decade. Should we deny employment opportunities to millions for another decade on the basis of such failed predictions?

A few months ago, I rushed back to Eugene from a Portland Business Alliance meeting where I was given a lapel pin that read “JOBS.” While picking up my son from soccer practice, another parent noticed the pin and said “Nice pin. I wish I had one of those.” “A pin,” I replied, thinking I have another in my pocket. Duhhh – dumb economist. “No, a job,” was the response. Those are the times you think, yes more stimulus, lots more, now.

And, admittedly, at other times I think the costs of a currency crisis would be very, very high, with a rapid imposition of massive structural adjustment. Given the possibility of such an outcome, which, I reiterate, was not inconceivable during the recent financial crisis, don’t policymakers have a responsibility to work toward a more balanced pattern of growth?

In addition to clearly differentiating between the short and long run deficits, I think if you want to meld these to positions into a consistent policy framework, the objective is to support deficit reduction via higher taxes on upper-income groups, those least impacted by the structural adjustment away from consumer spending, while maintaining spending on the social safety net. Whether this ultimately occurs, or if instead the weight of deficit reduction falls most on those negatively impacted by structural adjustment, remains to be seen.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply