William Cline and John Williamson published on Vox an interesting piece earlier this month June 18), titled “Equilibrium Exchange Rates,” in which they try to “estimate a set of medium-run fundamental equilibrium exchange rates compatible with moderating external imbalances” for the 30 largest economies. They assume that a sustainable equilibrium trade balance for the US implies a current account deficit of 3% of GDP (this is conservative – I would have thought “equilibrium” would have been lower), and try to estimate the amount of currency change needed to get there. They also assume that in general not just the US but all “countries should strive to keep imbalances (surpluses and deficits) under 3% of GDP.”

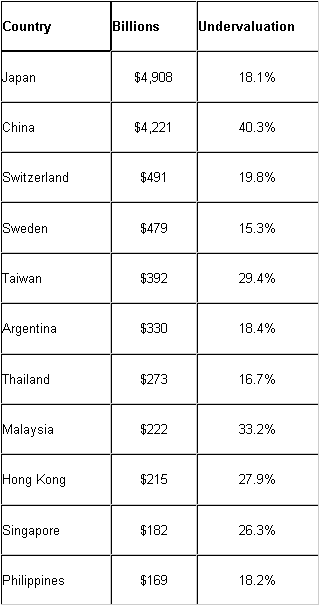

Using early June 2009 exchange rates, they find that six countries – most of whom are primarily commodity exporters, not coincidentally – have overvalued exchange rates relative to the dollar (Australia, New Zealand, South Africa, Brazil, Colombia, Mexico), and twelve, mostly in Europe, have currencies that are marginally undervalued. Of the 30 countries, eleven have currencies that are at least 15% undervalued relative to the US dollar. For convenience sake I include their 2008 GDP and rank them by size. (right)

Using early June 2009 exchange rates, they find that six countries – most of whom are primarily commodity exporters, not coincidentally – have overvalued exchange rates relative to the dollar (Australia, New Zealand, South Africa, Brazil, Colombia, Mexico), and twelve, mostly in Europe, have currencies that are marginally undervalued. Of the 30 countries, eleven have currencies that are at least 15% undervalued relative to the US dollar. For convenience sake I include their 2008 GDP and rank them by size. (right)

Economists can, and of course will, dispute the methodology and the extent of any perceived under- or over-valuation, but in my opinion the most valuable aspect of these exercises is not that they indicate the “correct” exchange rate level, whatever that means, but rather that they can indicate trends or signal interesting anomalies in the aggregate. Two things are noteworthy here, I think.

The first, and most obvious, is that eight of the eleven Asian countries within the top thirty economies (the exceptions are India, Indonesia, and Korea, whose currencies are all undervalued by 4-6%) are on the above list of significantly undervalued currencies, and the list is dominated by them (eight Asians out of eleven countries on the list). This simply suggests the not-exactly-controversial thesis that Asian countries have systematically undervalued their currencies as a strategy to generate employment growth. It also suggests that Asian central banks that worry about the impact of dollar weakness on their reserve holdings are in the funny position of having created the dollar overvaluation at the same time they were actively accumulating those overvalued dollars.

The second noteworthy consequence of their exercise, which I found much more interesting, was a finding that the authors seem to find a little surprising. They say:

The main counterpart to the overvalued dollar is the undervaluation of the Chinese renminbi, along with a few of the smaller Asian currencies. We are somewhat nervous because our estimate (based on the figure of RMB 4.88 to the dollar) of Chinese undervaluation is even larger than it was a year ago (RMB 5.81 to the dollar), despite the fact that the RMB rode the dollar up by 14% in effective terms in the intervening year. It may be that our estimate is now too large because the IMF’s projection of the Chinese surplus seems not to have declined despite the RMB’s real appreciation, although the fall in commodity prices in the past year has presumably worked in China’s favour. But all the other potential biases, notably the way of formulating the Chinese current account target as a substantial surplus rather than the deficit suggested by the FDI inflow, are in the direction of minimising estimated undervaluation. Our analysis is one more piece of evidence that the major macroeconomic imbalance in the world today stems from China’s exchange-rate policy.

Leaving aside the fact of their very high estimate of Chinese undervaluation, I think the authors are saying that although the RMB rose 14% from the last time they calculated these equilibrium exchange rates, nonetheless their measure of the adjustment needed to balance trade suggests that the RMB is actually even more undervalued than it had been a year ago.

What’s going on? How can a currency that has risen 14% against the dollar finish even more undervalued against the dollar? Part of the answer could be differential productivity growth rates, and since Chinese productivity is growing faster than US productivity it would imply that the RMB should revalue against the dollar just to maintain equilibrium. But of course there is absolutely no way Chinese productivity grew by even a fraction of the amount necessary during that time to explain this anomaly.

