Patrick Lawler, Chief Economist at the Federal Housing and Finance Agency spoke to the House Sub-Committee on Capital Markets the other day (pdf Link). He said some interesting things. My conclusions after reading it are:

-If you own a home, you are screwed. Values are not going to recover anytime soon.

-If you are trying to sell a home, you are screwed. The number of qualified buyers and the availability of mortgage money are going to fall.

-If you are trying to buy a home, you are screwed. To get a mortgage you can afford is going to get harder to find in the near future.

Part of the Dodd Frank FinReg Bill was to require mortgage originators/syndicates to retain 5% of the risk. This is the “skin in the game” concept. It makes perfect sense. It is designed to minimize the amount of stinky mortgages that can be originated. It’s hard to argue with the intent of this rule. But there will be consequences.

Dodd-Frank defined what a good mortgage should look like. They call it Qualified Residential Mortgage (“QRM”). There are stiff hurdles to this definition. EVERY other mortgage (None-QRM) are subject to the risk retention rules. QRM loans are not subject to the new rules.

So what constitutes a QRM? Like I said, its stiff:

*Minimum 20% down.

*Mortgage Insurance can’t be used to make up for the shortfall of real equity by the buyer.

*Owner occupied only.

*Mortgage debt service to income no greater than 28%.

*No prior defaults, judgments or BKs need apply. You have to have a long-term clean financial record.

*Only straight 30-year mortgages meet the QRM definition. No balloon payments, no interest only, no negative amortization.

In my opinion, if these standards were in existence starting around 2000 we would never have had the blowup in real estate that nearly killed us. There would have been no funny money mortgages. There would not have been the insane run-up in prices. Therefore the proposed new rules would significantly reduce the risk of another blowout in mortgage land. But talk about taking the punchbowl away. How many legitimate (qualified) buyers are left standing when the new rules are applied? The answer is very few.

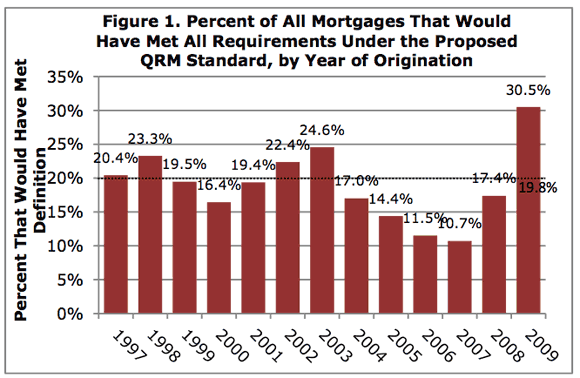

This chart shows the percentage of loans that were originated in the past that met the new standards of QRM.

Note in this chart that the average number of loans that met the QRM standards from 1997-2003 was only 20%. When you look at the number for 2007 (11%!!) you understand why we had a crisis. Fully 89% of all mortgage written were, well, junk. For me, the most significant number is the 35% for 2009. There was a substantial tightening of mortgage standards, but the amount of “bad” versus “good” was still 2 to 1. As the new retention rules take hold the availability of Non QRM will dry up.

What are the prospects for a potential buyer to get a Non QRM loan? In my opinion it will be slim. If it’s available at all, it will be expensive. Mr. Lawler points to the fact that Jumbo mortgages (loans that are too large for Fannie or Freddie to purchase) are today available at a cost of about 60 basis points over Non Jumbos. But Jumbos are high quality loans. There is significant equity and stable borrowers behind them. Therefore the pricing for a Non QRM that is smaller than a Jumbo has to be greater than the Jumbo by a significant margin.

If the cost of a new QRM is X% then the Non-QRM pricing will be at least 100bp over QRM levels. This suggests that Non-QRM will have a yield 150 – 200 over ten-year treasuries. I will leave it to the reader to plug in an estimate for the 10-year over time. Today it is only 4.4%, meaning that mortgage costs for the vast majority of borrowers would be 6.4%. Get the 10-year to a more reasonable 5% and mortgages will cost 7% for the average borrower.

Does it matter if the borrowing cost for 60-70% of all potential buyers is 1% higher? Is that a big deal? You bet it is. Does this mean that residential real estate has to collapse? No, but you would also have to conclude that there is very little upside to home ownership. There goes the American dream.

Note:

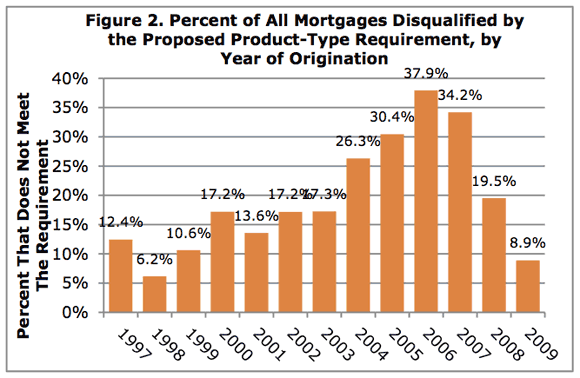

Dodd-Frank defines QRM and also Non QRM. It also establishes “None Qualified”. These are true junk mortgages. No Docs, Liars, No equity etc. These types of loans would not be eligible for syndication or Agency purchase, period. This, of course, would be a very good thing. There should be no tolerance for these types of loans. Right? Well this chart shows just how many loans would have been deemed Non-Qualified (junk) from 1997 through 2009. This chart staggers me. In 2006 38% of all mortgages were just junk. What were those lenders thinking of? Greed comes to mind.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply