1995 was one of my favorite years. Silicon Valley had been in a funk for over a decade, with a fading memory of the last tech bubble, the PC IPO craze that flamed out in 1983 but launched some really great companies. The peace dividend from the fall of the Berlin Wall had impacted engineers in local defense companies (remember the movie of a laid-off defense worker in LA going postal?), and an area-wide initiative called Joint Venture:Silicon Valley was formed to revitalize the place. Was Silicon Valley already over?

Then along came the Netscape IPO and the dot-com boom was born. It ran for five more years.

This time around our Netscape is Facebook, and it has its own social network of other high-profile IPOs. LinkedIn, Groupon, Twitter and Zynga are expected to go out before Facebook gets forced out by our SEC by April 2012.

The question du jour is will it spark the next great tech boom, and the most encouraging (nea joyous) answer is that people are still skeptical. They expect this bubblet to burn off fast and for Silicon Vallley to sink back into the abyss of the past decade. The herd was also full of skeptics in 1995, and in 1996, and 1997; it was only after the eBay IPO in 1998 that the stampede began and people opined that this time it was different. Of course it wasn’t, but the Nasdaq doubled from late ’98 to early ’00.

I led a local panel two weeks ago, with VCs squaring off against Angels and SuperAngels. When asked whether the slew of social IPOs would spark a new boom, they demurred and said these would be one-off events, like Google was – special companies that get out, not the start of another bubble. This attitude is good news; in 1999 the same sorts of opinion leaders would have said they know things are nuts but they have to keep investing to keep up. (You can look that up – a real quote from a well respected VC.) It is the attitude of greed, which is just fear – fear of falling behind.

Point is, we are still in “1995”, not “1999”.

Last week, however, the new tech boom began to be recognized. It started at GigaOm, where their European commentator asked whether we could avoid another bubble, and answered that we have already been in one for 20 months, it just hasn’t been recognized. Then the inestimable Om Malek compared some of the bubbilicious valuations (Twitter at $10B!!) with the salaries paid to baseball stars by the Yankees. He made them make sense. (If you have been following this blog, you know that for the past year I have reported on ever-rising valuations of SuperAngel startups, the signature of a new tech boom.)

The recogniton began building across the week, with Dick Kramlich of NEA telling Bloomberg how the coming social IPOs would be the first blockbuster IPOs since the ’90s! (NEA invested in Groupon when it was called ThePoint, at a normal venture valuation, before it ran to over a Billion Dollar value two years later.) It culminated with a report across the wire at MarketWatch about here comes dot-com 2.0!

The MarketWatch gushy wire got me worried, so I scanned more news items, and breathed a sigh of relief. The general thrust of the commentors is still coming in skeptical. The SF Chronicle ran a piece today about the incipient bubble, and concluded that the skepticism is curbing the hype. The head of the very successful incubator, Y Combinator, calmly explained that there is no tech bubble, since unlike the ’90s, almost all of these companies have real business models (Twitter excepted). Mark Cuban, who became an overnight billionaire in the dot-com bubble by selling a Broadcast.com to Yahoo for $5.7B, a business which then promptly disappeared, expressed disdain, calling this not a bubble but a “pyramid scheme“; he would know! Paul Kedrowsky, an industry watcher, opined late in the week that Facebook is not a bubble value, and it could go higher in secondary-market trading before its IPO.

Ok, this ‘we don’t believe it yet” got me comfortable again, until I saw the advance cover for next week’s Fast Company: Mark Pincus, CEO of Zynga, will grace it. CEOs are back, as celebrities – we haven’t seen that since 1999!

The problem: it is well known that when a magazine like Sports llustrated shows a star quarterback after a big game, he is likely to bomb the next week. Getting on the cover of Sports Illustrated was the kiss of death for a sports star. In the 1990s, getting on the cover of Inc had the same impact. Is Pincus peaking?

This weekend the WSJ laid the issue to rest. We are not like 1999 in one huge respect: money is leaving venture capital, not rushing in. This is not a general bubble but a narrow-based boom, with VC fundraising still very challenging, leading to haves and have-nots in the VC world. In the late 1990s, investors were piling money into VC firms. This time, especially because they use 10-year returns to allocate capital, capital is still leaving the venture world, not rushing into it. (VC ten year returns are really bad compared with other asset classes. The technical term is that VC ten-year returns have sucked, big time.) This actually bodes very well for future VC returns, as less money chasing these funds should make the brave & the few still moving into VC very successful.

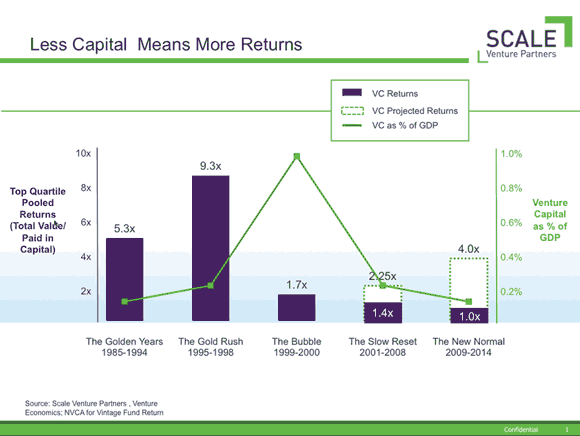

I discussed this with Rory O’Driscoll of Scale Ventures (formerly Bank of America Ventures). Rory is one of the great thinkers in this industry. He does his homework and respects numbers, as you can see from his blog VC Matters. He constructed the following chart, which shows how VC returns do best when VC finds are on a diet, and he expects future returns to rise:

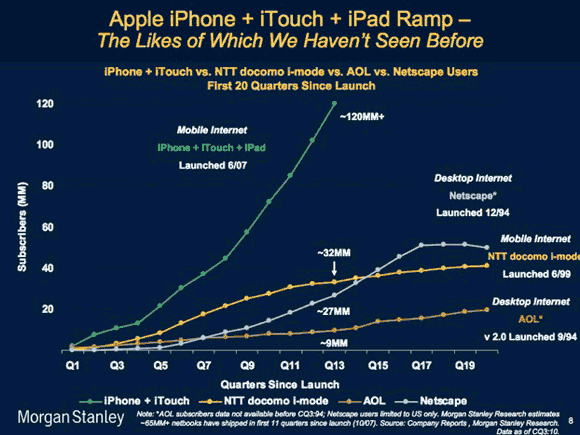

Curiously, no one has yet named this era. I call it the Social/Mobile/Web, and while the social web has dominated to date, the mobile side is shaping up to be huge. Mary Meeker was one of the great analysts of the dot-com bubble, and now she is at Kleiner Perkins, dong what she does best. Her latest work shows how the next decade will be shaped by the new face of mobile. From her point of view, it is 1996 all over again.

Leave a Reply