Hard to believe it’s month-end already. Gee, time sure does fly when you’re having fun. (Or…..B.) In any event, the lack of massive equity moves, such as we’ve observed for most of this year, should preclude the sort of month-end fixing/rebalancing jiggery-pokery that’s been observed for the past six months. Perhaps the most interesting thing will be to observe what the asset allocators do. Bonds have cheapened nicely against equities this month and are entering a seasonal purple patch. Equities, however, will be in solid “go away” territory for the next five months.

Not that any of this will necessarily matter, of course. Seasonals are all well and good, but should arguably be swamped by the importance of the incoming dataflow. Yesterday’s comments section contained some interesting debate about the valuation argument for equities, so Macro Man has delve a bit deeper.

One commenter posited that European equities looked attractive because of the dividend yield of certain companies. Now, Macro Man has neither the competence nor the mandate to trade individual stocks, so he is forced to look at things from a top-down, er, macro, index-level.

One of his favourite markets to trade is Eurostoxx, where not only are there listed options and futures on the index itself, but also listed options on the dividends paid out by the index consituents. Although payour ratios are not constant, these represents a decent proxy for market-implied earnings trends and, one could argue, economic growth.

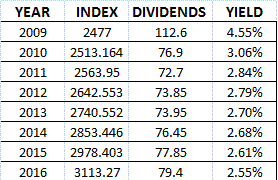

It is a peculiarity of the Eurostoxx that most of the index dividends are paid or committed early in the year, meaning that they actually represent a good bit of the prior year’s earnings. So for example, last year the Eurostoxx paid dividends equivalent to roughly 158 index points, a record high….representing earnings accrued primarily in 2007, before the worst of the financial crisis hit. 2009 dividend payments are expected at 112.6 on current pricing, and some 93 points of that has already been paid or committed. That decline represents the impaired earnings power of 2008. Next year, the market is forecasting divvy payments of 76.9 points, representing declining earnings this year.

Now, what’s interesting is that the strip is pricing the nadir of dividend payments to occur in 2011, meaning that the bottom in Eurostoxx earnigns is likely to occur next year rather than this. Moreover, divvy payments are not expected to exceed 2010 levels until 2015, implying that 2009 earnigns will not be bested until 2014!!!

Now, what’s interesting is that the strip is pricing the nadir of dividend payments to occur in 2011, meaning that the bottom in Eurostoxx earnigns is likely to occur next year rather than this. Moreover, divvy payments are not expected to exceed 2010 levels until 2015, implying that 2009 earnigns will not be bested until 2014!!!

Call Macro Man crazy, but that hardly strikes him as an attractive proposition. If the dividend futures are correct, we can expect basically zero earnings growth for the next five years. Why the hell should we want to buy equities then? And if divvy futures are underestimating the likely trajectory of earnings, aren’t they a better buy then equities (given that you don’t have to worry about getting the mutliple right.)? By way of disclaimer, Macro Man has been long various segments of this strip for most of the year as abottom-of-the-drawer “eventual recovery” trade.

Put graphically, the implied dividend yield of the Eurostoxx index in future years (using a forward index level implied by swap yields) doesn’t look like anything special…and that’s before you consider things like volatility and uncertainty.

Frankly, for a no-brainer valuation trade at this juncture, Macro Man personally requires a much higher equity risk premium to be enthused about jumping in.

Failing that, all we have to fall back on is money-market cash levels. And while “everybody else is doing it, so why don’t we” can on occasion be a persuasive argument, it’s also paved the road to some of the most spectacular crashes of the past couple of decades. Put another way, just because some other doughnut decided that it’d be fun to buy GM stock (which traded in positive territory for most of the day) the day that they announced their imminent bankruptcy timetable doesn’t mean that it’s a good idea for you or Macro Man to do it.

Leave a Reply