This should be a short post. QE2 — for the most part, the Fed has bought shorter nominal (non-inflation protected) Treasury notes. Now, we knew from the beginning that the Federal Reserve would buy the grand majority (94%) of its nominal bonds 10-years and shorter. Also, 97% of the bonds would be nominal, and only 3% TIPS. That makes some sense, because the Treasury bond market has an average maturity of around 5 years, and the Fed’s intended purchases of nominal bonds work out a little longer than that, at 6.5 years.

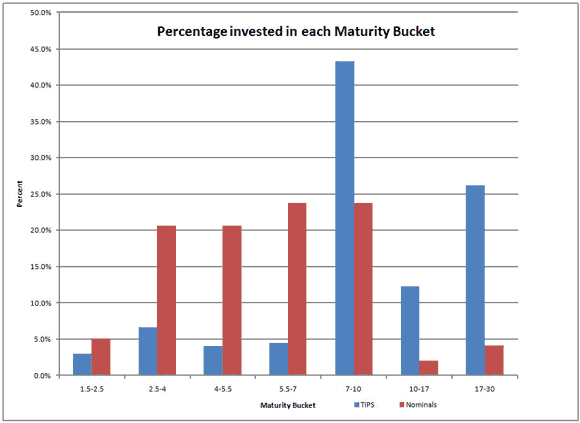

With TIPS the Fed left itself free to do whatever it wanted with respect to maturity. So far, the NY Fed has done ten purchases of TIPS — $16.1 billion worth, which would indicate they are 89.5% of the way to their (perhaps approximate) $18 billion dollar target. Let me summarize in a graph the purchases of TIPS to date, together with the targets for nominal Treasury purchases:

Average maturity for TIPS purchases is 14 years, versus 6.5 for nominal bonds. As you can see in the graph, below seven years, more nominals are bought than TIPS, and vice-versa above seven years. TIPS purchases are also concentrated in on-the-run 10- and 30-year bonds, which constitute 37% of all TIPS purchased. On-the-run bonds are the ones most recently issued, and more actively traded. They may have a disproportionate effect on the market as a whole.

What are we to make of this? It’s not as if the Fed is avoiding longer nominal bonds; their purchase profile is longer than that of the Treasury market as a whole. But with TIPS, the Fed is buying a disproportionate amount of the long end. Why? Possible reasons:

1) Maybe the Fed is no brighter than the average schmo, and can’t bring itself to buy many bonds with a negative yield versus the CPI.

2) Perhaps the Fed anticipates higher inflation in the distant future, and is purchasing a small hedge.

3) Maybe the Fed is trying to make long-term inflation expectations look high, for reasons that are not obvious to me.

I lean toward reason 2. Reason 3 is dumb. Reason 1 is too easy; the Fed has made so many errors in the past — but that doesn’t mean that will continue to do so.

The correct answer is not known with certainty; the main thing I want to highlight is that the Fed is disproportionately purchasing long TIPS. If you can tell us why, please comment so that we all might benefit.

Leave a Reply