Finisar Corporation (FNSR) is expected to drastically increase earnings this year and you wont be overpaying for those nice growth rates either.

Company Description

Finisar makes fiber optic and network test systems for high-speed communication. The voice, video and data technology is used in networking, storage, wireless and cable TV applications.

Record-Setting Quarter

On Jun 10 Finisar released its fourth-quarter results that showed 75% jump in revenues, to just under $190 million. The company is also running more efficiently, with an operating margin of 6.9% for the quarter, up from a 10% deficit one year ago.

Net income for the period came in at $14.1 million, more than doubling the previous quarter, and up from a substantial loss one year ago. Earnings per share broke down to 21 cents, beating the Zacks Consensus Estimate by 7 cents.

Estimates Jump

Following the earnings release, the full-year Zacks Consensus Estimate for fiscal 2011 jumped a dime to 78 cents. Forecasts for next year are up 17 cents on average, to 97 cents.

Given earnings of just 14 cents last year, the annual growth rates for Finisar are 460% and 24%, respectively. The company has a good chance of hitting those levels, given that it has met or beat expectations in 5 of the past 6 quarters.

Valuations

Finisar is trading with fairly solid valuations at this level. The forward P/E is about 18 times. While not great, it is in line with its peers.

The stock currently has a PEG ratio just under 1.0 as well, so the growth rate is coming at a slight discount. Finisar’s price-to-sales ratio is a nice 0.6 times.

Additionally, Finisar operates with an ROE of just over 13% while its industry averages a 5% loss. The profit margin registers at 2.2%, compared to the -20.4% that its peers average.

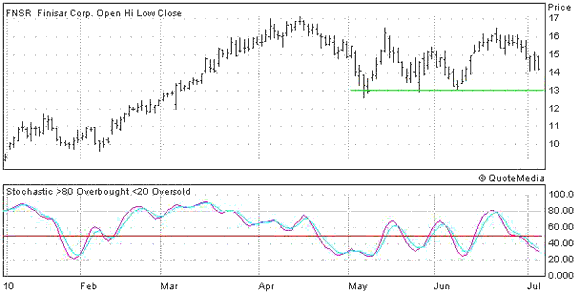

The Chart

Shares of FNSR have done a good job of maintaining this level. Just as the stock approaches about $13 per share the support kicks in as the stochastic nears “oversold” territory.

FINISAR CORP (FNSR): Free Stock Analysis Report

Zacks Investment Research

Leave a Reply