Between 2005 and 2008 the Chinese yuan appreciated by a bit over 20%. Then when the recession got bad in late 2008, the yuan was (wisely) re-pegged to the dollar. Now Fred Bergsten calls for another round of yuan appreciation:

C. Fred Bergsten, director of the Peterson Institute for International Economics, a leading research organization here, told House lawmakers on Wednesday that a similar increase over the next two to three years would create about 500,000 jobs. He said it would reduce China’s current account surplus by $350 billion to $500 billion, and the American current account deficit by $50 billion to $120 billion.

The United States should seek to mobilize the European Union and countries like Brazil, Russia and India to press China to realign the renminbi, and should seek W.T.O. authorization to impose restrictions on Chinese imports if it does not do so, Mr. Bergsten said.

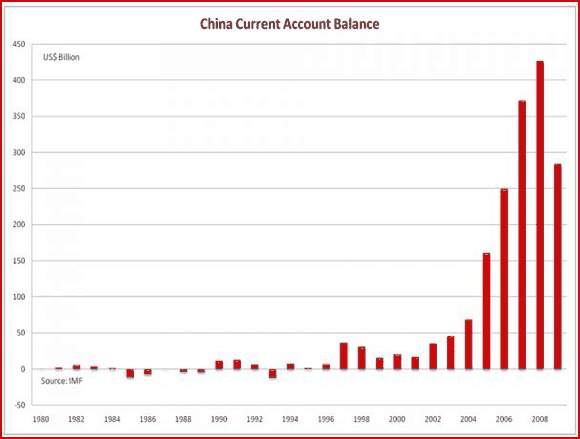

I’m not opposed to modest yuan appreciation, and indeed I think it will gradually occur over the next three years. But I am opposed to a trade war, which is utter madness in a world struggling to recover from the Great Recession. Here’s what I don’t understand however. Between 2004 and 2008 the Chinese CA surplus rose from about $70 billion to about $430 billion. Why does Bergsten now expect “a similar [yuan] increase over the next two to three years” to reduce the Chinese CA surplus by roughly that amount?

And for those of you expecting a Republican Congress to rescue us from Obama’s foolish statist polices, check out this quotation:

Mr. Grassley added: “The administration should go one step further and bring a case against China’s unfair currency manipulation at the W.T.O.”

In 1985 Paul Krugman (p. 7) argued that the dollar needed to fall sharply in order to prevent chronic CA deficits, which he said would lead to “infeasible” foreign debt levels. He was right about the dollar, it did fall sharply after 1985. But we’ve had 25 years of almost nonstop CA deficits, and no sign of a light at the end of the tunnel. Why? Because the falling dollar didn’t address the fundamental cause of the CA deficit, a saving/investment imbalance produced by a fiscal regime that is profoundly anti-saving. You can’t fix that with a band-aid.

Policymakers need to go back and reread Mundell.

PS. Perhaps the term ‘reread’ represented my own triumph of hope over experience.

HT: Mike Belongia

Leave a Reply