But remember in my June 3rd post I argued that we make a mistake when we think only currency and tariff policies can affect trade? There is a whole list of policies that, by directly subsidizing production or by implicitly or explicitly taxing consumption, will necessarily affect the trade account. Could it be that even as the RMB was nominally revaluing, other policies were implicitly “devaluing” the RMB – i.e. policies that implicitly increased subsidies to production, and/or taxed consumption – so that the net distortionary impact on trade actually increased? That could explain why a revaluing RMB is nonetheless consistent with an even more undervalued RMB in relative terms.

New lending surges

We are getting reports that June lending numbers are up on May. One of the more bizarre pieces of “good news” recently – very popular among the China bulls – were claims that new lending had moderated significantly in the past two months (so don’t worry too much about that credit bubble everyone’s talking about), but this is true only to the extent that new loans in April and May were compared to the astonishing first quarter numbers. In fact net new lending in April and May was around double the equivalent amounts last year and every year in this decade.

In June, it looks like we are retuning to an upward trajectory. According to an article in the current issue of Caijing:

Commercial bank lending in the first half is expected to hit 6.5 trillion yuan, with new loans in June coming in at about 660 billion yuan, the official Shanghai Securities News reported, citing people close to the matter.

Chinese banks lent out a record 4.6 trillion yuan in the first quarter to help start stimulus projects; while there has been a slowdown since April, the central bank says its policy remains “moderately loose.” Experts have warned against lending quality, unauthorized loan diversions, and the re-emergence of bad loans, which may cause banks to be more cautious in lending in the second quarter.

Discussing the impact of all this lending Andy Xie weighs in with another thoughtful and worried piece in the current issue of Caijing. He writes:

China’s credit boom has increased bank lending by more than 6 trillion yuan since December. Many analysts think an economic boom will follow in the second half 2009. They will be disappointed. Much of this lending has not been used to support tangible projects but, instead, has been channeled into asset markets.

Many boom forecasters think asset market speculation will lead to spending growth through the wealth effect. But creating a bubble to support an economy brings, at best, a few short-term benefits along with a lot of long-term pain. Moreover, some of this speculation is actually hurting China’s economy by driving asset prices higher.

The current surge in commodity prices, for example, is being fueled by China’s demand for speculative inventory. Damage to the domestic economy is already significant. If lending doesn’t cool soon, this speculative force will transfer even more Chinese cash overseas and trigger long-term stagflation.

He goes on to say:

The international media has been following reports of record commodity imports by China. The surge is being portrayed as reflecting China’s recovering economy. Indeed, the international financial market is portraying China’s perceived recovery as a harbinger for global recovery. It is a major factor pushing up stock prices around the world.

But China’s imports are mostly for speculative inventories. Bank loans were so cheap and easy to get that many commodity distributors used financing for speculation. The first wave of purchases was to arbitrage the difference between spot and futures prices. That was smart. But now that price curves have flattened for most commodities, these imports are based on speculation that prices will increase. Demand from China’s army of speculators is driving up prices, making their expectations self-fulfilling in the short term.

I usually don’t quote so much from a single source, but I think Andy Xie’s piece is a very good one and well worth reading (there is a lot more). He makes many of the arguments that all of us who worry about China’s continuing failure to adapt to the huge adjustment in the global and US economies. His conclusions:

What is happening in the commodity market is glaring proof that China’s lending surge is hurting the country. Even more serious is that it is leading Chinese companies away from real business and further toward asset speculation – virtual business.

…Many analysts argue GDP growth follows loan growth, and inflation is a problem only when the economy overheats. This is naive. Borrowed money channeled into speculation leads to inflation. And China may face a lasting employment crisis if private companies don’t expand.

This lending surge proves China’s economic problems can’t be resolved with liquidity. China’s growth model is based on government-led investment and foreign enterprise-led export. As exports grew in the past, the government channeled income into investment to support more export growth. Now that the global economy and China’s exports have collapsed, there will be no income growth to support investment growth. The government’s current investment stimulus is tapping a money pool accumulated from past exports. Eventually, the pool will dry up.

If exports remain weak for several years, China’s only chance for returning to high growth will be to shift demand to the domestic household sector. This would require significant rebalancing of wealth and income. A new growth cycle could start by distributing shares of listed SOEs to Chinese households, creating a virtuous cycle that lasts a decade.

Putting money into speculative investments isn’t totally irrational. It’s better than expanding capacity which, without export customers, would surely lead to losses. Businesses currently lack incentive to invest. But many boom forecasters wrongly assume that recent asset appreciation, fueled by speculation, signaled an end to economic problems. That’s an illusion. The lending surge may have created more problems than it resolved.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply