McDonald’s Corporation (MCD) continues to post strong same-store sales numbers around the globe. After a solid increase in the first quarter, the company posted a 3.1% gain in global same-store sales for May.

Estimates have been consistently rising for MCD over the last several months as the company has been relatively successful in combating rising commodity costs. It is a Zacks #2 Rank (Buy) stock.

The company also continues to generate enormous amounts of free cash flow that it has used to return value to shareholders. It spent approximately $2.0 billion in the first quarter of 2011 buying back shares and paying dividends, for instance.

May Sales

On June 8, McDonald’s reported global same-store sales growth of 3.1% for the month of May. Growth was solid across each regions, but the Asia/Pacific, Middle East and Africa segment was particularly strong with a 4.3% gain. Growth in China was a major contributor.

In the U.S., same-store sales were up 2.4% due in part to the launch of Frozen Strawberry Lemonade, the popularity of Fruit & Maple Oatmeal and strong demand for the company’s signature beverage and core offerings. In Europe, same-store sales grew 2.3%.

First Quarter Results

The very solid sales in May comes on top of a strong first quarter. The company reported a 4.2% jump in same-store sales in Q1, led by a 5.7% increase in Europe. Overall, revenues rose 9% to $6.112 billion, ahead of the Zacks Consensus Estimate of $6.008 billion.

Food and paper costs at company-operated restaurants increased from 32.9% of sales to 33.6% of sales reflecting higher commodity prices. The company was able to leverage its fixed expenses, however, sending operating income up 9%.

Earnings per share came in at $1.15, edging out the Zacks Consensus Estimate by a penny. It was a 15% increase over the same quarter in 2010.

Solid Growth Ahead

While rising commodity prices are expected to squeeze margins a bit, the company expects the damage to be relatively modest. For the full year 2011, management expects the total basket of goods cost to increase 4 to 4.5% in the U.S. and Europe.

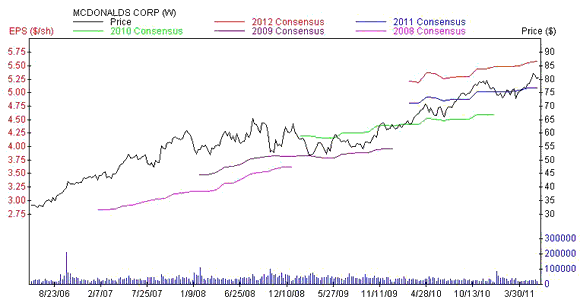

Analysts raised their estimates off the strong quarter and solid May sales figures. The Zacks Consensus Estimate for 2011 is $5.11, corresponding to 11% growth over 2010 EPS.

The 2012 consensus estimate is currently $5.60, representing 10% EPS growth.

Consensus estimates have been steadily increasing over the last several months, as seen in the company’s Price & Consensus chart:

It is a Zacks #2 Rank (Buy) stock.

Cash Flow Kings

McDonald’s continues to generate ridiculous amounts of cash and has been returning it to shareholders through stock buybacks and dividend increases. In the first quarter, for instance, it spent $2.0 billion in share repurchases and dividends.

Over the last 10 years, the company has raised its dividend at a compound annual rate of 27%. It currently yields 3.0%.

Valuation

The valuation picture still looks very reasonable for this wide moat business. Shares trade at 15.9x forward earnings, a slight discount to the industry average of 16.1x.

Conclusion

McDonald’s continues to see solid same-store sales growth and strong earnings growth despite rising input costs. The company also generates exceptional cash flows that is has been using to aggressively buy back shares and raise its dividend. For investors looking to add some stability to their portfolios during the recent market turbulence, MCD looks like a smart choice.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply