Futures are actually up a little this morning with the “greenshoots” crowd claiming to see new buds sprouting. Of course they keep looking at a few miniscule “reduced rate of fall” data and they are somehow blind to the elephant in the garden that is trampling the hell out of their “greenshoots!” That elephant is called DEBT, and I’ll get to that in a minute.

Keep in mind that whenever we’re talking “bonds” or “Treasuries,” what we’re really talking about, of course, is DEBT. This week alone the Fed had to convince “investors” to buy up $150 billion worth of OUR debt! That has now created a Historic CRASH of the bond market with TLT, the 20 year bond fund, losing almost 30% of its value. The ten year rose to 4% and that will take 30 year mortgages well over 6%. While that may not sound like much compared to historic rates, and it’s not, because we are so saturated with debt and have financed a huge portion of our debt with short term financing, resetting to higher rates will be very painful indeed. The more debt in the system, the more painful rising rates will be.

Today at 1:00 Eastern the 30 year bond auction will take place. Yesterday’s 10 year auction didn’t go so well. So, while the greenshoot crowd is pointing out what amounts to nothing I can see, we have crashing bond markets which are a HUGE, GIGANTIC WEED in our economic garden!

So, while equities have been holding up, bonds have been crashing. One or the other, but not both!

So let’s look at some other economic data that our fine media is calling greenshoots…

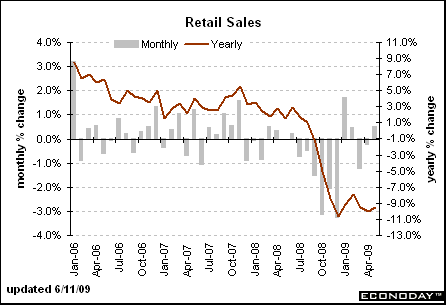

Here’s what’s happened in retail sales in April according to Econoday:

Retail sales fell another 0.4 percent in April after dropping 1.3 percent the month before as consumers retrench due to rising unemployment and tighter credit. Declines in sales were broad based. Excluding motor vehicles, retail sales posted a 0.5 percent decline, after a 1.2 percent plunge in March. Looking ahead, however, we may see an autos-led rebound in May retail sales as unit new motor vehicles sales rose 6.4 percent to 9.91 million units annualized, according to auto manufacturers. Also, higher gasoline prices likely helped bump up overall retail sales for May. The big question is how did retail sales do outside of autos and gasoline-and the latest reports from department stores suggests a down month.

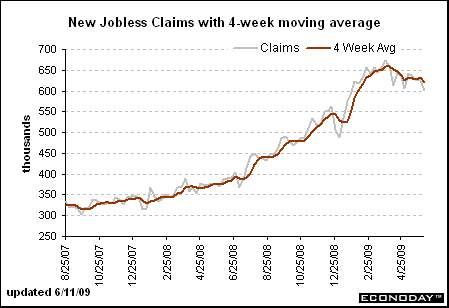

And initial unemployment claims fell to “only” 601,000. Heck, 300,000 would be BAD, 600k is horrid. Yet, amazingly this is spun into being somehow “good” because it appears the number has peaked. But, of course, when nobody in the entire country has a job, the number of new claims will fall to zero, I guess that will be a good thing! Meanwhile, continuing claims rose by 59,000 to 6.816 million!

Here’s how Econoday spun it positively:

Contraction in initial jobless claims slowed noticeably in the June 6 week, to 601,000 for a 24,000 dip (prior week revised 4,000 higher to 625,000). The improvement is clearly evident in the four-week average which fell 10,500 to 621,750 — its lowest level since February. These results will confirm global expectations that U.S. payroll contraction has already peaked.

Job losses are slowing as are increases in the number of unemployed. Continuing claims, in data for the May 30 week, rose 59,000 to 6.816 million, another record and extending a string of weekly increases that go all the way back to the very beginning of the year. But the 59,000 rise is comparatively mild and follows and a rise of only 6,000 in the prior week that is the mildest rise of the year. The unemployment rate for insured workers is unchanged at 5.1 percent.

For an ailing patient, today’s report is good news. But for holders of safe-haven securities the news, along with a stronger-than-expected retail sales report, point to higher interest rates and higher returns in other investments.

Clearly the numbers have leveled out, but the 600K area is absolutely horrid and nothing to cheer about. And they have been at this level for quite some time. The longer it stays in this area, the worse.

And since we’re no longer following the rule of law, as in lawless, capital will no longer want to form in our country to build factories and hire workers, so I would expect the employment picture to remain BAD for LONGER BECAUSE OF OUR GOVERNMENT’S ACTIONS.

You know, things like Bernanke’s latest memos showing that he absolutely was ready to remove Bank of America’s CEO had he not agreed, under pressure, to take in Merrill Lynch in the Fed’s shotgun wedding. Of course this is all stuff we know. What everyone is still missing, and that makes all of this a diversion, are the trillions upon trillions of leveraged toxic derivatives that have now accumulated at the big banks and are being hidden by the banks and our own government! Heck, even the accounting standards board (FASB) has been strong-armed in order to keep the toxic waste hidden from your view. Trust me, at some point they will see the light of day. When that day arrives, I hope you are ready, it will not be pretty!

The spring is wound very, very tightly in equities right now. We had a small change in the McClelland on Tuesday and then yesterday’s action did not produce the big move we’re looking for. That means the odds are high that there will be a big move today, direction not known by that oscillator.

In the daily and weekly timeframe stocks are WAY, WAY overbought by many measurements. But in the short term the stochastics indicate an overbought 10 minute, a mid-range 30 minute, and a 60 minute that has just exited oversold and is headed north. By those indications I might expect lower, then higher today, but anything is possible as none of them are up against extreme readings.

Right now we have the ying in stocks versus the yang in bonds. The bond market is the more powerful force, it influences capital flows and can cut off the life blood of the economy if it gets out of hand. Watch the bond market closely here. It is coming up on long term support, if it gets worse, then “bad things this way come,” as Yoda says!

Debt, our Beast of Burdon…

Graphs: Econoday

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply