How did the rating agencies come to have such a prominent role in the regulation of securities? This column traces their history back to the Great Depression. Ironically, the agencies became a regulatory instrument to address concerns about securities originators’ conflicts of interest, the very problem plaguing the agencies today. The lesson may be that no fixed regulatory solution is durable in the long run.

The role of rating agencies in setting the stage for the financial market turmoil that erupted in mid-2007 has been hotly debated. While arguments had for some time been made that the ratings process for structured financial instruments exacerbated conflicts of interest, the origins of the recent crisis in securitisations of sub-prime mortgages has provided further impetus to the debate. Frank Partnoy (2001, 2006), a fierce critic of the role of rating agencies, has provided an energetic accusation of the agencies’ role.

Vox columns by Charles Goodhart (2008) and Richard Portes (2008) have echoed these views. Central to current discussions of the role of rating agencies in adding to the subprime mess is the notion of “regulatory license”. Back in the 1930s, it is said, regulators provided agencies with a captive market, and this “original sin” is the cause of most of our subsequent troubles.

In a recent CEPR discussion paper, we revisit this view using new data for the interwar period (Flandreau et al 2009). We explore the performance of rating agencies during the Great Depression, when they became involved in regulation. Rating agencies had been around for a while (Moody’s started operating before WWI) but in 1931, in the midst of extensive fire sales of assets that threatened banks’ solvency, US authorities decided that banks supervised by the Comptroller of the Currency (the supervisory body that was in charge of dealing with so-called national banks in the US) would be enabled to book investment-grade securities at face value rather than at market price.

Why were rating agencies involved at that stage? One possibility is that they had provided early warnings of the looming disaster, or that they had done a particularly good job at picking out defaulters. If this were true, then they might have been credible instruments of certification and risk management by regulators. Other authors have also implied that, since rating competition was free and the agencies were brand-conscious, they possibly worked harder during the 1920s (than in today’s decrepit world of regulatory rents) and managed to secure the respect of market participants and regulators.

However, our study of performance, which for simplicity we limited to sovereign debt issued in New York, fails to find any evidence of superior forecasting capacities by the agencies. While we have some results suggesting that brand concerns played a role (for instance, Standard Statistics, a new market entrant, tended to be more conservative than competitors), we do not find any clear evidence of a superiority of rating agencies over “alternative” market forecasts such as bond prices. Of course, it could be that the information in bond prices during the 1920s reflected ratings but then the whole point that the use of ratings in regulation in the 1930s changed their influence in a radical way is void.

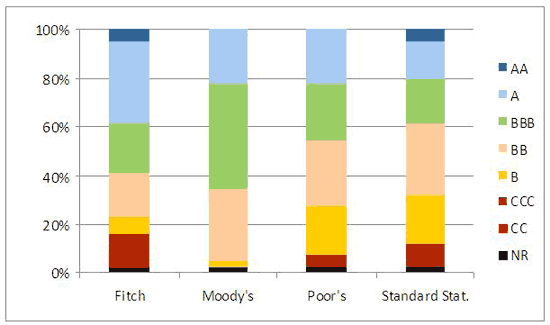

Figure 1. Ratings composition one year before the default

(1920-1939, 44 defaulted issues)

Source: Author’s computations.

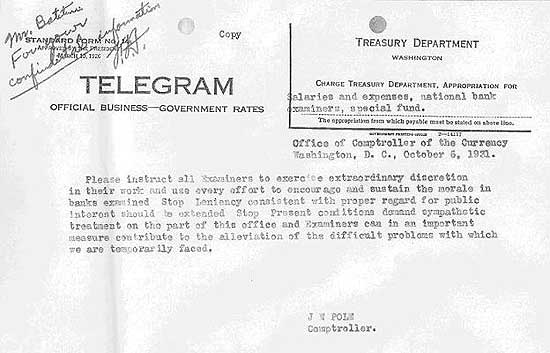

What then, explains the emergence of rating agencies as a regulatory instrument that persists today? Our research shows that the 1931 measure was part of a comprehensive strategy through which the US Treasury sought to provide relief to banks in the midst of what was identified as a liquidity crisis. Booking at face value, we computed, gave a boost to balance sheets. For corporate securities the valuation effect was 16.7% (A) and 32.8% (Baa). For foreign government securities, the corresponding numbers ranged between 75.6% (A) and 82.1% (Baa). Thus rating agencies were called in as a tool for fostering forbearance. In a telegram we found and reproduce below, examiners were further instructed to “exercise extraordinary discretion in their work and use every effort to encourage and sustain the morale in banks examined” (see Figure 2). As a result, more banks would be able to report healthy balance sheets, with the expectation that this would prevent a further collapse (this proved wrong).

Figure 2. Document from US Treasury Archive

But again, this per se does not explain why rating agencies were privileged by regulators over other instruments to promote forbearance. For instance, regulators could have used bond prices at the time of issue as a possible alternative. Our investigation revealed that what caused the emergence of rating agencies as a pillar of regulation was the perceived conflict of interest that investment banks and commercial banks involved in origination suffered at the time. It was perceived that bankers were “banksters” and had been unable to resist conflicts of interest between their role as originators and their role as gatekeepers of liquidity. As a result, the public suspected that the prices at which securities had been issued were likely to have been manipulated. Certification and regulatory intervention had to rest on some assessment of “value” that would be as far away from the origination process as conceivable. Rating agencies provided just this.

The rest of the story is well known. In doing this, regulators dragged the agencies closer to the core of the origination of new securities, which eventually proved damaging for their reputation. While some will emphasise the irony of now blaming the agencies for the very sins that caused their emergence in the first place, we suggest that there must be deep reasons for history to go in circles. And whatever they are, the lesson must be that there is no long-run, simple, and sustainable regulatory fix for our current troubles.

Disclaimer: The views expressed in this column are those of the authors only and do not reflect neither the views of their co-author in the research quoted nor those of the Bank for International Settlements.

References

•Flandreau, Marc, N. Gaillard and F. Packer, (2009), “Ratings Performance, Regulation and the Great Depression: Lessons from Foreign Government Securities”, CEPR Discussion Paper 7328.

•Goodhart, Charles A.E. (2008), “The Financial Economists Roundtable’s statement on reforming the role of SROs in the securitisation process”, VoxEU.org, 5 December 2008.

•Partnoy, Frank (2001), “The Paradox of Credit Ratings”, UCSD Law and Economics Working Paper.

•Partnoy, Frank (2006), “How and Why Credit Rating Agencies Are Not Like Other Gatekeepers”, in Yasuyuki Fuchita, and Robert E. Litan (eds.), Financial Gatekeepers: Can They Protect Investors?, Brookings Institution Press and the Nomura Institute of Capital Markets Research.

•Portes, Richard (2008), “Ratings agency reform”, VoxEU.org, 22 January 2008.

![]()

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply