Retail sales surprised on the upside in October. From the Wall Street Journal:

American consumers are showing clear signs of stepping up their spending.

Retail sales rose 1.2% to $373.1 billion in October, compared with September, the largest monthly jump since March and the fourth-consecutive month of increased spending.

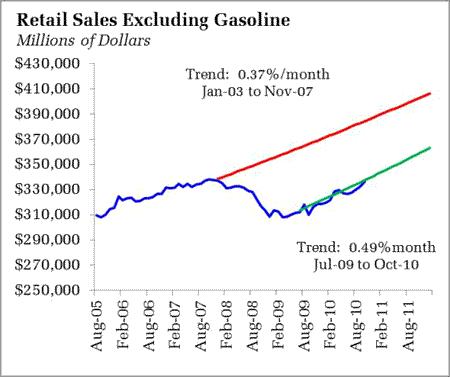

How excited should we be? It seems clear that the pace of sales has kicked up in recent months:

Another picture telling two sides of the same recovery. The recent trend line reinforces my expectation that trend growth is not out of the question. Indeed, this would only be slightly more optimistic with the most recent Philadelphia Fed survey of forecasters, which is pointing to slightly below trend growth next year. Still, even at the heightened pace of spending, there remains a gaping hole between the old and new that is unlikely to be filled anytime soon. Lots and lots of foregone consumption.

Of course, the media begins speculating on what this means for the upcoming holiday season:

This string of stronger retail reports—together with signs that businesses continue to restock shelves in anticipation of more robust sales going forward—are stirring hopes for a good holiday shopping season. The state of consumer health will get a further checkup on Tuesday, when retail giants Wal-Mart Stores Inc. and Home Depot Inc. report earnings.

I am not sure exactly what constitutes a “good” holiday season. I think that means a season where demand is strong enough to limit the necessity of discounting. It appears we have already lost that battle, as the rush to discount is already well under way. Moreover, some of the enthusiasm for the report dwindles upon reading the details:

Monday’s report pointed to particular areas of strength: Sales of autos and parts rose 5% in October, the largest jump since March. Excluding autos, which can be volatile from month to month, retail sales rose a more moderate 0.4%. Other bright spots included sales at sporting goods, hobby, book and music stores, which increased 1%. Restaurant and bar sales rose 0.3%.

But many consumers remain hesitant to go for big-ticket items that are usually bought using credit. Furniture sales fell 0.7%, for instance, as did sales at electronics and appliance stores.

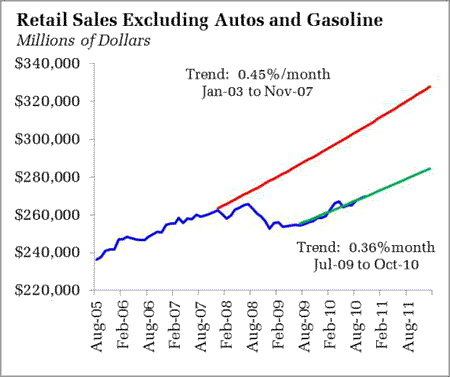

Autos were clearly driving the gains. Not entirely unexpected either. Quite honestly, while prerecession sales of roughly 16 million units annually might not be sustainable, the fall to 10 million units was equally unsustainable. Pent-up demand eventually emerges, carrying auto sales higher. Stripping motor vehicles and parts from the data yields this picture:

Here we see something closer to what some might call the “new normal” for consumer spending. Not devastating, but lackluster in comparison to the pre-recession trends.

Bottom Line: In general, the retail sales report was good news, as it is another indicator that drives a stake into the heart of the double-dip story. But keep in mind that the data continues to illustrate the good cop, bad cop conflict in the economy. Policymakers should be concerned about the distance between new trends and old, lest they risk falling into the trap of diminished expectations, believing that 9% unemployment should be the new normal. Market participants, however, may simply be content with confirmation that the foundation for ongoing corporate revenue growth remains secure.

Leave a Reply