No… but he’s got no love for the Empire, I can tell you that.

This morning, S&P put the AAA rating of the United Kingdom on negative outlook. Generally when S&P puts a negative outlook, it merely means they leaning toward a downgrade without any particular urgency. In this case, S&P says they need to see some progress made by an incoming British government on their burgeoning debt.

Since the U.K. is generally seen as the third most stable (U.S., Germany) of the big western economies, its not a big leap to say that the U.S. could be next. Its a perfectly legitimate concern. S&P mentions their concern that British debt could rise to 83% of GDP by 2013. In the U.S., its already 80%!

What would happen if the U.S. lost its AAA? Very hard to say. Foreign investors would still have the problem of finding someplace to put their money. I’d be surprised if the U.S. would lose its AAA rating, but say, France and Germany hold on to their ratings. Japan is already AA. It might result in a revision of how foreigners view ratings in general.

In other news, how is General Electric AA+ and stable if the U.K. needs to be downgraded? How is Assured Guaranty still AAA and stable?

Enter Bill Gross, always eager to talk his position. He stokes the fire by saying that the Treasury market is selling off due to ratings fears. Maybe. Indeed, I’ve heard that Asia is selling today. But always remember, when Bill Gross talks, he is always always always talking from position. So I’m assuming Gross is short Treasuries and today is adding.

Enter Bill Gross, always eager to talk his position. He stokes the fire by saying that the Treasury market is selling off due to ratings fears. Maybe. Indeed, I’ve heard that Asia is selling today. But always remember, when Bill Gross talks, he is always always always talking from position. So I’m assuming Gross is short Treasuries and today is adding.

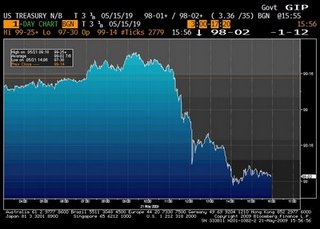

I don’t think really think the whole ratings thing makes sense to explain the Treasury sell-off. Here is the intra-day on Treasuries. S&P comes out with their report on the U.K. at 4:20 AM.

Treasuries are actually higher all during the Asian and European sessions, and its only once the U.S. session really gets going that the bond market sells off.

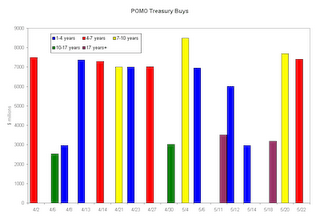

A better explanation is the continued belief that the Fed is defending some level on Treasuries. Admittedly, I thought they would, but the evidence is clear that they aren’t. Here are the Fed’s Treasury purchases since the program began:

A better explanation is the continued belief that the Fed is defending some level on Treasuries. Admittedly, I thought they would, but the evidence is clear that they aren’t. Here are the Fed’s Treasury purchases since the program began:

Traders keep hoping the Fed will increase their POMO buys, whereas this chart clearly shows they keeping to the $7-8 billion range in the belly and about $3 billion on the long end. Their reluctance to increase purchases shows they either have no particular target or their target is much higher than where we are.

No sense in getting in the way of the Treasury negative momentum here. I’m probably not a buyer until 3.60%.

Leave a Reply