I’ve just come back from two weeks on the road, during which time I attended a couple of conferences. The first conference (NBER International Seminar on Macroeconomics) dealt with issues of exchange rates, reserve accumulation and financial crises (more on that later). The second one, a joint Bank of Canada-ECB workshop (not online), focused on exchange rates in the global economy. At the latter, Jeff Frankel delivered the keynote speech, entitled “On Global Currency Issues“, in which he outlined what’s “out” and what’s “in” in international finance. One of the phenomena he concluded was no longer relevant was “the global saving glut”.

I still wonder whether there ever was a global saving glut. In part, the question hinges on one’s view of what the nature of the glut. Was it world saving was higher then they it had been before. That patently was not true (and will be even less true as government deficits rise). Was it that saving relative to investment in East Asia and oil exporting countries was higher in the early 2000’s than in the past? That view is more defensible. Yet, it’s important to recall that current account balances are endogenous variables, determined by the interaction of saving and investment in different economies, so one can’t say without further analysis whether the US current account deficit was driven by excess supply of saving from East Asia, or excess demand for saving from the United States. And we for sure know that there was plenty of pull from the US (tax-cut induced public sector ([1] [pdf] and private sector borrowing).

The strongest evidence in favor of the global saving glut explanation, so construed, is that interest rates seemed unnaturally low at roughly the same time the US current account deficit was large. Well, what’s the evidence for that assertion?

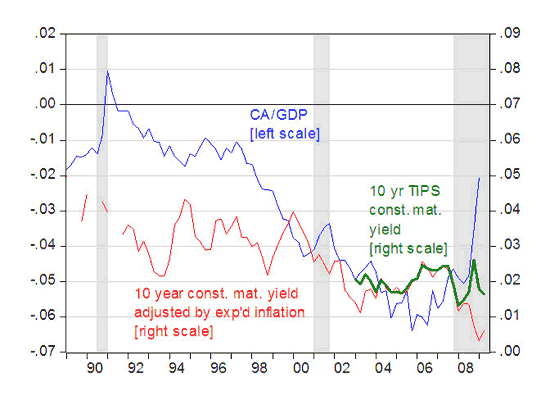

Figure 1: Current account to GDP ratio (blue); 10 year constant maturity real interest rates, calculated by using Survey of Professional Forecasters 10 year expected inflation rates (red); and 10 year constant maturity real interest rates from TIPS yields (green). NBER defined recession dates shaded gray. Source: BEA, 2009Q1 GDP preliminary release, St. Louis Fed, Survey of Professional Forecasters, and NBER.

The correlation between real interest rates and the US current account deficit has always been something I viewed as more asserted than obvious in the actual data, and that point becomes apparent in this picture. Even if one saw the correlation for a few years in the mid-2000’s, for certain the alleged correlation has disappeared for now. The US current account has begun a headlong drive toward balance, even as long term rates remain at levels comparable to those in 2004 (if one uses TIPS). The real interest rate is even lower, if one uses expectations data to convert nominal to real rates.

I think this debate is not purely academic. As Jeff Frankel points out in his speech, the question has not been completely resolved as to why the US ran such large current account deficits since 2001. On one side are those who focus on the “push” of saving from East Asia combined with the lure of incredibly sophisticated and sound US financial markets, leading to excess risk taking and leverage in the US, which in turn induced an unsustainable boom and bust episode [2]. As I discussed in this post from January, this is essentially the view propounded by the previous Administration in the last Economic Report of the President (Chapter 2).

However, I think it at least equally plausible — especially after the revelations of the frenzy to abdicate regulatory responsibility and loosening capital requirements in the previous Administration (and the resulting attendant criminal behavior) — that “pulled in” saving from the rest of the world. So my view is that the “saving glut” was more of a typical Kindleberger type of mania, combined with the Akerlof-Roemer (not Romer) type of “looting” behavior.

Whether we will have a recurrence of the US current account imbalance depends in part upon whether you hold the “push” view or the “pull” view. It also depends on whether, if you hew to the latter view, the Obama Administration and Congress can come to an agreement on a regulatory framework which quells the risk-taking and “looting” behavior we have seen over the previous eight years.

So the answer to the question I posed in the title: (1) the saving glut as an idea should indeed be put to rest; in fact (2) the saving glut was mostly a mirage, and the US current account deficit really was much more a function of a typical capital inflow boom driven by an unsustainable fiscal policy (as in Frieden (2006) and Chinn (2005)) and deregulatory disarmament than those much lauded “sophisticated” American securities markets; and (3) The saving glut did not “cause” the current economic and financial crisis; that is largely a result of our own policy errors on macro and regulatory policy of our own making.

The Global Saving Glut: Rest in Peace? Mirage? Bete noir?

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply