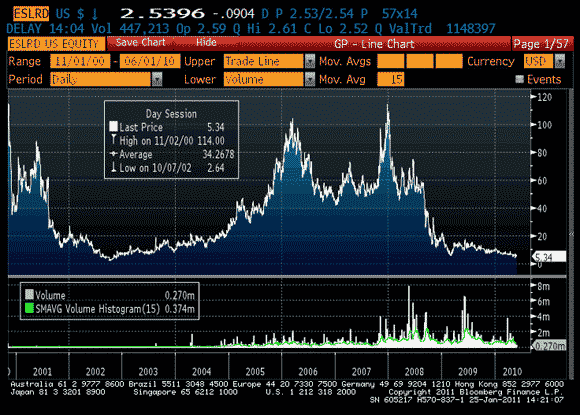

The average return of an asset is merely looks at the price. one can argue whether geometric or arithmetic averages, but let’s ignore that here. Look at the firm ESLRD, Evergreen Solar. They make solar power cells, so it’s a sexy product, one very amenable to sales pitches of the next black swan that rubes do not fully appreciate. It came out in November 2000, with $112MM of insider money, and $42MM from outsiders via their IPO. the price (split adjusted) was $84.

The price fell over the next couple years, then rebounded in 2006 and 2007, and lately collapsed, and is now trading at $2.50. They have never made money. In 2006 revenue peaked at $103MM, up sharply from 2005, which instigated the bounce in stock around that time. Alas, it did not continue, and revenue has fallen, and it appears they will never be viable (current market cap is only $87MM).

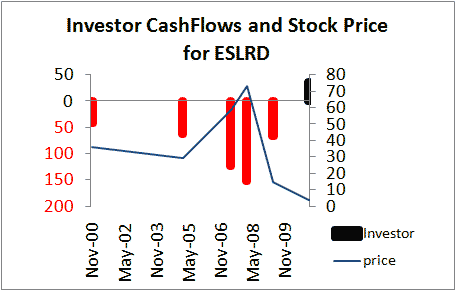

Unfortunately for investors, their total of $446MM worth of injections were not random, but rather at relative stock highs, such as in 2007 and 2008. Look below and the red lines are investor contributions, and the black line at the end is their total value of those red lines today. If you look at the Internal Rate of Return. The internal rate of return on an investment or project is the “annualized effective compounded return rate” or discount rate that makes the net present value (NPV) of all cash flows (both positive and negative) from a particular investment equal to zero.

It’s especially useful when analyzing funds, because often they have incubation periods with little money, and they are presented only if successful, a clear selection bias. Then, they muddle along. But if they made 50% their first year with $10MM (their equally prescient yet less fortunate peers lost money and never went live), and then made 5% the following 6 years when they had $250MM under management, allowing them to look like all-stars based on top-line returns.

In contrast, most stock data merely looks at the return of stocks independent of cash flows, the annualized return is around -10%, consistent with a stock going to zero over 10 years. But the Internal Rate of Return was -47%, much worse. This is the average return to your average dollar that came in, weighted by how long it was there. It is a much more accurate picture at what an average investor endured.

Clearly in cases of failed companies, they generally will have much lower IRRs than ‘average rates of return’. Ilia Dichev (2005) looked at a variety of indices, and equity net inflows, and found this adjustment reduces returns by 1.3% for NYSE/AMEX for the period 1926-2002, 5.3% for Nasdaq from 1973-2002, and 1.5% for 19 major international stock exchanges from 1973-2004. Applying this correction to the entire market is something that is never done in all those ‘stocks for the long run’ or Ibbotson analyses.

Why don’t these experts recognize this bias? Well, economists hate to do anything that decreases their best example of the risk premium, the elusive thing that explains everything and nothing; it is implied by their basic conception of utility used everywhere, and so they can’t simply turn it off. As to index providers, every one of them has a vested interest in indices they catalog, they are not disinterested providers of information. Just as Moody’s used to selectively present their default data (note that munis and asset backed securities are separated from corporate defaults?), the major index providers have a strong vested stake in having their product look good.

Leave a Reply