In 2005 Paul Krugman called the US housing bubble. A couple weeks ago he reminded us that he called the bubble, and implied only a fool (or a brainy right-wing ideologue?) could have failed to see it. He presented a graph showing that housing prices in the US had been rising rapidly. Interestingly, housing prices had been rising rapidly in lots of countries, but relatively few turned out to have housing bubbles. Here’s a graph Tyler Cowen linked to recently:

Let’s use the archive list of months as a vertical line to estimate prices in 2005 when Krugman made the call, and compare them to today’s price:

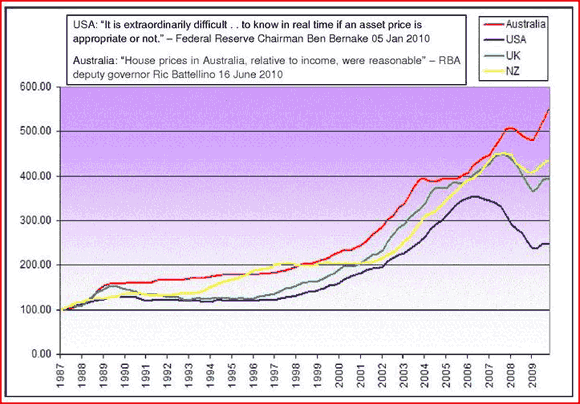

- US 2005 = 300, 2010 = 250

- UK 2005 = 375, 2010 = 395

- NZ 2005 = 330, 2010 = 430

- Aus 2005 = 390, 2010 = 550

I don’t know about you, but to me only the US looks like a clear-cut bubble. Yes there were some rises and falls in other countries, but it wasn’t obvious (ex ante) in 2005 whether prices in the other three countries were above or below their long run equilibrium. Indeed it still isn’t, as Australian housing prices could crash at any time.

I’ve consistently argued that the bubble theory is only useful if it leads to good predictions. Krugman did make a good prediction, that housing prices would be lower in the not too distant future. BTW, I’d say you at least need to provide some sort of time frame—say 5 years out. It’s not enough to say “I predict prices will keep rising, and then eventually fall.” That’s true of any market. Although Krugman did not provide a specific number in the post I linked to, I am pretty sure that the actual drop in the US occurred over the sort of time frame he envisioned, if he had been forced to name a date. So I give him complete credit for a correct prediction.

But here’s my question. Given that the other three markets did not decline over the same time period, is it really true that we could be confident, ex ante, that US houses were overpriced in 2005? It certainly seems so given everything that has happened since, but might that be a cognitive illusion? Confirmation bias? I doubt Krugman thought NGDP would suddenly fall 8% below trend in the 12 months after mid-2008. Where would housing prices be today if NGDP had kept growing at 5%. I don’t know.

I’m inclined to believe there was some irrationality in the 2005 housing market, but I am less confident than Krugman that price bubbles are easy to spot. In the next post I’ll provide one reason why, despite the undeniable excesses that swept the housing market, investors with rational expectations about NGDP growth and immigration might not have spotted the oncoming collapse in US housing prices.

BTW, look at housing prices in Australia; the one country on the list that did not experience a recession in 2008, and which has very rapid immigration.

PS. This interactive graph in The Economist shows that among 20 countries, only the US and Ireland showed a clear bubble-like pattern after 2005. In most countries prices are now higher than in 2005, and in the few other exceptions (Germany, Japan) there had been no run-up in prices prior to 2005. So my results don’t come from cherry-picking these four anglophone nations, bubbles really are hard to spot. (I’m puzzled by the Spanish price graph, but even if it is inaccurate and Spain was a bubble, that just makes three clear bubbles in The Economist group of 20.)

You can adjust the horizontal scale to get different starting dates. Many countries saw steep price run-ups prior to 2005. If you start at 2005:Q2, it’s easy to compare current prices to mid-2005 prices.

PPS: Compare Krugman’s mea culpa post, with these Japan predictions dredged up by David Henderson. The second paragraph shows Krugman at his best. What happened to that guy?

It ain’t over yet. Won’t be for years. There’s plenty of scope for further “corrections”, world wide. Probably little basis for declaring victory in the second inning.

Was this the same Mr. Krugman that advocated the Fed increase the credit money supply and slash interest rates in the wake of the dotcom crash in 2002? You mean that guy? That was what caused the housing bubble to begin with. Government guarantees and programs only exaxerbated it. We had been in a housing buble for a while by the time Mr. krugman “called it.” There are some economists, the Austrians notably, who called a housing bubble when they saw the actions of the Federal Reserve in 2002 and 2003. Krugman still doesn’t see the cause nor does he quite understand why deficit spending and money printing haven’t gotten us out our current mess.