Team Macro Man fully expected after a 6 day, 9% rally that equities are due a correction, yet despite the best efforts of Mayfair and Greenwich, seemed supported on dips, only managing to put in a Doji despite the FOMC mentioning the dreaded “D” word. With the Aussie pushing the highs post-China reval level, TMM has been forced to admit that actually, whilst equities & bond yields made new lows (was it really just a week ago…?), neither the metals space (especially Copper) or risky FX markets did. This is despite the fact that at least 90% of TMM’s emails and IBs seem to, even now, still be resolutely bearish in their commentary, or attempting to suggest that punters are being sucked into buying at the highs. Now TMM is of the opinion that much of the past week (as mentioned in yesterday’s post) has simply been position-reduction (either forced, or voluntary), but can’t help be reminded of the last time markets that were fretting about a double-dip and got sucked into a bear-trap which was subsequently followed by a very aggressive multi-month rally. Team Macro Man remembers it well as they were amongst those that were the wrong way around that time…

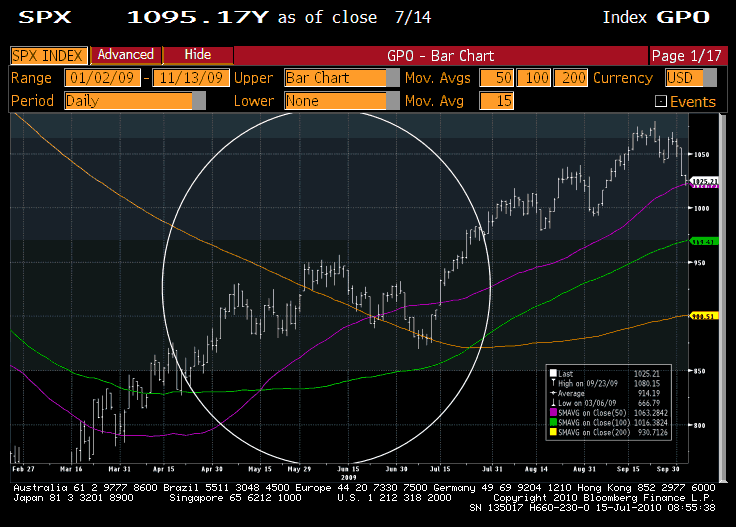

(click to enlarge)

So what was the set-up in July 2009?

- A Head and Shoulders pattern had recently completed.

- The S&P500 had broken below its 200day moving average.

- Double-dip fears related to the inevitable multi-year de-leveraging of household balance sheets and scepticism about the existence of a recovery and credibility of the stress tests were widespread.

- There was a large dichotomy between traders and analysts with respect to whether earnings and guidance would be good or not.

Sound familiar? As we now know, traders were wrong and analysts were right, with a blow-out earnings season powering equities higher with little correction, forcing players to chase. Although we have only had a handful of earnings releases, there have been some from important companies (Alcoa, Intel & Novartis) that have both beaten strongly as well as raising guidance, and this has forced many to cover their shorts. As TMM’s wise friend RightField commented yesterday, before players will truly embrace such an analogue, they will need to see some of the earnings of the financials given the poor conditions in the housing market and political sensitivity with respect to the FinReg Bill (no point showing great earnings if it will spark more populism in the yet-to-be-passed Bill). But if earnings and guidance continue to print well then deflation/double-dip concerns are likely to dissipate.

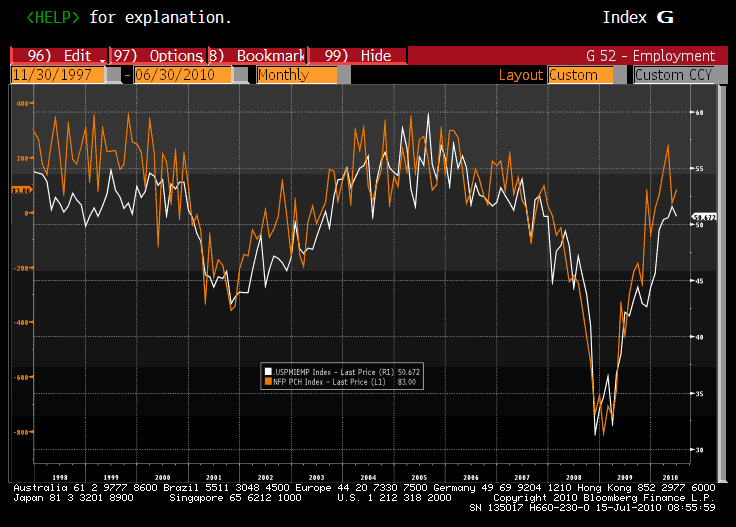

Of course, TMM is not suggesting that the situation is exactly the same. ISM, for example, was rising and the inventory build was just beginning to get underway – this time, it is falling and inventories have already been built. But as at least some offset to that, equities are cheaper relative to earnings expectations now (at 13.5x current year earnings) than they were in July 2009 (16x current year earnings) and a falling ISM is not the same as a double-dips (something that is rarer than a dog that speaks Norwegian). And TMM wonders if rather than weakening, Payrolls have merely been coming into line with other measures of the labour market – the chart below shows private payrolls (orange line) vs. the GDP-weighted Employment components from the ISM and non-manufacturing ISM reports (white line). Private payrolls clearly outperformed the survey measures for a while and have now come back into line with them. And even the most entrenched bears would struggle to argue that that chart does not look like a “V” – it is just that the fall was so sharp and over a larger period of time than in prior recessions, and thus so must be the recovery.

(click to enlarge)

But enough cheerleading. The above analogue is dependent upon financial earnings, so today’s numbers from JPM are important in that respect, if they disappoint then TMM expect a Soothsayer turn for the worse on Monday. Indeed, TMM are sympathetic to the view that should core-CPI surprise the downside tomorrow that deflationary fears will reach a new height. As mentioned yesterday, TMM has a long-held theory about market turns around the 16th/18th July, but wonders if we might have already seen it? Isn’t it starting to feel a bit like July 2009…?

Leave a Reply