In the 1990’s many Japanese banks were known as zombie banks because while technically insolvent, they continued to operate because their ability to repay their debts is shored up by implicit or explicit government credit support. The banks did not write down their loans, but neither did they lend much because they were in a holding period until the asset pricing fairy pulled prices back up to their pre-bubble peak. A decade of stagnation followed.

Luckily, Americans are too stupid to do that again. Instead, we have the FHA, a government agency staffed by many talented economists who I’m sure could prove to you their policy is optimal (under certain assumptions), highlighting the benefits of a rigorous education in the dismal science. Currently the FHA is dominating the lower-than-average house mortgage market. It offers lenient terms for home buyers than any profit-oriented banker, all in the name of stimulus, such as only a 3.5% vs. 10% down payment, and debt-payment/income ratios of 60% vs 36%.

Why FHA’s contrary lending stance is a bad idea is because it takes a certain level of financial capital, and the correlated amount of prudence, to maintain a house, to make sense as the residual claimant on the property, to be the owner. There’s a large probability a furnace will break, and then what? For a $150k house, if you could only afford the 3.5% down payment, there’s a smaller chance you can maintain the house due to normal wear-and tear, as well as those big expenses like a blown furnace. Then, when the deteriorated house makes it clear the transaction is not easy money, the homeowner bolts and the property sits for 18 months attracting squatters, drug users, and vandals, which depresses neighborhood values (this is due to laws designed to protect the homeowner, who presumably is being bullied by the bank).

This FHA insanity highlights why, as mercurial and imperfect markets are, they are better than government directed markets. Markets make mistakes but they correct themselves much faster than government does.

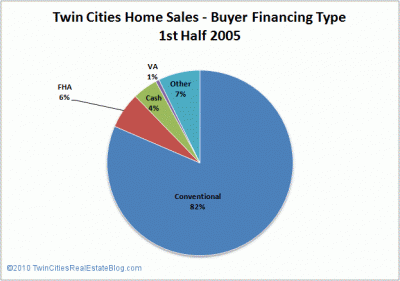

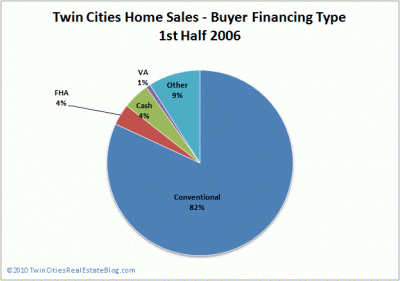

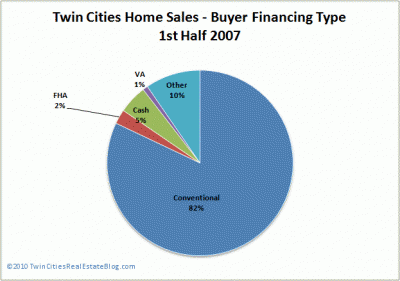

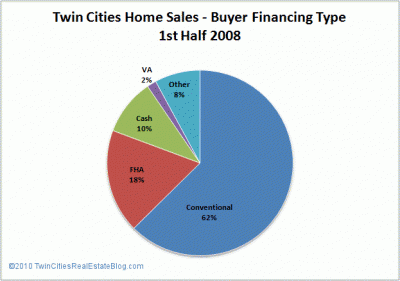

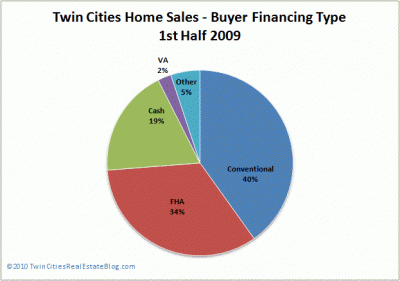

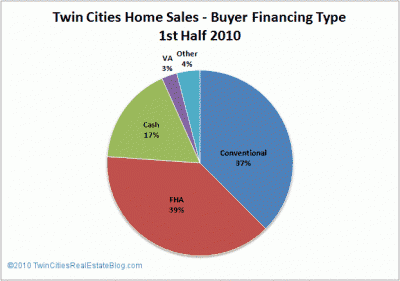

The following pie charts show the growth in FHA as a percent of total mortgage loans in the Minneapolis-St.Paul metro area since 2005 (data from here). For houses under $400k, they really dominate according to people I know in the business, but I wasn’t able to get it broken out that way. In fact, I couldn’t get much data from the FHA in general, as if they know what they are doing is dumb. FHA is the red slice of the pie.

Leave a Reply