Priceline.com, Inc. (PCLN) has been on an amazing rally for the last three months, more than doubling in price after jumping from $175 to over $350. With estimates on the rise and a bullish growth projection, PCLN looks like a serious momentum contender.

Company Description

Priceline.com, Inc. is an online travel company operating in the U.S., Europe and Asia. The company was founded in 1997 and has a market cap of $16 billion.

Although PCLN has been trending higher for most of the last few years, shares took a quantum leap forward on August 4 after the company reported awesome Q2 results that easily beat expectations.

Second-Quarter Results

Revenue for the period was up 27% from last year to $767 million. Earnings also came in strong at $2.81, 14% ahead of the Zacks Consensus Estimate, where the company has an average earnings surprise of 15% over the last four quarters.

The strong results were driven by the company’s growing international presence, where sales were up 63% from last year to $322 million.

Hotel bookings also looked great, where hotel-room nights booked was up 48% from last year. The company’s domestic business was nothing to sneeze at either, with gross bookings were up 20% on strong demand for hotels.

Balance Sheet

Although Priceline’s total debt increased $245 million from last year to $636 million, its cash and short-term investments skyrocketed $631 million to $1.22 billion.

Estimates

We did see some upward movement in estimates off the good quarter, with the current year adding $1.25 to $11.46. The next-year estimate is up $1.90 in the same period to $14.26, a bullish 24% growth projection.

Valuation

In light of the recent string of gains, shares of PCLN don’t come cheap, trading with a forward P/E multiple of 31X, a sharp premium to the industry average of 16X.

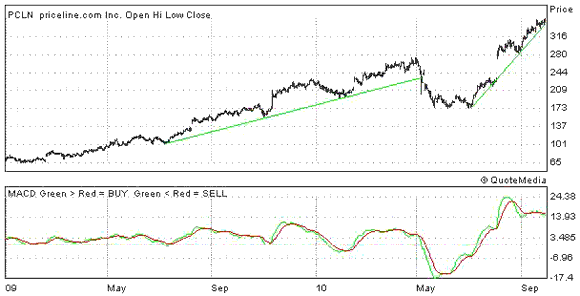

2-Year Chart

PCLN began moving higher in early July before surging in August on the better than expected Q2 results. The MACD below the chart is in mostly neutral territory, with a slight bias to the up side, take a look below.

Leave a Reply