The Institute for Supply Management’s (ISM) manufacturing index surged to 60.8 in January from 58.5 in December. This was also a positive surprise as the consensus had been looking for the index to come in at 58.2. The December number was also revised sharply higher from its original reading of 57.0.

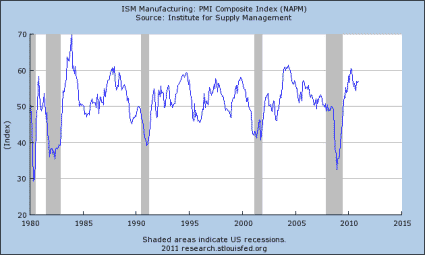

The overall index last matched this level in January of 2004, and the last time that it was higher than this was back in April of 1984. This is a “magic 50 index” where any reading over 50 indicates that the manufacturing side of the economy is expanding and any reading under 50 indicates a contraction in manufacturing. The overall index has now been above the magic 50 mark for 18 straight months.

The key takeaway from this number is that the manufacturing sector is expanding, and doing so at a faster rate than in December. This reading is extremely strong by any historical perspective. In fact, it has been matched or exceeded in only 89 months since the start of 1948, or 11.7% of the time. Almost all of those instances are ancient history.

Since 1980, the current level has been matched or exceeded only 11 times, or less than 3% of the months. Unfortunately, the St. Louis Fed is a bit slow in updating its numbers this morning, so the graph below does not include the new data. The graph shows the history of the overall index for the last 30 years.

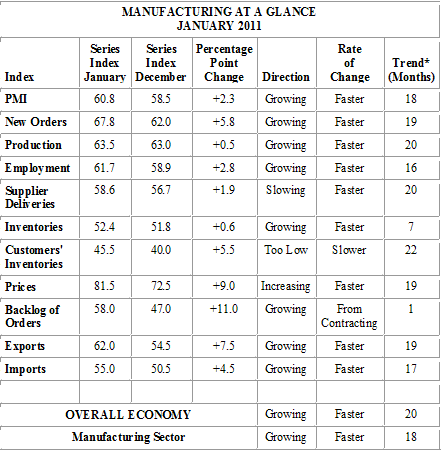

The ISM index has a very long and venerable history, it used to be known as the Purchasing Managers Index or PMI. The overall index is made up of ten sub-indexes. All of the indexes showed improvement over last month. Nine are above the magic 50 level, the index tracking purchasing managers views of their customers inventories is the only exception.

The sub-indexes are as interesting as the overall index. When one digs below the headline number, this is a very solid report. In terms of the current state of the economy, the most important of these is the production index. It rose 0.5 points to 63.5, which is the highest it has been since last May.

Production

The production index has been in positive territory for 20 straight months now. Thirteen industries reported an increase in production while three saw production fall in January.

Backlog of Orders

However, the index with the biggest impact on the very short term is the backlog of orders, and there the picture is one of sharp improvement. The order backlog sub index soared 11.0 points, the greatest increase of any of the sub-indexes. That is a good thing since order backlog had been one of the problem areas having spent four straight months below the 50 level.

The current reading is the highest since last May. Ten industries reported an increase in January, while four reported declines.

New Orders

Looking just a bit further out, as existing orders in the backlog are worked off, they need to be replaced with new orders. The new orders sub-index thus gives us the best view of where things will be in the next few months. The new orders index climbed to 67.8 from 62.0.

In other words, new orders are flooding in to the nation’s factories. New orders have been on the rise for 19 straight months now. This is the highest level for this sub-index since January of 2004. Twelve industries reported higher new orders while just three reported a decline in new orders.

Employment

With unemployment at 9.4% in December, and expected to remain there or even tick up a bit when the employment report comes out on Friday, the employment sub-index is of particular interest. The employment index rose to 61.7 from 58.9 in December.

The employment sub-index has been above 50 for 16 straight months now. Eleven industries reported an increase in employment while only two reported declines. The last time the employment sub-index was this high was way back in 1973!

Prices Paid Index

The prices paid index rose 9.0 points, and remains at the highest overall level, at 81.5, of any of the sub-indexes. This is a very clear indication that deflation is not around the corner, as some of the other price indexes like the CPI have seemed to be indicating.

Most of the prices paid in this index though tend to be commodities, not final goods. Still, the high prices paid sub-index is be ammunition for those who are critical of Federal Reserve’s quantitative easing program.

The general rule on the sub-indexes is that the higher they are the better, but this sort of level is a bit worrisome, and could raise fears of overheating. Given the rest of the data out there, I’m not terribly concerned about that. Even though the level is very high, we were higher on this sub index as recently as July of 2008.

Foreign Trade

The ISM index also gives a bit of a glimpse into the foreign trade situation. It seems to be indicating an improvement in the trade deficit. The index tracking new export orders rose 7.5 points to 62.0 while the index tracking imports rose 4.5 points to 55.0.

However, the import figure only refers to imports of materials or components that domestic manufacturers use, not to finished goods. Still, the figures seem to point to further improvement in the trade deficit and net exports. Net exports were a huge boost to GDP growth in the fourth quarter, subtracting 3.44 points from growth.

In other words, if the trade situation had remained unchanged from the third quarter, GDP growth would have been negative in the fourth quarter, not +3.2%. Thus, this sign of further potential strength in net exports bodes well for GDP growth in the first quarter.

Report Card: A+

Overall, this was an outstanding report. It was slightly better than the consensus expectation, and the overall level is consistent with an economic boom in the making, not a return to recession. It is at highs that have rarely been seen over the last 30 years.

Three of the four sub-indexes that I consider to be most important — Production, New Orders and Employment — are not just above 50, but above 60. The fourth, Order Backlog, is not that far off the pace at 58.0, and had the biggest increase of any of the sub-indexes. The table below is from the ISM report and provides the summary information.

It’s nice to see lagging indicators that support your hypothesis. This is exactly what we should see in the early to mid stages of inflation. People are erroneously looking to rates for inflation, but it’s going to look different this time.