Retail Sales were in line with high expectations for February. Total retail sales rose 1.0%, and are up 8.9% from a year ago. January was revised up from 0.3% growth to 0.7% growth. That was a major positive surprise.

The Retail Sales report covers far more than just the shopping malls and is a very broad-based measure of consumer spending. Since consumer spending makes up 71% of the economy it is a very important number. That overstates things a bit since retail sales are mostly about the sale of goods, not services, and services make up two thirds of what consumers spend. Still, it is a pretty important thing to watch.

Auto sales were a bit of a help to overall retail sales in February, rising 2.3% on the month, after rising 1.2% in January (revised up significantly from 0.5%). On a year-over-year basis they were up a whopping 23.7%.

Excluding autos, retail sales rose 0.7%, up from the January rise of 0.6%, and that was after the December number was revised up from a 0.3% gain. Year over year, sales are up 6.0%. The consensus was looking for a 0.6% rise on the month, excluding autos. So this is a minor positive surprise. The year-over-year numbers are pretty robust.

Breakdown by Category

The growth was uneven. The report tracks 13 major categories of stores, of which ten were up and only three down on the month. Year over year, eleven of the types of stores are showing increases, ranging from 2.6% (General Merchandise stores) to 23.7% for the auto dealers like CarMax (KMX). The auto numbers also include the parts stores like AutoZone (AZO).

The only stores showing a decline were the Electronics and Appliance stores, where sales were down 2.2% from a year ago, and Furniture Stores, posting a 4.0% year over year decline. The retail sales data is adjusted for things like the season and the number of shopping days, but not for price changes. Electronics is one area where prices routinely fall.

Excluding the car lots, the highest year-over-year growth (12.9%) was at the gas stations. With the price of gasoline surging, that is mostly about higher prices, not about people driving more, or a sudden increase in the number of people buying 44 oz fountain drinks. Non-store retailers, a group that includes mail order and on-line firms like Amazon.com (AMZN) were also very strong, with sales up 12.6% year over year.

For the month, the auto dealers (and parts stores) were also the strongest category with a 2.3% increase, on top of a 1.2% rise in January. The miscellaneous store group was in second place with a 2.0% increase, up from a 0.5% rise in January. That group is also very solid on a year-over-year basis, with sales up 10.5%. Gas stations took the Bronze with a 1.4% increase, on top of a 1.3% rise in January.

The worst performers on the month were the furniture stores, where sales fell 0.8% for the month, after a 1.5% decline last month. The January number was revised down sharply from a previously reported decline of just 0.3%. Apparently, the Presidents Day sales this year were a bit of a bust. Times are still tight, and there are few purchases that are as easily deferrable as buying a new dining room table. Housing (both new and used) sales are normally a major driver for furniture sales, and it is no secret that the housing market remains depressed.

The two other groups showing declines are the non-store retailers, where sales were down 0.3% on the month — though that is after a 1.5% surge in January, and the group is still very strong on a year-over-year basis. Drug stores like Walgreen’s (WAG) were also down 0.3% on the month, after being up 0.6% in January. On a year-over-year basis, drug stores are sort of in the middle of the pack, up 5.4%.

Food Inflation Apparent?

With all the chatter about food inflation breaking out, one would expect to see a big pop in Grocery store sales. That was not really the case, as sales were up 0.6% for the month, down from a 1.4% increase in January. Year over year, sales were up 3.4%, well below the overall increase in retail sales.

That is a bit of an indication that fears of food price inflation are a bit overblown. Certainly food commodity prices are way up, but raw commodities make up a pretty small part of the nation’s shopping cart. The price of wheat is a very small part of the cost of a loaf of bread, for example.

Food price inflation has not a big long-term problem, at least not here in the U.S. In other parts of the world, higher food prices are a serious problem, and many analysts have pointed to higher food costs as one of the key sparks to the unrest in Tunisia and Egypt, which is spreading to other parts of the Middle East.

Electronics & Appliances

Sales at Electronics and Appliance stores such as Best Buy (BBY) rose by 0.9% on the month after having fallen 0.2% in January. That was a big downward revision from an original increase of 0.3%. As I noted above, aside from furniture, it is the only category of stores where sales were below year-ago levels.

The appliance side of those stores suffers from the same problem as the furniture stores: low housing sales. In addition, electronics is one area where prices routinely fall, so some of the weakness is probably due to price, not volume. New electronic gizmos are also purchases that can be easily deferred.

