“We have met the enemy and he is us,” Pogo used to say. Well, we’ve also now met the recovery, and he is ugly.

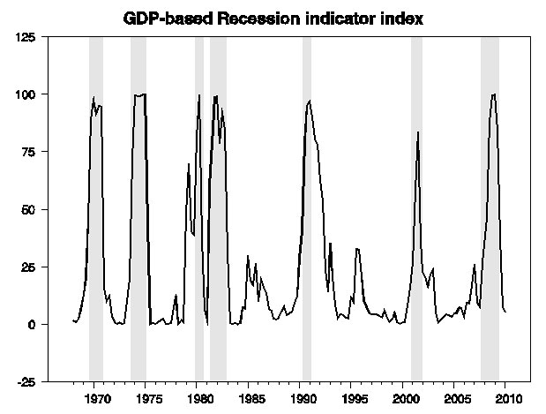

The Bureau of Economic Analysis reported today that U.S. real GDP grew at an annual rate of 2.4% during the second quarter. The latest GDP numbers bring our Econbrowser Recession Indicator Index for 2010:Q1 down to 5.4%. This index is based on a very simple pattern-recognition algorithm for characterizing economic recessions. It is not a prediction of where the economy is headed, but rather a backward-looking assessment of where the economy stood as of the first quarter, using today’s 2010:Q2 data release to help inform that assessment. University of Oregon Professor Jeremy Piger maintains a related index which has been at or below 1% for each month so far of 2010, while the most recent value calculated by U.C. Riverside Professor Marcelle Chauvet’s algorithm is 7.8%. All three approaches agree that the economy remains in a growth phase that began in the third quarter of last year. A subsequent economic downturn would be described as the beginning of a new recession rather than a continuation of the previous recession.

The plotted value for each date is based solely on information as it would have been publicly available and reported as of one quarter after the indicated date, with 2010:Q1 the last date shown on the graph. Shaded regions (with the exception of 2007:Q4-2009:Q2) represent dates of NBER recessions, which were not used in any way in constructing the index, and which were sometimes not reported until two years after the date. The most recent recession is shown on the graph as ending in 2009:Q2 as implied by the index; as of this writing the NBER has not yet assigned an end date for this recession.

But a pretty recovery it’s not. The economy has grown by 3.2% in real terms over the last year, about the average annual historical growth rate since World War II. But since recessions are characterized by below-average growth, expansions should typically exhibit above-average growth, and particularly in the first year of an expansion we often see very strong growth as a result of the positive contribution of inventory restocking in the initial stages of recovery. Inventories have done their part this time around as well, contributing 1.9 percentage points of that 3.2% growth over the last year. But that’s the problem– inventories have been essentially the sole factor driving the recovery so far.

Imports were a huge drag on GDP in the second quarter. It is as if all the additional spending by U.S. consumers and firms went to buy imported goods and services, with no net positive contribution to the demand for domestic production. Added purchases by the federal government provided an important boost to the second quarter, though that seems unlikely to continue and faces headwinds from future spending cuts by state and local governments. Housing made a modest positive contribution to the second quarter, though Bill McBride expects residential fixed investment to decline in Q3 with expiration of the tax credit.

Exports and nonresidential fixed investment were relative bright spots. But could they be enough to carry the economy into a sustained recovery without inventories and fiscal stimulus? The most pessimistic participant at the June FOMC meeting was calling for 2.9% real GDP growth for 2010 as a whole.

But I’ll be relieved if we end up doing that well.

Leave a Reply