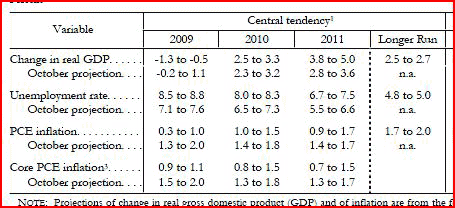

Thinking about the issues raised in my piece last week, it is worthwhile to spend more time on actual inflation and inflation expectations within the context of the Fed’s policy of “credit easing.” Consider as a starting point the recent work by John Williamson at the San Francisco Fed who concludes:

This analysis highlights the central roles of economic slack and inflation expectations in the risk of deflation over the next several years. The evidence indicates that a substantial increase in slack can lead to deflation, but the depth and duration of the deflation depends on how well anchored inflation expectations are. Two policy implications can be drawn from this and other research on deflation. First, a central bank should take appropriate actions to stem the emergence of substantial slack in the economy and thereby reduce the risk of deflation. Second, it should clearly communicate its commitment to low positive rates of inflation. An example of such communication is the Federal Open Market Committee’s recently released long-run inflation forecasts. Such words, backed by appropriate actions, reinforce the anchoring of inflation expectations and reduce the chances of a deflationary spiral.

Conventional wisdom of the Fed’s policy describes quantitative easing as an effort to boost inflation expectations. This flows from the fact that the Fed Funds rates is at zero, therefore further decrease in the real rate can only be achieved by boosting inflation expectations. To me, however, the Fed has not committed to a program of raising inflation expectations. Instead, they are reiterating their existing commitment to a low, stable rate of inflation. Consider the most recent FOMC statement:

In light of increasing economic slack here and abroad, the Committee expects that inflation will remain subdued. Moreover, the Committee sees some risk that inflation could persist for a time below rates that best foster economic growth and price stability in the longer term.

In these circumstances, the Federal Reserve will employ all available tools to promote economic recovery and to preserve price stability.

There is some risk of suboptimal inflation rates, and therefore they will conduct policy conducive to raising inflation. But what rate of inflation? Is there any sense that the Fed is actually trying to change the expectations of their policy goals? Not in the minutes from the previous meeting, where they clearly define their expectations for inflation under appropriate monetary policy:

It would appear that the Fed is attempting to anchor inflationary expectations in a range consistent with conventional understanding of the Fed’s implicit inflation target of 1.7-2% (note that this implied the Fed see a floor on the real rate of -2%). If actual inflation is substantially less than this target, the Fed would be expected to ease policy accordingly. Otherwise, they would be accommodating declining inflation, which would challenge their commitment to their target. Their commitment to stable inflation would not be credible, and expectations would become unanchored in a deflationary direction.

Consider this commitment further via the Fed minutes:

Many participants noted some risk of a protracted period of excessively low inflation, especially if inflation expectations were to move down in response to lower actual inflation and increasing economic slack, and a few even saw some risk of deflation. Several others, however, anticipated that longer-run inflation expectations would remain well anchored, supported in part by the Federal Reserve’s aggressive expansion of its balance sheet and the resulting growth of the monetary base, and therefore thought it unlikely that inflation would decline below levels they saw as consistent with the dual goals of price stability and maximum employment.

Yes, there is a risk of deflation, so policymakers will expand the balance sheet accordingly to prove their commitment to low and stable inflation. Notice the theme – to maintain credibility, the monetary authority needs to behave consistent with their commitments. In this framework, the Fed had little other choice but to expand the balance sheet aggressively if they want to avoid expectations of deflation.

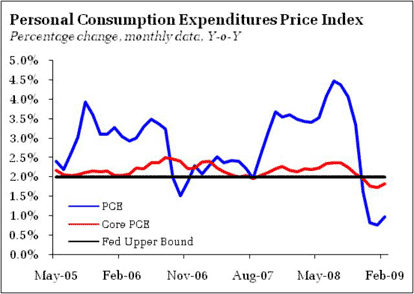

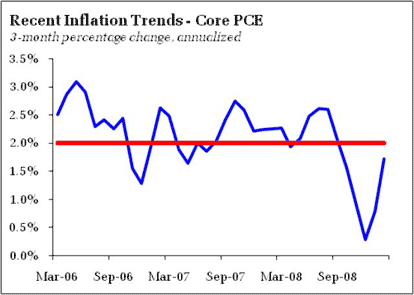

Has the Fed been successful in anchoring expectations? Deflation concerns stem in part from the sharp drop in year-over-year inflation:

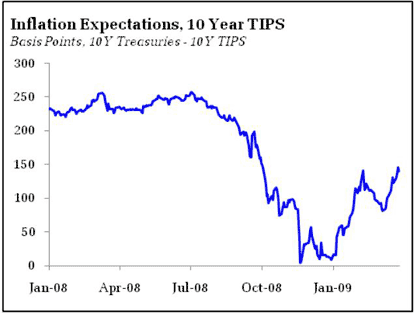

The TIPS market, however, is now waiving off deflation concerns:

