What do we know about the spread of protectionism during the Great Depression and what are the implications for today’s crisis? This column says the lesson is that countries should coordinate their fiscal and monetary measures. If some do and some don’t, the trade policy consequences could once again be most unfortunate.

The Great Depression of the 1930s was marked by a severe outbreak of protectionism. Many fear that, unless policymakers are on guard, protectionist pressures could once again spin out of control. What do we know about the spread of protectionism then, and what are the implications for today?

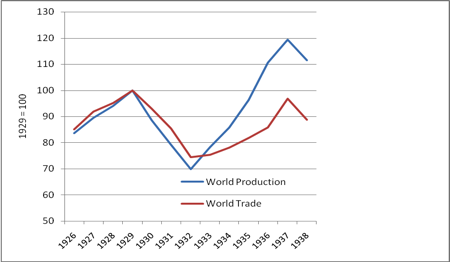

While many aspects of the Great Depression continue to be debated, there is all-but-universal agreement that the adoption of restrictive trade policies was destructive and counterproductive and that similarly succumbing to protectionism in our current slump should be avoided at all cost. Lacking other instruments with which to support economic activity, governments erected tariff and nontariff barriers to trade in a desperate effort to direct spending to merchandise produced at home rather than abroad. But with other governments responding in kind, the distribution of demand across countries remained unchanged at the end of this round of global tariff hikes. The main effect was to destroy trade which, despite the economic recovery in most countries after 1933, failed to reach its 1929 peak, as measured by volume, by the end of the decade (Figure 1). The benefits of comparative advantage were lost. Recrimination over beggar-thy-neighbour trade policies made it more difficult to agree on other measures to halt the slump.

Figure 1. World trade and production, 1926-1938

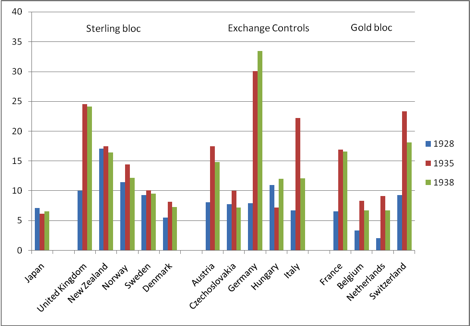

The impression one gleans from both contemporary and modern accounts is that trade policy was thrown into complete chaos, with every country scrambling to impose higher barriers. But, in fact, this was not exactly the case (Eichengreen and Irwin, forthcoming). Although recourse to trade restrictions was widespread, there was considerable variation in how far countries moved in this direction. Figure 2 illustrates this for tariffs. Tariff rates rose sharply in some countries but not others. The history of the 1930s would have been very different had other countries responded in the manner of, say, Denmark, Sweden and Japan. It is important to understand why they did not.

Figure 2. Average tariff on imports, 1928-1938, percentage

The answer, in a nutshell, is the exchange rate regime and the policies associated with it. Countries that remained on the gold standard, keeping their currencies fixed against gold, were more inclined to impose trade restrictions. With other countries devaluing and gaining competitiveness at their expense, they adopted restrictive policies to strengthen the balance of payments and fend off gold losses. Lacking other instruments with which to address the deepening slump, they used tariffs and similar measures to shift demand toward domestic production and thereby stem the rise in unemployment.

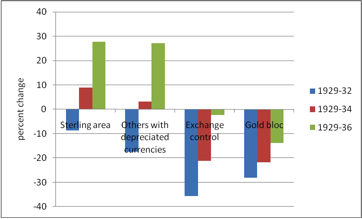

In contrast, countries abandoning the gold standard and allowing their currencies to depreciate saw their balances of payments strengthen. They gained gold rather than losing it. As importantly, they now had other instruments with which to address the unemployment problem. Cutting the currency loose from gold freed up monetary policy. Without a gold parity to defend, interest rates could be cut, and central banks No longer bound by the gold standard rules could act as lenders of last resort. They now possessed other tools with which to ameliorate the Depression. These worked, as shown in Figure 3. As a result, governments were not forced to resort to trade protection.

Figure 3. Change in industrial production, by country group

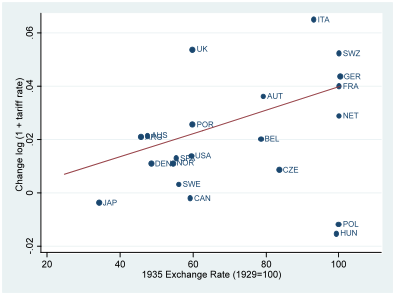

This relationship is quite general, as we show in Figure 4. It also carries over to non-tariff barriers to trade such as exchange controls and import quotas.

Figure 4. Exchange rate depreciation and the change in import tariffs, 1929-1935

This finding has important implications for policy makers responding to the Great Recession of 2009. The message for today would appear to be “to avoid protectionism, stimulate.” But how? In the 1930s, stimulus meant monetary stimulus. The case for fiscal stimulus was neither well understood nor generally accepted. Monetary stimulus benefited the initiating country but had a negative impact on its trading partners, as shown by Eichengreen and Sachs (1985). The positive impact on its neighbours of the faster growth induced by the shift to “cheap money” was dominated by the negative impact of the tendency for its currency to depreciate when it cut interest rates. Thus, stimulus in one country increased the pressure for its neighbours to respond in protectionist fashion.

Today the problem is different because the policy instruments are different. In addition to monetary stimulus, countries are applying fiscal stimulus to counter the Great Recession. Fiscal stimulus in one country benefits its neighbours as well. The direct impact through faster growth and more import demand is positive, while the indirect impact via upward pressure on world interest rates that crowd out investment at home and abroad is negligible under current conditions. When a country applies fiscal stimulus, other countries are able to export more to it, so they have no reason to respond in a protectionist fashion.

The problem, to the contrary, is that the country applying the stimulus worries that benefits will spill out to its free-riding neighbours. Fiscal stimulus is not costless – it means incurring public debt that will have to be serviced by the children and grandchildren of the citizens of the country initiating the policy. Insofar as more spending includes more spending on imports, there is the temptation for that country to resort to “Buy America” provisions and their foreign equivalents. The protectionist danger is still there, in other words but, insofar as the policy response to this slump is fiscal rather than just monetary, it is the active country, not the passive one, that is subject to the temptation.

But if the details of the problem are different, the solution is the same. Now, as in the 1930s, countries need to coordinate their fiscal and monetary measures. If some do and some don’t, the trade policy consequences could again be most unfortunate.

![]()

Leave a Reply