Sporting goods and hobby stores saw sales rebound, with a rise of 1.3% reversing a 1.0% drop in January. Year over year they are up 5.0%, which is a bit below average. Sales at building materials and garden center stores such as Home Depot (HD) also rebounded from a bad January. Sales were up 0.6% after being down 1.3% last month.

More significant for the group, though, was a big upward revision to the January numbers. It was first reported as a decline of 2.9% in January. This is one area where the harsh weather is a plausible reason for the weak sales in that month. On a year-over-year basis, the category is strong, up 10.9%.

Given how weak the construction industry has been, up 10.9% from a year ago is a very strong showing, but then again, a year ago things were pretty depressed. It may also be that people are spending more to spruce up their existing place, rather than move into new homes.

Other Discretionary Spending

Clothing stores like The Gap (GPS) also had a good sales month, with sales up 0.8%. Here again, though, the bigger story is the revisions to the January number. Clothing store sales are now seen as having been up 0.9% in January, while they were first reported as a drop of 0.3%. Relative to a year ago they are up 3.8%, which is decidedly below average. A new pair of jeans is a bit less discretionary than a new kitchen table, but more discretionary than going to the grocery store.

General merchandise stores, a category that includes the department stores, saw a 0.7% increase on the month, matching its January increase. Year over year, general merchandise sales are up 2.9%, so sales are generally on the soft side at the mall anchors as well as the stores in the periphery of the mall.

Going out to eat and drink is also a very discretionary item, and sales at bars and restaurants were up a strong 1.2%, a sharp acceleration from the 0.1% increase in January. Once again, the revisions were a key part of the story, as previously we thought sales at restaurants were down 0.7% in January. Year over year things are still on the soft side, with sales up 3.8%.

Report Card: B/B+

Overall, this is an encouraging report. While the strong numbers for the month were anticipated, the upward revisions to last month’s numbers were not.

The retail sales report is at times very interesting when it shows a clear divergence between spending in discretionary spending items and on staple-type stores. That was not really the case this month. Autos are highly discretionary, but it is clear that Detroit is on the rebound (at least metaphorically, I’m not so sure about the city itself). Going out to eat is also discretionary, and the Bars and Restaurants had a good month.

On the other hand, the very discretionary furniture store category remains very soft. The non-discretionary areas were mixed, with grocery stores doing OK, but drug store sales soft. Gas station sales were strong, but that is more likely a story about prices, not volumes.

This report suggests that consumer spending will be a solid contributor to GDP growth in the first quarter. This report, taken in isolation, would tend to push up forecasts of first quarter GDP growth, offsetting the disappointing trade report we got yesterday (see “Trade Picture Gets Ugly“).

The upward revisions to last month are particularly significant in that regard. It is clear that the effects of the blizzards in January were not as significant as first thought, but there might also be some rebound effect going on. People prevented from shopping due to the weather in January were going out to the stores in February.

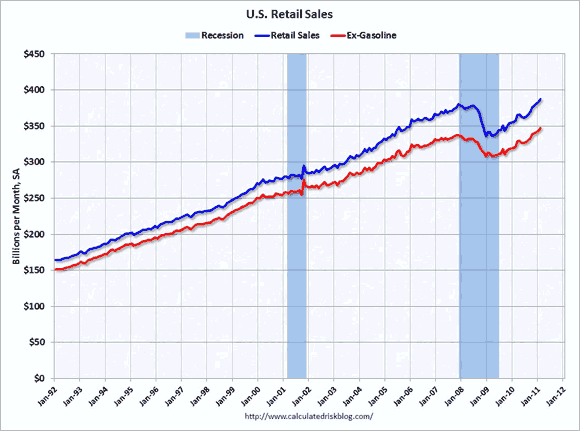

The graph below (from this source) shows the longer-term path of retail sales, both total (blue line) and excluding sales at gas stations (red line). In both cases we are at new highs, but recall that these numbers are not adjusted for inflation. While inflation is still very low, over the course of a few years it still plays a significant role.

The pace of growth since the bottom (slope of the lines) appears to be slightly better than what prevailed prior to the Great Recession, but it was not a very fast snap-back — more like a reset to a lower level than a continuation of the previous growth rate from a lower level.

The ex-gasoline numbers are probably a better reflection of the overall state of the economy than the total numbers, but both are telling a pretty similar story. Things are getting better, but slowly.

HOME DEPOT (HD): Free Stock Analysis Report

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply