Despite the stunning contraction of industrial production and trade across the globe, the global economy is still a far cry away from the calamities of the Great Depression. However, if the economic damage of the current global crisis may have been contained so far, worrisome parallels to the early 1930s remain and preventive policy actions must be kept up.

The world is experiencing its most severe recession since World War II. In their recent Vox column, Barry Eichengreen and Kevin O’Rourke (2009) suggest that we are already on the path to another global depression. By other metrics, however, we are still far cry away from the calamities of the Great Depression (Romer, 2009). The economic damage caused by the current crisis has been contained thus far, though worrisome parallels to the early 1930s persist.

Comparing the salient features: Great Depression versus today

The current global crisis is the most severe financial crisis since the Great Depression, and the IMF now predicts that 2009 will have the deepest global downturn in the post-World War II era. Such parallels invite comparisons with the Great Depression. In doing so, it is useful to distinguish between setting, initial conditions, transmission, and policy responses.

- Crises and contractions in the core: US at the epicentre

The US economy was the epicentre of the financial contraction in both the Great Depression and the current crisis. This feature distinguishes these episodes from the many other financial crises of the past few decades, all of which occurred in small, typically emerging economies, or more garden-variety recessions in the major economies. Given the weight of the US economy and the US financial system, a global impact has thus been all but certain from the onset.

- Financial and economic vulnerabilities

Both episodes were preceded by rapid credit expansion and financial innovation that led to high leverage. However, while the 1920s credit boom was largely US-specific, the 2004-07 boom was global. With much higher levels of real and financial integration than during the interwar period, a US financial shock now has a larger and more immediate impact on financial systems elsewhere. These greater financial vulnerabilities must be balanced against weaker global economic conditions in 1929. Germany was already in recession then. Wholesale and, to a lesser extent, consumer prices in major economies had already stagnated or begun falling before the onset of the US recession. Slowing activity thus led to deflation almost immediately. In contrast, inflation above target in mid-2008 has provided an initial cushion in the current crisis.

- Financial sector balance sheet adjustment

Liquidity and funding problems have played a key role in the financial sector transmission in both episodes. Concerns about the net worth and solvency of financial intermediaries were at the root of both crises, although the specific mechanics differed given the financial system’s evolution.

In the Great Depression, the problems arose from the erosion of the deposit base of US banks in the absence of deposit insurance. In four waves of bank runs, about one-third of all US banks failed between 1930 and 1933. The failure of the Austrian bank Creditanstalt, in 1931, set the scene for bank runs in other European countries.

In the current crisis, reassurance from deposit insurance has largely prevented bank runs by retail depositors. Instead, funding problems have arisen for financial intermediaries relying on wholesale funding, particularly those issuing or holding (directly and indirectly) US mortgage-related securities whose value was hit by increasing mortgage defaults. With large cross-border linkages, the problems have immediately been international in reach. In contrast, the spillovers were more gradual in the 1930s, with the US funding problems transmitted through rising capital flows to the US and money supply contraction in the source countries.

- Policies to fight the crisis

Unlike in the Great Depression, when countercyclical policy responses were virtually absent (with the exception of the sterling block going off gold in 1931), there has been a strong, swift recourse to macroeconomic and financial sector policy support in the current crisis. Central banks in the major currency areas have intervened massively to provide financial systems with liquidity and lowered policy interest rates. Exceptional discretionary fiscal stimulus will support aggregate demand this year.

- No depression thus far

Despite the stunning contraction of industrial production and trade across the globe in the second half of 2008, the global economy is still a far cry away from the calamities of the Great Depression. The traumatic financial sector adjustment seen in the early 1930s has been avoided. Declines in activity and inflation in the US – the core economy – have so far been less virulent than they were during 1929–31. Perhaps most importantly, the destructive forces of debt deflation have not set in. This suggests that benefits of the unprecedented policy support, an international monetary system that provides for reflationary adjustment and more favourable initial macroeconomic conditions have outweighed the effects of greater vulnerabilities and cross-border linkages.

Worrisome parallels to the Great Depression remain

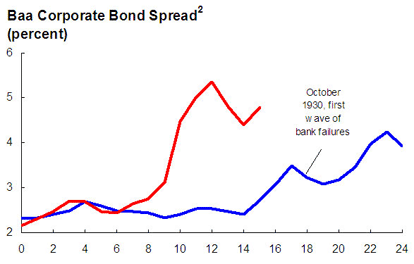

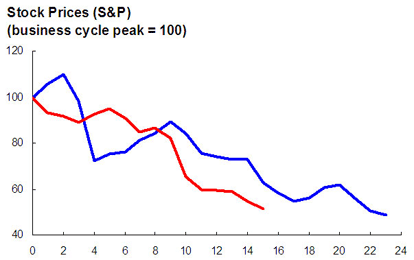

Despite the success in containing the damage to date, risks should not be underestimated. The deterioration in financial conditions from balance sheet contraction, asset fire sales, and increased demand for liquid assets has been more rapid than during the Great Depression and at least as strong, if not stronger (see Figures 1 and 2 describing financial factors in the US). Feedback effects on the solvency of financial intermediaries from declining economic activity are beginning to emerge. As we now know, it was the emergence of adverse feedback loops between real and financial sector adjustment in the absence of an offsetting policy response that gradually turned the severe recession of 1929-30 into the Great Depression. Clearly, policy actions to restore confidence in the financial sector, stop asset price deflation, avoid debt deflation, and support a global recovery must be kept up.

Figure 1. Baa corporate bond spread (percent), months after business cycle peak

Note: Blue line starts July 1929 and red line starts December 2007, the business cycle peaks identified by the National Bureau of Economic Research. Average yield on Baa-rated corporate bonds over yield on long-term treasuries.

Sources: Bernanke (1983); Federal Reserve Board; and Haver Analytics.

Figure 2. S&P stock price index, months after business cycle peak

Note: Blue line starts July 1929 and red line starts December 2007, the business cycle peaks identified by the National Bureau of Economic Research. Stock prices normalised to 100 at start date.

Sources: Bernanke (1983); Federal Reserve Board; and Haver Analytics.

Note: This article is based on Box 3.1 in the April 2009 World Economic Outlook.

References

Bernanke, Ben S., 1983, “Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression”, American Economic Review, Vol. 7_ (June), pp. 257–7.

Eichengreen, Barry, and Kevin H. O’Rourke, 2009, “A Tale of Two Depressions”, VoxEU.org, 6 April 2009.

Romer, Christina, 2009, “Lessons from the Great Depression for Economic Recovery in 2009”, presented at the Brookings Institution, Washington, D.C. (March 9).

IMF (2009). World Economic Outlook, April.

![]()

Leave a Reply