Was the subprime crisis inevitable? This column looks at how the last mortgage crisis in the 1930s shaped the policy landscape in the US, arguing that it eventually led to the emergence of private securitisation in the 1990s, a surge in homebuilding and homeownership, and a second great mortgage crisis that was just around the corner.

The current mortgage crisis in the US is more severe than any since the 1930s. So it makes good sense to examine the origins, impacts, and consequences of that last great mortgage crisis great mortgage crisis – indeed many commentators have made a direct comparison between the two (see for example Eichengreen and O’Rourke 2010). The case for examining the last great crisis is especially pronounced given that the US Secretary of the Treasury has just asked Americans to “consider the challenge of how to build a more stable housing finance system” (Geithner 2010).

Yet we should be humble in taking up this challenge. We are after all reforming a mortgage system that was built on a framework that Depression-era policymakers forged in response to their own crisis. One of those policymakers was Henry Hoagland, who described the situation he faced in 1935 as a member of the Federal Home Loan Bank Board thus:

[A] tremendous surge of residential building in the [last] decade…was matched by an ever-increasing supply of homes sold on easy terms. The easy terms plan has a catch…[o]nly a small decline in prices was necessary to wipe out this equity. Unfortunately, deflationary processes are never satisfied with small declines in values. In the field of real-estate finance… we have depended so much upon credit that our whole value structure can be thrown out of balance by relatively slight shocks. When such a delicate structure is once disorganized, it is a tremendous task to get it into a position where it can again function normally. (Hoagland 1935)

This column looks back over the terrain that Hoagland described by examining how the residential mortgage market worked before 1930 and how it was changed by crisis and policy in the 1930s. It turns out that this history lesson provides some fresh perspective on today’s mortgage crisis (see my accompanying paper, Snowden 2010, for more details).

A century-long view of the 1930s mortgage crisis

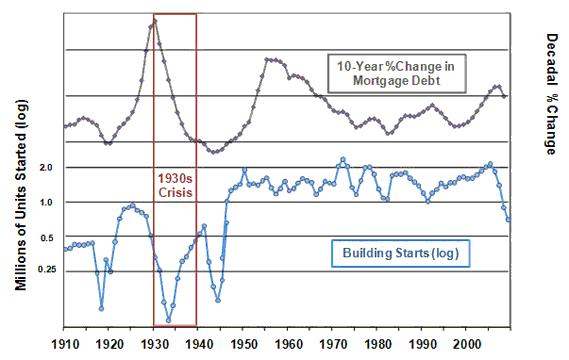

To place events in the 1920s and 1930s into perspective, Figure 1 presents a long-run view of developments in the housing and residential mortgage sector using annual series of non-farm residential building starts and growth rates of inflation-adjusted residential mortgage debt.

- Between 1921 and 1929 the nominal volume of non-farm residential mortgage debt tripled, and inflation-adjusted debt grew faster than in any decade before or since.

- The rapid expansion financed a home-building boom and an increase in the rate of home ownership from 41% to 46%.

- Nominal mortgage debt started to contract abruptly in 1930, but remained constant in inflation-adjusted terms over the next decade as the visible manifestations of a mortgage crisis unfolded – record levels of foreclosure, widespread distress among mortgage lenders, a collapse and weak recovery in home building, large decreases in home values, and the reversal of the gains in home ownership made in the 1920s (Wheelock 2008).

Figure 1. Building starts and decadal change in CPI-deflated mortgage debt, 1910-2008

Notes: see Snowden (2010).

