It’s been ten days since the Social Security annual report to Congress has come out. I’ve been waiting for the devotees of SS to write something cheery about the report. For the most part the cheerleaders have been silent. That’s with good reason. The report stunk. There’s nothing in it to write home about.

The exception has been one of the principal defenders of SS. Dean Baker of CEPR wrote this article. The headline intends to create an air of optimism.

I got a chuckle when I got to the part where Dean spells out what he thinks is the “good news”:

In the 2011 report the trustees assumed that we would enjoy substantially longer life expectancies than they did in the 2010 report.

I would agree with the notion that extending average life is “good news”. But, as Dean goes on to explain, this increase in longevity is just more bad news for SS. Dean describes the increase in life expectancy as the “main” reason for the financial deterioration at the Fund. That’s simply not correct. There is evidence of deterioration in all the fundamentals at SS. The bottom line is: Not even one of SS strongest defenders can find anything positive to say.

I think that the SS defenders are in shock. They have held up the annual report for decades and each time said:

“See! It’s solid as a rock!”

But they can’t say that any longer. The Trustees (finally) acknowledged that the SSTF had entered a period of perpetual annual cash deficits. This is a very critical milestone and the Trustees of the Fund didn’t see it coming. They missed this tipping point by six years.

A reader sent me this summary of the Trustee’s prior estimates of when we would cross into the dark zone of deficits. They missed by a mile, is all I can say.

2011 – shortfall is permanent

2010 – shortfall is a one year occurrence, then back to cash flow positive

2009 – shortfall begins 2015 (6 yrs away)

2008 – shortfall begins 2017 (9 yrs away)

2007 – shortfall begins 2017 (10 yrs away)

2006 – shortfall begins 2017 (11 yrs away)

2005 – shortfall begins 2017 (12 yrs away)

2004 – shortfall begins 2018 (14 yrs away)

2003 – shortfall begins 2018 (15 yrs away)

2002 – shortfall begins 2017 (15 yrs away)

2001 – shortfall begins 2016 (15 yrs away)

2000 – shortfall begins 2016 (16 yrs away)

The question that has to come to mind is, “If the Trustees missed the first critical milestone on this slippery slope, how much faith should we put into their “Drop Dead Date” where SS runs out of money?”

IMHO one should put little faith in that 2036 estimate. It could be a decade earlier.

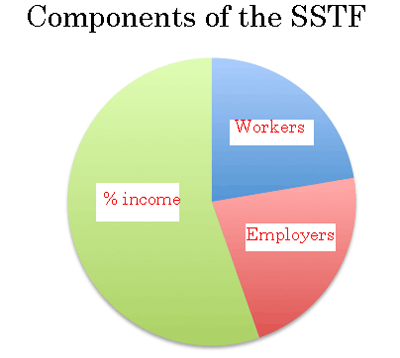

A big “Pro SS” argument you hear is that there is a big surplus in the Trust Fund. That this Fund is as big as it is because workers have been paying into it for years. “They deserve the money back”, is the thinking. At the end of 2010 the Fund was, in fact, very big. It stood at 2.6 Trillion. But who actually did contribute all that dough? Not what you think.

The SSTF has enjoyed cash receipts greater than expenses for years. These annual surpluses were invested in Treasury Bonds. The Trust Fund is equal to the sum of prior year surpluses + interest (and interest on interest). If you apportion the prior years surpluses between contributions by employers and employees you get this pie (in the face) chart :

Note that interest income at the Fund is greater than all the prior year surplus taxes from workers/employers. Note that the excess payments by workers for the past 23 years comes to only 22% of the total.

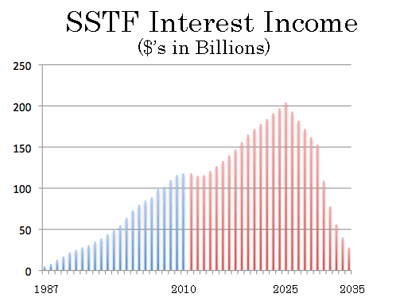

Another big lie you hear from the lovers of SS is, “SS is self funding, it doesn’t add to the deficit”. This is simply a false statement. Every penny of interest paid to the Fund is expensed in the current year budget. It is a very big number today. It gets scary big in the future. This looks at past and projected future interest due to SS from taxpayers (SSTF “Intermediate” or Base case assumptions).

The annual toll reaches $204b in 2025 (up from $118b in 2010).

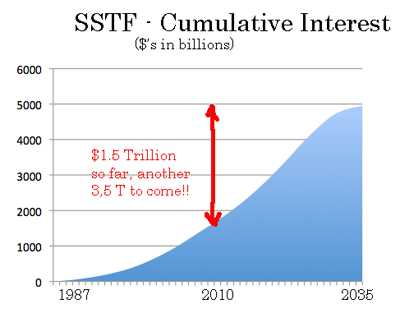

Now add it up. From inception (1987) to “big bang” (2036) the interest tab will come to a very lumpy $5 trillion. The bulk of that ($3.5 Trillion) is staring us in the face.

I don’t have a problem with the notion that the workers who contribute to SS should get a fair return on their money. But as you look at the SS picture and realize it is so highly dependent on interest income, it has to raise some red flags. Central to this is the question, “How fair is that “Fair” rate that SS has (and will) receive?”

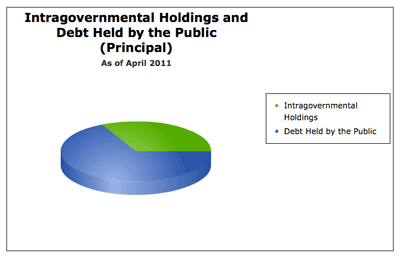

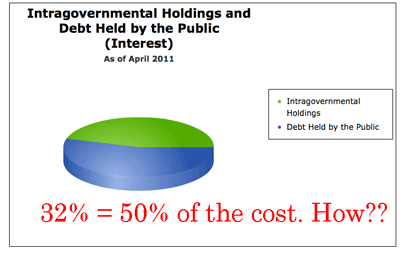

I think that the fairness issue is (and has been) a problem. The way the system works there has been a subsidy. Consider these two charts from the US Treasury and decide if this looks fair to you.

Note: The $4.6T Intergovernmental account consists of SS, Civil Servants Retirement Fund and Military Pension Fund. All of these Funds enjoy the same implicit interest subsidies from general taxpayers:

The intergovernmental liabilities represents only 32% of total debt, but the interest expense in nearly 50%. There’s something very wrong with that.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

The quote from the summary says

“The 0.30 percentage point increase in the OASDI actuarial deficit and the one-year advance in the exhaustion date for the combined trust funds primarily reflects lower estimates for death rates at advanced ages, a slower economic recovery than was assumed last year, and the one-year advance of the valuation period from 2010-2084 to 2011-2085.”

But the full trustee report confirms that the demographic factors (-.14) were by far the largest change in “Table IV.B9.—Reasons for Change in the 75-Year Actuarial Balance”

http://www.ssa.gov/OACT/TR/2011/IV_B_LRest.html#400766

The second largest was economic factors at -.06 percentage of taxable payroll

One of the reasons that the trust funds get more interest is that the publically held debt have shorter maturities.

http://www.treasurydirect.gov/govt/rates/pd/avg/2011/2011_04.htm