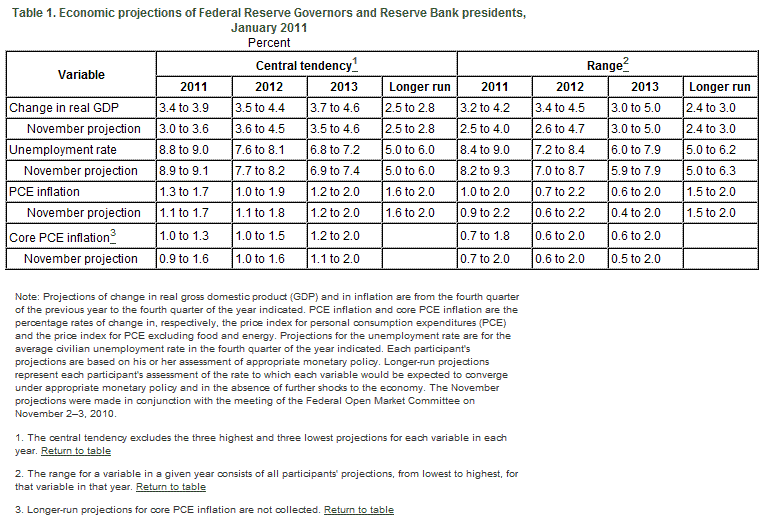

The minutes for January meeting for the FOMC, the branch of the Federal Reserve Board that determines the direction of monetary policy, are out. The GDP outlook by the FOMC was revised higher to 3.9% ; the unemployment rate was revised down and projected to decline gradually. Meanwhile, the rate of inflation — going from 1.3-1.7%, up from 1.1-1.7% — is still forecast to be below the Fed’s 2% target.

Here are few excerpts of the January FOMC meeting:

Participants’ Views on Current Conditions and the Economic Outlook:

“While participants viewed the downside risks to their forecasts of economic activity over the projection period as having diminished, their assessment of the most likely outcomes for economic activity and inflation over the projection period was not greatly changed. Most participants raised their forecast of real GDP growth in 2011 somewhat and continued to anticipate stronger growth this year than in 2010, with a further gradual acceleration during 2012 and 2013. The unemployment rate was still projected to decline gradually over the forecast period but to remain elevated. Total inflation was still expected to remain subdued, and core inflation was projected to trend up slowly over the next few years as economic activity picks up but inflation expectations remain well anchored.

On the risks:

Participants generally saw the risks to their outlook for economic growth and employment as having become broadly balanced, but they continued to see significant risks to both sides of the outlook. On the downside, participants remained worried about the possible effects of spillovers from the banking and fiscal strains in peripheral Europe, the ongoing fiscal adjustments by U.S. state and local governments, and the continued weakness in the housing market. On the upside, the recent strength in household spending raised the possibility that domestic final demand could snap back more rapidly than anticipated. If so, a considerably stronger recovery could take hold, more in line with the sorts of recoveries seen following deep economic recessions in the past.

Regarding risks to the inflation outlook, some participants noted that increases in energy and other commodity prices as well as in the prices of imported goods from EMEs posed upside risks. Others, however, noted that the pass-through from increases in commodity prices to broad measures of consumer price inflation in the United States had generally been fairly small.

On the pace of QEII:

In their discussion of monetary policy for the period ahead, members agreed that no changes to the Committee’s asset purchase program or to its target range for the federal funds rate were warranted at this meeting….The Committee decided to maintain its existing policy of reinvesting principal payments from its securities holdings and reaffirmed its intention to purchase $600 billion of longer-term Treasury securities by the end of the second quarter of 2011…A few members noted that additional data pointing to a sufficiently strong recovery could make it appropriate to consider reducing the pace or overall size of the purchase program. However, others pointed out that it was unlikely that the outlook would change by enough to substantiate any adjustments to the program before its completion.”

Some forecasts:

Leave a Reply