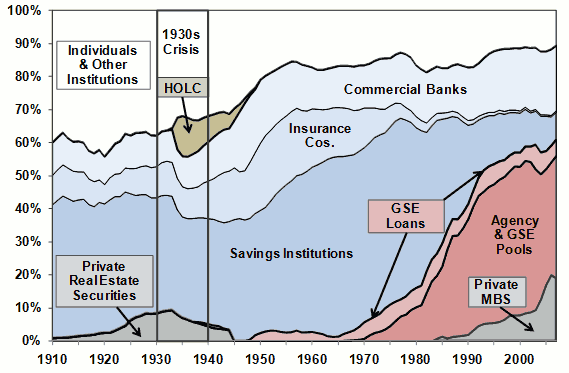

Figure 2 provides a companion view showing how the structure of the residential mortgage market has changed over the past century. During the 1920s, for example, the share held by institutional lenders – commercial banks, life insurance companies and, savings institutions – remained virtually constant. The big change during that decade was the rapid growth in two new forms of private real estate securities that by 1929 funded nearly 10% of the outstanding residential mortgage debt. Goetzmann and Newman (2010) examine one of these innovations: single-property real estate bonds that were used to finance commercial property, including multifamily residential projects, in large urban areas. The second form of securitisation was introduced by New York mortgage guarantee companies that issued participation certificates, similar to modern pass-through securities, on groups of mortgages that they insured and placed into trusts.

Figure 2. Shares of non-farm residential mortgage debt, 1910-2007

Notes: The Savings Institutions category includes Building & Loan Associations, mutual savings banks, Savings & Loan associations and other savings institutions. See Snowden (2010).

Against this backdrop, two striking changes in market structure occurred during the 1930s.

- First, the share of private real estate securities gradually fell to zero.

Behind this decline, however, were decade-long liquidations of both single-property real estate bonds and guarantee mortgage companies after both innovations failed in the early 1930s. Unwinding these structures proved to be so difficult, involved, and costly that privately-sponsored mortgage insurance and securitisation disappeared from the US mortgage market for decades (Snowden 1995).

- Second was the the large impact of the Home Owners’ Loan Corporation (HOLC) during the mortgage crisis (Figure 2).

This agency was created in 1933 to serve as both a bad mortgage bank – by buying distressed mortgages from private lenders – and as a loan modification programme – by refinancing the mortgages it purchased with long-term, high-leverage, amortised loans. Within three short years the HOLC held mortgages on one-tenth of the nation’s owner-occupied homes and only now are beginning to understand just how it worked and how well it worked (Courtemanche and Snowden 2010, Fishback et al. 2010 and Rose 2010).

A few other institutional developments during the 1930s deserve comment. One set involved Building & Loan Associations (B&Ls) which were the most important source of home mortgage debt during the 1920s, but hit hard by the onset of the crisis. Three new programmes were created for B&Ls between 1932 and 1934: the mortgage loan discounting facility of the Federal Home Loan Bank System, a new system of Federal Savings & Loan charters, and an insurance programme (FSLIC) for members’ share accounts. Most B&Ls did not participate in these new programmes and by 1941 a total of 6,000 B&Ls had failed – half of the number that had been operating in 1929. Some 4,000 of the remaining associations embraced the new system and became the core of the modern S&L industry.

A second development of note was the creation of a federal mortgage loan insurance programme in 1934 through the auspices of the Federal Housing Administration (FHA). The FHA loan programme was heavily used by intermediaries that were not served by the Federal Home Loan Bank System – mortgage companies, commercial banks, and life insurance companies. To provide a dedicated secondary market facility for the new insurance programme, the National Housing Act of 1934 authorised federal charters to be issued to privately-financed, mortgage associations that were permitted to use FHA loans as collateral for covered mortgage bonds. Not a single private mortgage association had been chartered by 1938 and the responsibility for creating the secondary market for FHA loans was then given to the federally-funded Federal National Mortgage Association (FNMA).

How did we get here?

Figures 1 and 2 also show how the crisis of the 1930s altered the long-run development of the residential mortgage market. After WWII the portfolio lenders that were so well-supported by the new federal programmes of the 1930s became dominant as Savings & Loans, commercial banks, insurance companies, and mutual savings banks held an unprecedented 80% of the nation’s residential mortgage debt. Competition was limited and innovation de-emphasised within the postwar system, but all major lenders had plenty of “skin in the game” as they held mortgages that they, or close affiliates, originated and serviced. Supported by the secondary market operations of the Federal National Mortgage Association and the Federal Home Loan Bank System, this framework financed a rapid expansion in home building, mortgage debt and home ownership in the 1950s without, as shown in Figure 1, crisis or substantial instability.

The postwar mortgage system began to unravel in the late 1960s because portfolio lenders could not profitably underwrite the risks of funding long-term mortgages with fixed rates and generous prepayment privileges after the rate of inflation, and nominal interest rates, became high and variable.

While bad policy and lax regulation eventually turned the failure of this business model into the thrift debacle, the key development during the 1970s was the return of securitisation. The innovation did not return as the federally-sponsored, covered mortgage bond system that had been envisioned in 1934. Instead, securitisation reappeared through the operations of one federal agency (Ginnie Mae) and the two Government Sponsored Enterprises (Fannie Mae and Freddie Mac) that were carved out of secondary market facilities – the Federal National Mortgage Association and the Federal Home Loan Bank System – that had been designed in the 1930s to support portfolio lenders.

We can see in Figure 1 that the distress and change in the nation’s residential mortgage market between 1970 and 1990 was accompanied by increased instability in home building and in the growth of inflation-adjusted mortgage debt. This volatility, however, was moderate by historical standards.

Figure 2 shows that agency securitisation made modest inroads at first, but captured virtually all of the mortgage business lost by insurance companies and savings institutions during the 1980s. Private agencies played an important role in the process by repackaging the virtually default-free cash-flows generated by government-sponsored enterprise pass-through securities into collateralised mortgage obligations that offered investors different exposure to the prepayment and interest rate risks that were generated by the underlying pools of mortgages.

The boundaries in mortgage securitisation became blurred during the 1990s in two ways.

- First, government-sponsored enterprises began to hold large numbers of the mortgages and securities that they underwrote in their own portfolios because they could profitably fund them with debt that enjoyed an implicit federal guarantee.

- Second, private agencies began to securitise on their own by underwriting the credit risk on pools of mortgages that the government-sponsored enterprises, at least at first, would not securitise.

After 1995 the two forces converged to generate the third great expansion of residential mortgage debt in the past century, a re-emergence of private-label securitisation on a scale not seen since the 1920s, and a surge in homebuilding and homeownership. The second great mortgage crisis was just around the corner.

References

•Courtemanche, Charles and Kenneth Snowden (2010), “Repairing a Mortgage Crisis: HOLC Lending and Its Impact on Local Housing Markets”, NBER Working Paper 16245, July.

•Eichengreen, Barry and Kevin H O’Rourke (2010), “A tale of two depressions: What do the new data tell us?”, VoxEU.org, 8 March.

•Fishback, Price, Shawn Kantor, Alfonso Flores-Lagunes, William Horrace, and Jaret Treber (forthcoming), “The Influence of the Home Owners’ Loan Corporation on Housing Markets During the 1930s”, Review of Financial Studies.

•Geithner, Timothy (2010), “Opening Remarks at the Conference on the Future of Housing Finance: August 18, 2010”, Downloaded 8/18/10.

•Goetzmann, William N and Frank Newman (2010), “Securitization in the 1920’s”, NBER Working Paper 15650, January.

•Hoagland, Henry (1935), “The Relation of the Work of the Federal Home Loan Bank Board to Home Security and Betterment”, Proceedings of the Academy of Political Science, 16(2),45-52.

•Rose, Jonathan (2010), “The Incredible HOLC? Mortgage Relief during the Great Depression”, Unpublished Working Paper, April.

•Snowden, Kenneth (1995), “Mortgage Securitization in the U. S.: 20th Century Developments in Historical Perspective”, in M Bordo and R Sylla (eds.), Anglo-American Financial Systems, New York: Irwin, 261-98.

•Snowden, Kenneth (2010), “The Anatomy Of A Residential Mortgage Crisis: A Look Back To the 1930s,” in L. Mitchell and A. E. Wilmarth (ed.), The Panic of 2008: Causes, Consequences and Proposals for Reform. Northampton, MA, Edward Elgar Publishing.

•Wheelock, David C (2008), “The Federal Response to Home Mortgage Distress: Lessons from the Great Depression”, Federal Reserve Bank of St. Louis Review, May/June, 90(3):133-48.

![]()

Leave a Reply