Tell me if you think this story sounds familiar.

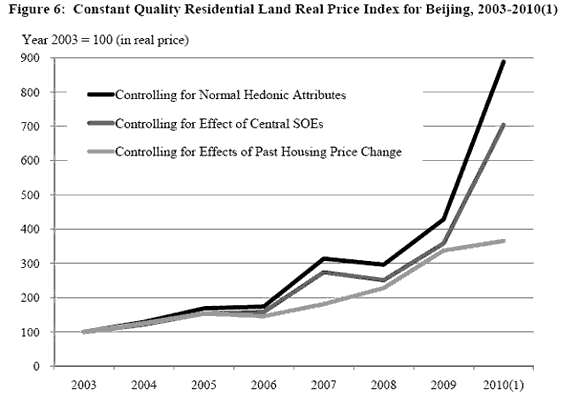

A new NBER working paper by Jing Wu, Joseph Gyourko, and Yongheng Deng (also discussed by Joseph Cotterill and Tyler Cowen), used recorded prices for 300 residential land auctions in Beijing to develop the first constant-quality land-price series for a Chinese market. The study concludes that inflation-adjusted constant-quality land prices have increased by nearly 800% since 2003:Q1, with half that increase occurring over the past two years.

Source: Wu, Gyourko, and Deng (2010)

Some observers had dismissed the apparent parallels between the Chinese real estate bubble and that in the United States based on institutional differences in the details of loan financing between the two countries. For example, Michael Kleist wrote last March:

Certainly there isn’t a mortgage credit-related bubble. The majority of homes in China are purchased with down payments between 30-40%, which is required by the banks, and nearly 25% of homes are purchased with all cash. Only those qualifying for low-cost housing can purchase a home with a minimum down payment as low as 20%. For this reason foreclosures in China are practically nonexistent.

But Wu, Gyourko, and Deng provide this interesting additional detail:

There also is a statistically and economically strong positive correlation between land auction price in Beijing and the winning bidder being a state-owned enterprise (SOE) associated with the central government. All else constant, prices are about 27% higher when a central government-owned SOE wins a land auction, so these entities appear to be playing a meaningful role in rising land values in Beijing….

If these particular developers are superior investors and are able to buy unobservedly high quality sites, then part of this effect could be a proxy for quality. We certainly do not claim that our hedonic controls are perfect. However, in other regressions not reported here, we also find that Central SOE developers pay high prices relative to the values of nearby housing unit sales prices. That suggests these particular buyers simply pay more and that this does not merely reflect omitted quality effects. Moral hazard arising from these entities believing they are too important to fail, combined with their access to low cost capital from state-owned banks, also could help explain their bidding behavior.

Mike Shedlock also relays several troubling anecdotal reports about where the money for down payments comes from. Here’s one of the more benign accounts that he quotes:

There are circles in neighborhoods, or churches, community groups that are kind of like informal credit unions. People pool money into a large sum and then bid for its use month by month. 5% a month is the typical rate of interest….

Parents lend to their children to buy their condo with the understanding it will be repaid or they will come to live in their old age under that roof. Almost no one has the 20 to 30% down to buy a place. The down payment is typically borrowed at terrible interest or comes from a “marriage gift” which had its origin in borrowed funds, not from savings….

A collapse of the bubble could cost lots of folks their life savings. This makes the financial aspect of Chinese society much more fragile than it appears on the surface. There is a lot of interconnected personal debt below radar.

Popular opinion remains that the current worries in financial markets began in Europe. But as I’ve noted previously the Chinese stock market decline began before that in Europe and coincided with measures in China to curb property speculation. As of the moment, the equity decline in China substantially exceeds that in Europe.

Blue: SSE Shanghai Stock Exchange composite stock price index. Red: IEV S&P Europe 350 stock price index. Source: Google Finance

Leave a Reply