The inability of global leaders to address global current account imbalances now truly threatens global financial stability. Perhaps this was inevitable – the dollar has not depreciated to a degree commensurate with the financial crisis. Moreover, as the global economy stabilized the old imbalances made a comeback, sucking stimulus from the US economy and leaving US labor markets crippled. The latter prompts the US Federal Reserve to initiate a policy stance that will undoubtedly resonate throughout the globe. As a result we could now be standing witness to the final end of Bretton Woods 2. And a bloody end it may be.

Of course, the end of Bretton Woods 2 has been long prophesied. Back in October 2008, Brad Setser foresaw its imminent demise:

I increasingly suspect that the combination of falling oil prices and falling demand for imported goods will produce significant fall in the US trade and current account deficit in the fourth quarter, with a corresponding fall in the emerging world’s combined surplus. The Bretton Woods 2 system – where China and then the oil-exporters provided (subsidized) financing to the US to sustain their exports – will come close to ending, at least temporarily. If the US and Europe are not importing much, the rest of the world won’t be exporting much….

And rather than ending with a whimper, Bretton Woods 2 may end with a bang….

….If Bretton Woods 2 ends in 2009 – if US demand for imports falls sharply in the last part of 2008 and early 2009, bringing the US trade deficit down – it won’t have ended in the way Nouriel and I outlined back in late 2004 and early 2005. We postulated that foreign demand for US debt would dry up – pushing up US Treasury rates and delivering a nasty shock to a housing-centric economy… it didn’t quite play out that way. The US and European banking system collapsed before the balance of financial terror collapsed.

But Bretton Woods 2 was soon reborn, as the steady improvement to the US current account deficit was soon reversed:

Bretton Woods 2 simply morphed forms. Rather than a reliance on US financial institutions to intermediate the channel between foreign savers and US households, a modified Bretton Woods 2 – Bretton Woods 2.1 – relied on the US government to step into the void created by the financial mess and become the intermediary, either by propping up mortgage markets via the takeover of Freddie and Fannie, or the fiscal stimulus, or a dozen of other programs initiated during the financial crisis.

In essence, a nasty surprise awaited US policymakers – after two years of scrambling to find the right mix of policies, including an all out effort to prevent a devastating collapse of financial markets and a what Administration officials believed to be a substantial fiscal stimulus, the US economy remains mired at a suboptimal level as stimulus flows out beyond US borders. The opportunity for a smooth transition out of Bretton Woods 2 was lost.

How has it come to this? To understand the challenge ahead, we need to begin with two points of general agreement. The first is that the US has a significant and persistent current account deficit, which implies that domestic absorption of goods and services, by all sectors, exceeds potential output. In other words, we rely on a steady inflow of goods and services to satisfy our excess demand, a situation we typically find acceptable during a high growth phase when domestic investment exceeds domestic saving. The second point of agreement is that high unemployment implies that actual output is far below potential output. We clearly have unused capacity.

Points one and two appear that they should be mutually exclusive, but they are not. The fact that they are not begs an explanation. Paul Krugman sends us to Paul Samuelson to provide that explanation:

Here’s what he [Samuelson] wrote in his 1964 paper “Theoretical notes on trade problems”: “With employment less than full and Net National Product suboptimal, all the debunked mercantilist arguments turn out to be valid.” And he went on to mention the appendix to the latest edition of his Economics, “pointing out the genuine problems for free-trade apologetics raised by overvaluation”.

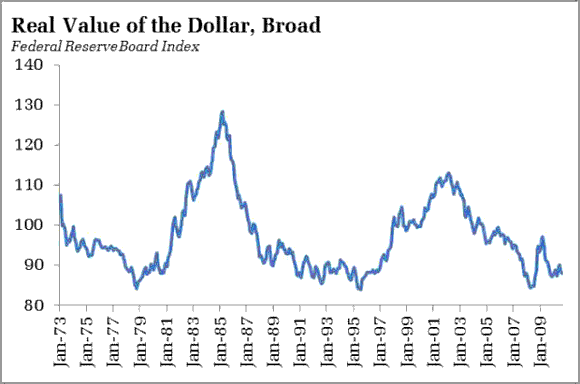

I think Samuelson is correct; an excessively high dollar is the explanation for the simultaneous existence of a sizable current account deficit and excessive unemployment. Indeed, there appears to be a externally determined downward limit to real value of the Dollar, and we are close to pushing against it:

