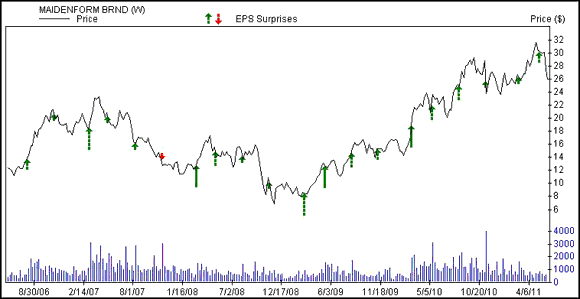

The earnings surprise winning streak continues. Maidenform Brands, Inc. (MFB) recently reported Q1 results and surprised on the Zacks Consensus for the 14th consecutive quarter. This Zacks #1 Rank (strong buy) is still cheap, with a forward P/E of only 12.1.

Maidenform Brands sells intimate apparel, including shapewear (items that women, and some men, wear underneath clothes that make you appear thinner), at department stores and other retail outlets in 64 countries.

It offers various recognizable brands such as Maidenform, Control It!, Flexees, Inspirations, Sell Expressions and Sweet Nothings. The company also produces the DKNY and Donna Karan licensed brands.

Shapewear Is Still Hot

For the last several years, sales of shapewear have been boosting the company and that story was no different in the first quarter of 2011.

On May 11, the company reported first quarter results which saw shapewear sales soar 25.9%. But other segment sales weren’t too shabby either which combined to push net sales up 14.5% to $163.6 million.

It was the 9th consecutive quarter of sales growth.

Department stores and national chain store sales rose 8.5%, mass merchant net sales rose 31.5% and international sales climbed 27.9%.

Maidenform Surprised By 10.7%

Maidenform easily kept its earnings streak alive as it surprised on the Zacks Consensus by 6 cents. Earnings per share were 62 cents compared to the consensus of 56 cents.

The earnings surprise chart is impressive when you remember that there was a recession in the middle of it.

Full Year Guidance Affirmed

While the company is still bullish about the full year, it kept its prior earnings guidance of $2.15 per share intact.

Consequently, the analysts didn’t have to do much to their estimates but the full year estimate did rise by a penny to $2.15 per share after the earnings report.

That is earnings growth of 10.6%.

Another 12% earnings growth is expected in 2012 as the Zacks Consensus rose to $2.41 from $2.38 in that time.

Valuations Still Attractive

Maidenform shares have been affordable for months, despite recently trading near new 52-week highs.

In addition to a P/E under 15, which I use as a “value” cut-off, it also has a price-to-book ratio of 2.9. That is just within the value parameters of under 3.0.

Its other fundamentals are also solid, including a 1-year return on equity (ROE) of 25.6%.

Maidenform Brands is still delivering strong sales and earnings growth along with the value.

MAIDENFORM BRND (MFB): Free Stock Analysis Report

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply