Having earlier reviewed some of the reasons in favor of additional quantitative easing (QE2), I’d like to acknowledge some of the dissenting views.

(1) One concern was expressed by Edward Hugh (hat tip: Tyler Cowen):

it is no exaggeration to say that a protracted and rigourously implemented round of QE2 in the United States could put so much pressure on the euro that the common currency would be put in danger of shattering under the pressure. Japan is already heading back into recession, as the yen is pushed to ever higher levels, and Germany, where the economy has been slowing since its June high, could easily follow Japan into recession as the fourth quarter advances.

Perhaps there’s some basic issue I’m overlooking, but here’s how I see it. If other countries want to prevent their exchange rates from appreciating, they should respond with easing of their own, which from my perspective would be a win-win outcome for everybody. If other countries feel that easing is contraindicated for their domestic situation, then isn’t that part of the case why the dollar needs to depreciate relative to their currencies, given the current economic conditions in the U.S.?

(2) Stanford Professor Myron Scholes raises a separate issue:

If the Fed takes on more risk, society still has the risk. The risk doesn’t go away, any more than the risk of holding subprime mortgages went away before the crisis. We cannot structure the risk such that it disappears. Society still has the risk, and will want to hold safe assets if the Fed affects the risk premium.

I think that’s a very important observation. Here’s how Cynthia Wu and I have been thinking about this issue within the context of our recent paper claiming that the Fed could flatten the slope of the yield curve by buying more long-term bonds:

Certainly from the perspective of an individual investor, a 10-year Treasury bond has different risk characteristics from a 6-month T-bill, and these differences get priced by the market. If an individual investor changes her relative holdings of these assets, she perceives herself to have a different risk exposure, and perceives the U.S. Treasury to be the counterparty…. If the government changes the maturity structure of its outstanding debt, it is in fact committing to a different state-contingent path for spending, taxes, or inflation.

The time path of spending, taxes, and inflation are part of society’s risk structure that Scholes is discussing, and is something that we assume would have to be altered as a result of these kinds of policy choices. Our interpretation is that the average positive upward slope to the term structure comes from the historical desire of the government to pass along interest-rate risk to its creditors.

(3) Robert Waldman (along with Arnold Kling and Bob Hall) asks:

But why the Fed? The Treasury is a huge player in the bond market. They are still selling long term bonds. Why? What if the Treasury decided to finance the deficit with 1 and 3 month T-bills alone?

Again this is an excellent question, and one with which I also have struggled. In terms of my theoretical understanding of the mechanism by which large-scale asset purchases might be effective, the operation is identical whether implemented by the Treasury or the Fed. One reason one might give for having the Fed conduct the operations is the possible additional benefits of using it as a signal and framework for the conduct of future monetary policy. A second is that the primary goal of the proposal is to prevent what I regard as a harmfully low level of inflation, and targeting inflation is traditionally the responsibility of the Federal Reserve rather than the Treasury.

(4) Federal Reserve Bank of Kansas City President Thomas Hoenig has expressed the following concerns:

without clear terms and goals, quantitative easing becomes an open-ended commitment that leads to maintaining the funds rate too low and the Federal Reserve’s balance sheet too large…. rather than inflation rising to 2 or 3 percent, and demand rising in a systematic fashion, we have no idea at what level inflation might settle. It could remain where it is or inflation expectations could become unanchored and perhaps increase to 4 or 5 percent.

Again I agree that these are critical issues. At a minimum, we need to acknowledge up front the limited potential of QE2 and be prepared to admit when it has accomplished all it can. Options for limiting the commitment include targeting the 2- or 3-year Treasury yield or announcing an exit strategy based on a particular level for the core PCE, as I discussed here. I’ve also urged the Fed to keep a close eye on commodity prices through this process.

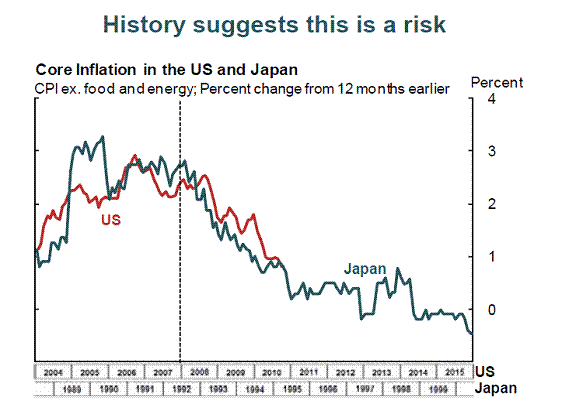

(5) A final concern is that QE2 will be ineffective in restoring full employment. Variations on this perfectly accurate statement have been made by a great number of people; for a recent collection see Yves Smith. But the issue is not, and in my mind has never been, whether monetary policy can “solve our problems”. Instead the question is whether a sufficiently low or negative rate of inflation would make our problems worse. If it would make our problems worse, then the goal of monetary policy is to avoid doing that. Here’s another reminder from the October 14 FedViews of what’s at stake:

Leave a Reply