The current investor sentiment is still getting a lot of press around the blogosphere, almost always picking out the rapid increases in bullish sentiment and it’s most probably negative (contrary) implications for the market’s short- and intermediate term performance. According to an exclusive CNNMoney survey (32 experts participated), stock market experts (investment strategists and money managers) expect the S&P 500 to rise 11% (on average) in 2011, and not one of them thinks the S&P 500 will close at a lower level at the end of the year.

This survey seems in full compliance will the latest poll from the Market Vane Bullish Consensus., which was reported at 62% for the week ending December 31, 2010, the highest level since November 9, 2007. The Market Vane Bullish Consensus is compiled daily (but is available on a weekly basis as well) by tracking the buy and sell recommendations of leading market advisers and commodity trading advisers (CTA) relative to a particular market (in this event the stock market), and reflects the open positions of the advisers and CTAs as of that day’s market close.

As Rennie Young from MarketTells already showed, this group is regularly on the right side of the market, and consecutive readings above | below the 50% mark do more often have positive | negative implications for the market’s intermediate- and long-term performance (but not necessarily over the short-term).

But the question is: Will too many (CTA) bulls really make a bear (market) ?

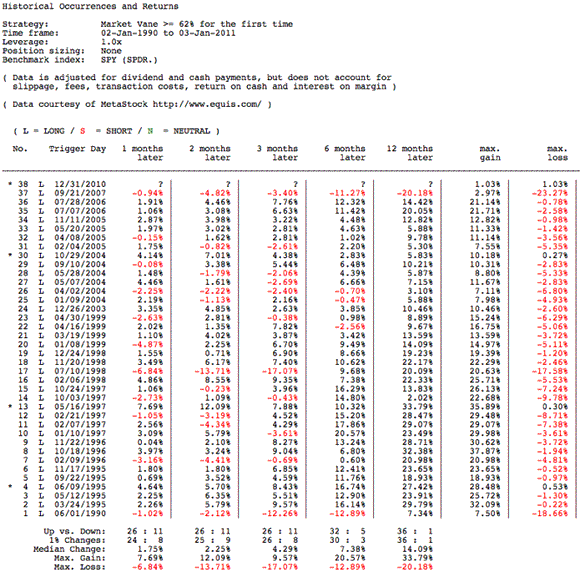

Table I below shows all occurrences (since 1990) and the market’s performance over the course of the then following 1 , 2 , 3 , 6 and 12 months, assumed one went long of the last session of a week (like on December 31, 2010) where the Market Vane Bullish Consensus was reported at or above the 62% mark for the first time (means no consecutive readings were accounted for).

When the the Market Vane Bullish Consensus was reported at or above the 62% mark for the first time in the past, …

- … probabilities (winning percentage) and odds (median return) for a higher close 1 to 12 months later always surpasses the market’s at-any-time probabilities and odds for a higher close 1 to 12 months later ;

- … the SPY ( S&P 500 SPDR) closed at a higer level 6 and 12 months later on 32 (or 86.50% of the time) and 36 (or 97.30% of the time) out of 37 occurrences, with one exception only during the financial crisis in 2007 ; and

- … downside (in contrast to upside) potential was regularly limited over the course of the then following 12 months ; the SPY ( S&P 500 SPDR) posted a double-digit (temporary) drawdown (≤ -10.0%) on only 3 out of 37 occurrences, but a double-digit (temporary) gain (≥ +10.0%) on 31 out of 37 occurrences.

Conclusions:

As always everything is possible (not to be mistaken for ‘probable’), an imminent major correction as well the beginning of the next bear market, but the permanent repetition of a stock market adage (regularly without giving any evidence / data / statistics / listing of occurrences / …) doesn’t turn a bullish (Market Vane) sentiment poll into a bear market. And it seems cautious is warranted (being up to make any long-term bets on the short side of the market) when leading market advisers and commodity trading advisers (CTA) are heavily leaning on the long side of the market.

Disclosure: No position in the securities mentioned in this post at time of writing

Remarks: Due to their conceptual scope – and if not explicitly stated otherwise – , all models/setups/strategies do not account for slippage, fees and transaction costs, do not account for return on cash and/or interest on margin, do not use position sizing (e.g. Kelly, optimal f) – they’re always ‘all in‘ – , do not use leverage (e.g. leveraged ETFs), do not utilize any kind of abnormal market filter (e.g. during market phases with extremely elevated volatility), do not use intraday buy/sell stops (end-of-day prices only), and models/setups/strategies are not ‘adaptive‘ (do not adjust to the ongoing changes in market conditions like bull and bear markets).

(Data courtesy of MetaStock , and for data import, testing, surveys and statistics I use MATLAB from MathWorks)

Leave a Reply