The US appears to have little control over that minimum level. Foreign central have repeatedly acted to limit Dollar depreciation. Over the years, US policymakers have happily accepted this state of affairs (the steady financial inflow certainly helped support structural fiscal deficits), all the while ignoring the very real structural outcomes of blind adherence to the idea of a strong Dollar. spencer at Angry Bear succinctly lays out the structural impact:

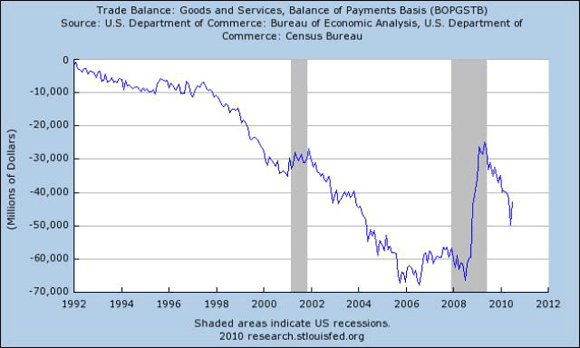

The first chart is of imports market share, or imports as a share of what we purchase in the US. In the second quarter of this year imports market share rebounded to about where it was at the pre-recession peak, or about 16% of consumption. Since the early 1980’s when the US started borrowing abroad to finance its two structural deficits — federal and foreign–trades share of consumption has risen from about 6% to some 16%. Normally this has a small negative impact on the US economy, but sometimes you get quarters like the last quarter. Last quarter real domestic consumption rose at a 4.9% annual rate. That was an increase of $162.6 billion( 2005 $). But real imports also increased $142.2 billion (2005 $). That mean that the increase in imports was 87.5% of the increase in domestic demand.

To apply a little old fashion Keynesian analysis or terminology, the leakage abroad of the demand growth was 87.5%. It does not take some great new “freshwater” theory to explain why the stimulus is not working as expected, simple old fashioned Keynesian models explain it adequately.

Years of current account deficits – deficits induced not by the decisions of private savers looking to maximize returns but by foreign public sector entities seeking to maintain export growth – has literally resulted in a US economy that, on net, is unable to produce the goods its citizens want to consume. Hence a blast of stimulus flows overseas , the rising trade deficit heralded as a sign of strong US demand despite the inconvenient truth of little net job creation.

Which brings us to this observation by Simon Johnson:

The main reason the U.S. isn’t bouncing back so fast is because of exports and the dollar. South Korea, Russia, and other emerging markets that go through severe crises usually undergo a sharp depreciation in the inflation-adjusted value of the currency, making them hypercompetitive, at least for a while. This makes it easier to replace imports with domestic goods and services and much more attractive to export.

In contrast, the global financial crisis actually strengthened the U.S. dollar as it was seen as a haven, although the dollar has fallen somewhat from its recent peak against major trading partners.

Currency depreciation – of substantial magnitude – is a mechanism by which economies recover from financial crisis. But we shouldn’t underestimate that challenges that accompany such an adjustment. If it happens to quickly – a sudden stop of capital – the most likely short run outcome is that the current account deficit will be resolved with import compression via a sharp drop in demand. This would be painful, to say the least. It is not the optimal path.

Neither, though, is the current path – a painstakingly slow Dollar depreciation. The result so far is persistently high US unemployment, with no relief in sight. In frustration, policymakers lash out against the wrong target, free trade. Krugman’s frustration rises to the level that he supports the Levin bill as the only remaining option:

Finally, the idea that what we need is a mature discussion of global rebalancing strikes me as reasonable — if you have been living in a cave the past three or four years. We’ve been reasoning, and reasoning, and reasoning, and nothing changes. Clearly, China does not want to act — not out of national interest, but because of the political influence of its export industries. It won’t change its behavior unless it faces an additional incentive — like the prospect of countervailing duties.

But I don’t want to make this piece about China. It is more than China at this point. It became more than China the instant US Federal Reserve policymakers woke up one morning and decided they needed to take the dual mandate seriously. And seriously means quantitative easing. Brad DeLong suggests that when the Fed actually acts on November 3, it will be too little too late. But if it is too little, more will be forthcoming.

