The President of the United States has hit commodity investors. Several Senators, the Attorney General, the CFTC and most of the other global exchanges have joined in. I think they are all pointing fingers in the wrong direction. It’s the Federal Reserve that is behind all the speculation of late. Let me throw out some raw numbers to make a point:

(I) Copper futures on the CME have seen average volume of 50,000 contracts a day this year. Each contract is for 25,000 pounds. Therefore the average turnover of copper at just the CME is 570,00 tonnes. The annual global consumption is 20mm tones so Copper futures at the CME (alone) are equal to 5.7Xs total world consumption (200 day trading year).

(II) CME corn futures trade at a rate that is 10Xs global consumption of 861 million tones.

(III) CME wheat turns over 5Xs global consumption.

(IV) NYMEX Crude volume is equal to trade at 5Xs total global consumption of 32 billion barrels barrels.

Let me emphasize that these are all global commodities. There are active exchanges in many other financial centers. There are also private transactions. Finally, there are over-the-counter derivatives and ETFs for all of these commodities. The average traded volume in the US futures market(s) is an average multiple of 5-8Xs of global consumption. The total world financial turnover is at least twice and possibly 3Xs that which is evident from US futures data. (For example consider crude and London ICE trading. Recent volume in crude trading at ICE is by itself an additional 6X’s global consumption.) What this means is that a barrel of oil is traded back and forth (mostly on paper) 15-20 times before it is consumed. The sum of the global financial ins and outs for just crude would be ~$60 Trillion.

The fact that commodities are traded 10-20 times their consumption is confirmed (to me) when looking at FX global volumes. The CLS data (interbank trading only, no futures or derivatives) shows that FX trading is $4 T a day. That comes to $800T per year or about 13Xs total global GDP of $62T.

Does this make sense to you? Is it necessary? Is it desirable? Is it controllable? What’s causing it? I’ll try to answer these important questions.

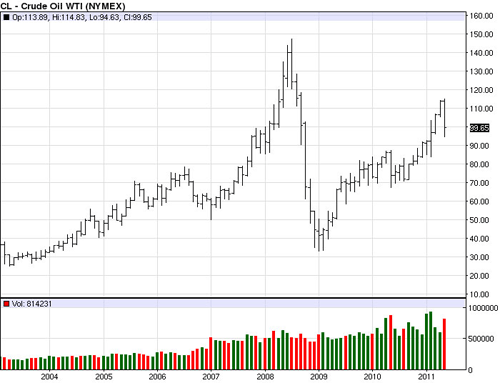

* No, it doesn’t make sense. These numbers are far higher than the historical norm. Consider this chart that shows long-term NYMEX crude trading volume. Volume is up 200-300% versus what was happening in 2004/05.

* No, it’s not necessary. The volume that a commodity is traded is directly correlated to the uncertainty of the price dynamics of the underlying commodity. The higher the uncertainty the greater the volume. There is a great deal of uncertainty today regarding the future path of commodity prices, but there has always been uncertainty (and volatility) so I am not convinced that the sharp increase in the volume of trading is justified based exclusively on risk factors.

* No, it is not desirable. We have seen in just the past few months how crude prices have performed. They raced higher, and then they collapsed. In my opinion a great deal of the volatility was related to increased trading and not to real changes in the underlying dynamics of supply and demand. Higher volatility in prices results in (net) higher prices to end-users. Consumers are paying a pretty penny for the resulting added on risk-premium.

* Finally we come to the critical question of what’s causing this? I maintain that the increased trading and the resulting volatility in key global commodities is the Federal Reserve. Zero interest rates (and QE) have eliminated the cost of owning commodities to near zero. Not only is their no financial penalty (interest expense) to finance a physical position there is a financial incentive to participate in the commodity market. When interest rates are zero, money will seek out a higher return. This reality is the basis of current Fed policy. The Fed wants people to take money from their checking and money market fund and put it to a more useful purpose. The Fed is happy when that “useful purpose” is to buy stocks or junk bonds. The Fed and the rest of world should not be surprise that another “useful purpose” is hard assets like commodities.

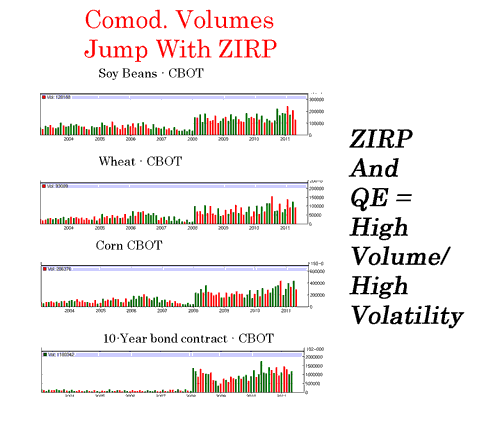

Consider this review of longer-term volume in the futures markets. They all show a big jump in volume around 2008. That is ZIRP at work:

The President can yell all he wants. He can sick the Attorney General on the players. The CFTC (and all the other exchanges) can play around with margin rules all they like. Those Senators making a fuss are crying to the moon. None of these steps will make a damn bit of difference.

If the President of the United States truly believes that volatility/speculation in commodities is a problem that has reached a critical level and that the situation requires policy response(s) he should call Ben Bernanke and tell him to raise the Federal Funds rate to 2%. That would solve the problem as far as excess speculation goes. But it will not happen as Bernanke has his foot planted firmly on the ZIRP gas pedal.

ZIRP causes all manner of speculation. It’s insane to think that Bernanke can target this powerful force so that it only has positive effects like boosting stocks and corporate bonds. With those pluses come some minuses.

If the country wants cheap money and strong equities it also has to have overvalued commodities and high volatility of prices.

You can’t have one, and not the other. Blame the Fed for the speculation, not the speculators who have been drawn to the light that Ben Bernanke is shining.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply