The jobs report was a clear disappointment relative to both expectations at the beginning of the week and certainly after the blowout ADP report. After adjusting expectations to the upside, ADP once again scores a major miss (how we came to care about this data series still remains a mystery to me). That said, the overall tenor of fourth quarter employment reports suggest an economy growing around trend growth. Better, but not good enough to prompt a policy response from the Fed.

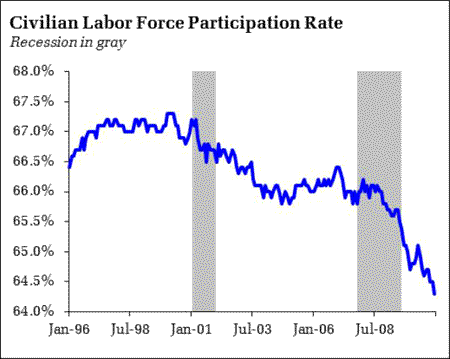

The headline NFP gain was 103k overall, 113k private. Consensus had been looking for something around 140k at the beginning of the week. On the upside, the BLS revised up the October and November numbers, so that the average monthly NFP gain during the fourth quarter was 128k, pretty much right in the middle of the 100k to 150k estimates of growth required to keep a lid on unemployment. And the unemployment rate did more than hold steady – it retreated, falling from 9.8% to 9.4%. The improvement, however, is less positive than at first blush. Persistently high unemployment continues to drive workers out of the labor force, illustrated by a fresh decline in the labor force participation rate:

The report internals were not particularly reassuring if one is still looking for the fabled V-shaped recovery. Gains in wholesale and retail trade as well as transportation and warehousing were consistent with the generally solid consumer spending news during the quarter. But the biggest gainer was the ever consistent health care sector, which added 37.1k. Something of a disappointment was the deteriorating trend in the rate of temporary help gains – the sector added just 15.9k jobs, down from 31.1k in November and 28.6 in October. Weekly hours, both average and aggregate were unchanged, while hourly wage gains were a minimal 3 cents.

In short, nothing to change the direction of monetary policy, a point reinforced by Federal Reserve Chairman Ben Bernanke’s Senate testimony today. Although Bernanke begins with a nod to the recent data:

More recently, however, we have seen increased evidence that a self-sustaining recovery in consumer and business spending may be taking hold. In particular, real consumer spending rose at an annual rate of 2-1/2 percent in the third quarter of 2010, and the available indicators suggest that it likely expanded at a somewhat faster pace in the fourth quarter. Business investment in new equipment and software has grown robustly in recent quarters, albeit from a fairly low level, as firms replaced aging equipment and made investments that had been delayed during the downturn.

his ultimate conclusion remains unchanged:

Although it is likely that economic growth will pick up this year and that the unemployment rate will decline somewhat, progress toward the Federal Reserve’s statutory objectives of maximum employment and stable prices is expected to remain slow. The projections submitted by Federal Open Market Committee (FOMC) participants in November showed that, notwithstanding forecasts of increased growth in 2011 and 2012, most participants expected the unemployment rate to be close to 8 percent two years from now. At this rate of improvement, it could take four to five more years for the job market to normalize fully.

Bernanke continued his defense of large scale asset purchases, explaining the importance of ongoing monetary easing given the persistent deviation of unemployment and inflation from the Fed’s mandate. He also emphasizes that this policy is ultimately temporary and not equivalent to unbounded government spending:

As I am appearing before the Budget Committee, it is worth emphasizing that the Fed’s purchases of longer-term securities are not comparable to ordinary government spending. In executing these transactions, the Federal Reserve acquires financial assets, not goods and services. Ultimately, at the appropriate time, the Federal Reserve will normalize its balance sheet by selling these assets back into the market or by allowing them to mature.

Bernanke then places himself, again, in the middle of the fiscal policy debate. Should this be the purview of the Fed Chair? Does it invite Congress to meddle with monetary policy? Is this a reflection of Bernanke’s political affiliation, his desire to take sides with fellow deficit hawk Republican’s? Interesting that Bernanke continues the tradition of blaming retirees for the nation’s fiscal challenges:

In subsequent years, the budget outlook is projected to deteriorate even more rapidly, as the aging of the population and continued growth in health spending boost federal outlays on entitlement programs. Under this scenario, federal debt held by the public is projected to reach 185 percent of the GDP by 2035, up from about 60 percent at the end of fiscal year 2010.

By linking the aging population and health care costs in the same sentence, he sends the message that the old are sick and consequently the cause of the impending crisis. I would have preferred that he explicitly separated rising health care prices we all face from the issue of the aging population.

Bottom Line: The employment report was lackluster, consistent with expectations the US economy is operating – sustainably – around trend growth. The report was also consistent with the view that this just isn’t good enough to rapidly alleviate the hardships imposed by the recession. The lack of more dramatic improvement in labor markets keeps the idea of policy tightening off the FOMC’s table, and while I can envision the Fed bringing a halt to large scale asset purchases when the current program is complete, given the employment and inflation data, I can’t wrap my mind around a rate increase this year.

Leave a Reply