Put simply, the Federal Reserve is positioned to declare war on Bretton Woods 2. November 3, 2010. Mark it on your calendars.

So perhaps Bretton Woods does not end because foreign governments are unwilling to bear ever increasing levels of currency and interest rate risk or due to the collapse of private intermediaries in the US, but because it has delivered the threat of deflation to the US, and that provokes a substantial response from the Federal Reserve. A side effect of the next round of quantitative easing is an attack on the strong dollar policy.

The rest of the world is howling. The Chinese are not alone; no one wants it to end. From Bloomberg:

Leaders of the world economy failed to narrow differences over currencies as they turned to the International Monetary Fund to calm frictions that are already sparking protectionism….

….Days after Brazilian Finance Minister Guido Mantega set the tone for the gathering by declaring a “currency war” was underway, officials held their traditional battle lines. U.S. Treasury Secretary Timothy F. Geithner and European Central Bank President Jean-Claude Trichet were among those to signal irritation that China is restraining the yuan to aid exports even as its economy outpaces those of other G-20 members.

“Global rebalancing is not progressing as well as needed to avoid threats to the global economic recovery,” Geithner said. “Our initial achievements are at risk of being undermined by the limited extent of progress toward more domestic demand- led growth in countries running external surpluses and by the extent of foreign-exchange intervention as countries with undervalued currencies lean against appreciation.”

At the same time, officials from emerging economies including China complained that low interest rates in the U.S. and its developed-world counterparts mean investors are pouring capital into their markets, threatening growth by forcing up currencies and inflating asset bubbles. The MSCI Emerging Markets Index of stocks has soared 13 percent since the start of September…

…“Near-zero interest rates and rapid monetary expansion are geared at stimulating domestic demand but also tend to produce a weakening of their currencies,” Mantega said Oct. 9. As a result, developing countries will continue to build up reserves in foreign currency to avoid “volatility and appreciation.”

Consider the enormity of the situation at hand. The Federal Reserve is poised to crank up the printing press for the sake of satisfying their domestic mandate. One mechanism, perhaps the only mechanism, by which we can expect meaningful, sustained reversal from the current set of imbalances is via a significant depreciation of the dollar. The rest of the world appears prepared to fight the Fed because they know no other path.

Bad things happen when you fight the Fed. You find yourself on the wrong side of a whole bunch of trades. In this case, I suspect it means that Bretton Woods 2 finally collapses in a disorderly mess. There may really be no other way for it to end, because its end yields clear winners and losers. And the losers, in this case largely emerging markets, and not prepared to accept their fate.

Moreover, there is no agreement on what should be the post-Bretton Woods 2 rules of the game for international finance. Is there even a meaningful policy discussion? Perhaps a little hope via Bloomberg:

Suggestions for how to resolve currency differences were vague in Washington, with French Finance Minister Christine Lagarde proposing better coordination and more diversification, while Canada’s Jim Flaherty suggested that new “rules of the road” be outlined.

Of course, in the next sentence hope is dashed:

European Central Bank Executive Board member Lorenzo-Bini Smaghi suggested the G- 20 may be too big to find a compromise.

Unless checked in South Korea, the discord may snap the G- 20’s united front formed to fight the financial crisis and recession.

And don’t expect that the International Monetary Fund is prepared to deal with this crisis:

Unable to find common ground themselves, governments agreed the IMF should serve as currency cop by preparing reports which show how the policies of one economy affect others. The studies will focus on the U.S., China, the U.K. and the euro area.

“The need to have this kind of spillover report has been discussed for months and now it’s part of our toolbox,” IMF Managing Director Dominique Strauss-Kahn said.

Well, thank the Heavens above, the IMF stands ready to produce a report. Now I can sleep easy.

Bottom Line: The time may finally be at hand when the imbalances created by Bretton Woods 2 now tear the system asunder. The collapse is coming via an unexpected channel; rather than originating from abroad, the shock that sets it in motion comes from the inside, a blast of stimulus from the US Federal Reserve. And at the moment, the collapse looks likely to turn disorderly quickly. If the Federal Reserve is committed to quantitative easing, there is no way for the rest of the world to stop to flow of dollars that is already emanating from the US. Yet much of the world does not want to accept the inevitable, and there appears to be no agreement on what comes next. Call me pessimistic, but right now I don’t see how this situation gets anything but more ugly.

Leave a Reply