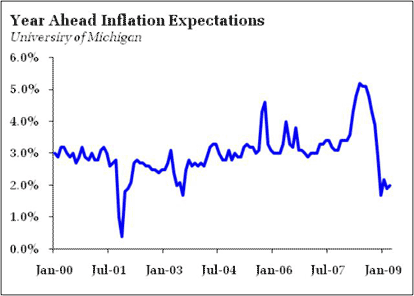

In the context of the above discussion, the widening of the 10 TIPS breakeven looks consistent with a successful Fed policy to anchor expectations, which, again, differs from changing where that anchor lays. Likewise, the public perception does not appear to be tilted toward deflation:

Interestingly, the public’s near term inflation expectation is well above the drop experienced in the wake of 9/11. It is worth noting that the rapid disinflation of late last year has somewhat reversed in recent months:

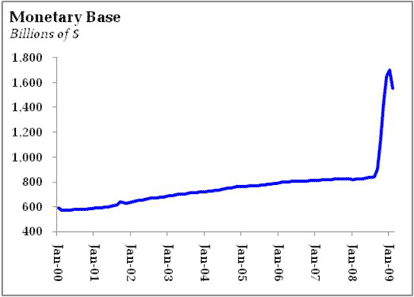

It is also worth thinking about what would have happened if the Fed did not do this:

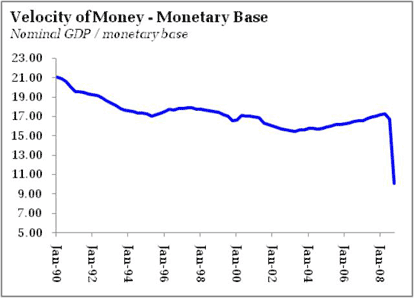

Given that the velocity of the monetary base did this:

Now, credibility cuts both ways. The above analysis suggests that the Fed has so far staved off deflationary expectations by acting in a manner consistent with its inflation target. But suppose inflation rises above that target – perhaps velocity explodes, so that inflation rises even if output remains at suboptimal levels (something akin to Johnson and Kwak’s emerging market scenario). Then the Fed would need to maintain its commitment to the inflation target by contracting the balance sheet. From the minutes:

Moreover, some noted a risk that expected inflation might actually increase to an undesirably high level if the public does not understand that the Federal Reserve’s liquidity facilities will be wound down and its balance sheet will shrink as economic and financial conditions improve.

Policymakers are already considering the removal of their liquidity injections. In other words, they have not committed to a permanent increase in the money supply. Indeed, I believe this is why Fed Chairman Ben Bernanke describes policy as credit easing not quantitative easing. The latter implies permanence. From the minutes:

Several participants indicated that they thought the FOMC should explore establishing quantitative guidelines or targets for a monetary aggregate, perhaps the growth rate of the monetary base or M2; in their view such guidelines would provide useful information to the public and help anchor inflation expectations. Others were skeptical that a single quantitative measure could adequately convey the Federal Reserve’s current approach to monetary policy because the stimulative effect of the Federal Reserve’s liquidity-providing and asset-purchase programs depends not only on the scale but also on the mix of lending programs and securities purchases. In addition, a few participants noted that the sizes of some Federal Reserve liquidity programs are determined by banks’ and market participants’ need to use those programs and thus will tend to increase when financial conditions worsen and shrink when financial conditions improve; the size and composition of the Federal Reserve’s balance sheet needs to be able to adjust in response.

Again, the Fed has committed to nothing other than to maintain a balance sheet consistent with well-anchored inflation expectations. Note too that this does not imply a complete reversal of the balance sheet expansion; if the velocity of money remains low, then some part of the balance sheet expansion can be permanent and not lead to an increase in expectations of the Fed’s inflation target.

The risk is that the Fed commits a policy error by not allowing the balance sheet to contract sufficiently to offset any increase in inflationary pressures. There is a reasonable risk of such an outcome. Consider the first half of 2008, when the Fed continued to ease policy even as inflation, and inflation expectations, was rising dramatically. Had that situation continued, the Fed would have been accommodating increased inflation expectations, thereby threatening their perceived commitment to low and stable inflation. Instead, the Fed got “lucky” and the global economy collapsed, sending inflation downward as commodity prices collapsed. Would the Fed get so “lucky” again?

I think, however, the more likely risk is that the Fed’s independence is compromised and they politically cannot shrink the balance sheet in a timely fashion. As I have argued, policymakers understand this risk, and are vociferously reiterating their independence. This too helps keep expectations in check.

Another risk is that policymakers deliberately attempt to reset the inflation target to a higher rate. This may become the policy choice if policymakers believe they need to reduce real rates below the -2% floor implied by the current target (effectively, the Fed chooses the inflation solution to the debt overhang). Resetting the inflation target, I believe, would amount to a commitment by the Fed to a permanent increase in the money supply growth rate. But I doubt it would be easy – how could a new target be credible if the Fed abandons the current target? An attempt to set a new target, I fear, would lead inflation expectations to become fully unanchored. I think the Fed knows this; hence, they avoid the loaded term quantitative easing in favor of credit easing.

Bottom line: The conduct of Fed policy is consistent with a commitment to the existing inflation target. The increase in the monetary base, in this framework, was necessary to prevent expecatations from shifting in the direction of deflation. But credibility works both ways; they need to remain ready to withdraw liquidity should inflation pressures emerge. The repeated claims that the expansion of the balance sheet is not permament is consistent with credibly committing to the existing target. There remains, however, plenty of room for policy error, and not to mention the now omnipresent fear that the Fed has sacrificed its independence.

Leave a Reply