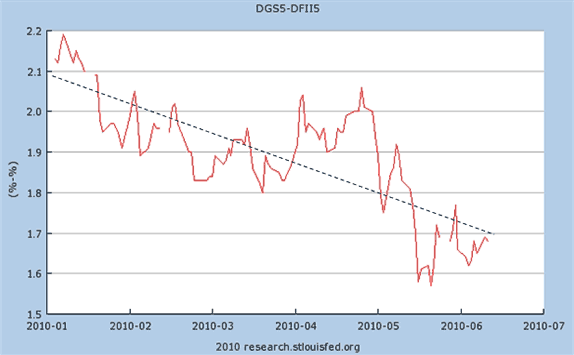

Take a look at the figure below. This figure shows the difference between the nominal interest rate on the 5-year Treasury and the real interest rate on the 5-year Treasury inflation protected security (TIPS). This difference amounts to the markets expectation of future inflation. This figure, which goes through June 15, 2010, reveals a clear downward trend in inflation expectations over the first half of this year.

Source: Fred Database

I would like to attribute this decline to productivity growth, but it too appears to be coming down. That leaves us with one troubling possibility: the market is expecting aggregate demand to decline going forward. And unless the Fed acts to stabilize this expected fall in total spending it will effectively amount to a tightening of monetary policy. Obviously, the last thing the U.S. economy needs is a tightening of policy during an anemic recovery. I hope Ben Bernanke and the Fed are taking notice.

P.S. This is another instance where a NGDP futures market would be immensely helpful. More generally, they would make monetary policy a whole lot easier and effective as explained here. I really wish our leaders would push NGDP futures as part of the package of economic reforms.

Leave a Reply