In his recent NYT editorial, US Treasury Secretary Timothy Geithner proclaimed:

Even the surge in imports, which lowered the rate of increase of G.D.P., actually reflects healthy and growing American demand.

I imagine that he must then be thrilled by today’s trade report, which revealed the trade deficit swelled by $7.9 billion on the back of an explosion of imports. Analysts were quick to note that the new figures will contribute to another downward revision to the already disappointing Q2 GDP report:

“The wider-than-expected trade gap points in itself points to a 0.4 percentage point downward revision to GDP growth, which needs to be added to the 0.8 percentage point estimated downward revision coming from construction and inventories. Added together, these revisions at this point suggest second-quarter real GDP growth will barely be above 1% (call it 1.1%–1.2%),” said John Ryding and Conrad DeQuadros at RDQ Economics.

Peter Newland of Barclays Capital says that his firm’s tracking estimate for second-quarter GDP is now at just 0.3% growth. Economist Nouriel Roubini puts the figure at 1.2%.

I think you can argue a trade deficit reflects solid demand growth when the economy is operating near potential, or at least looks headed toward potential. I think such an analysis is ludicrous when unemployment hovers near double digits. Clearly, we have unused capacity. Yet no way to utilize it? Instead, I think the import surge reflects the deeply embedded structural imbalance in which US demand spending is increasingly satisfied with overseas production. In essence, you can stimulate domestic demand, but that demand is offset by an increased import bill. It is, of course, considered crass to suggest the import picture is an impediment to US growth. At least departing CEA Chair Christina Romer was willing to acknowledge the import picture may be a little important:

A bit of you keeps saying that if only those were American products, think of how high GDP growth would have been.

Indeed. The import surge, perhaps, is in part temporary. From Bloomberg:

The expiration of export-tax rebates on some Chinese commodities beginning in July may also cut U.S. imports from China in coming months, helping to narrow the deficit and thus contributing to growth in the third quarter, said Bandholz.

I am not really counting on that story, but one can hope. Note that in the earlier interview, Romer shifts quickly to the export story.

People are buying things. Importantly, exports are growing at 10%. We’ve always said that we have a demand problem and that one way to deal with it is to get foreigners to buy more of our products.

Geithner too is enamored with the potential of export growth:

Exports are booming because American companies are very competitive and lead the world in many high-tech industries

Federal Reserve Chairman Ben Bernanke also places significant weight on the export picture:

At the same time, rising U.S. exports, reflecting the expansion of the global economy and the recovery of world trade, have helped foster growth in the U.S. manufacturing sector.

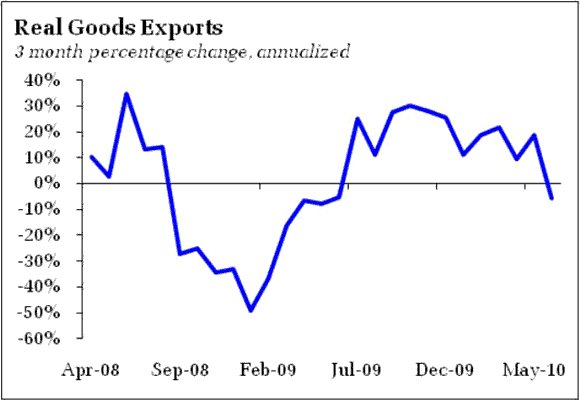

Unfortunately, all look to be behind the curve on the trend in real exports:

Combined trends in exports and imports are simply not supportive of economic growth. And, given the current state of the global financial architecture, where the US is expected to be the repository of global savings, it is difficult to see how the external sector contributes positively to the recovery.

Leave a Reply