Reports out of Europe say a huge scramble for gold coins is on. Dealers have run out of inventory. This is a microcosm of the Creditanstalt Problem: at some point bailouts no longer work, and creditors run for the exits taking the rescue funds with them. As a senior PIMCO manager said: “the risk is that investors are using the ECB as a vehicle to exit their positions.” Well, duh! Amazing it would happen at the same time period in May as it did in May 1931.

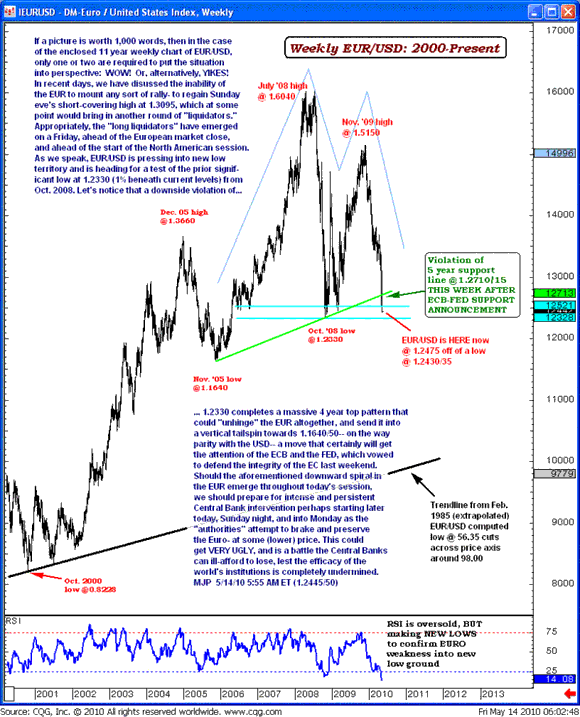

The Euro hit the next support level at $1.233, the Oct08 level, and after going slightly lower to $1.223 bounced around the time the ECB announced concrete steps to sterilize their recent purchase of PIIGs bonds (in order to maintain the supply of Euros as constant). This may alleviate inflation concerns and spark a short-term recovery. If turns down again and breaks below that level, the next range is $1.164 – 1.18, which provided support back in 2003-05. Chart and analysis from MP Trader (via SlopeofHope) below.

Goldman Sachs (GS) in contrast has a target of $1.35. They think the Eurozone will grow about as fast as the US with Germany making up for austerity among the much smaller PIIGS, and hence think rates settle back a bit. More on that in a later post. If the ECB intervenes strongly enough, a huge short squeeze could drive the Euro back above $1.35 quickly, and it might settle back down there.

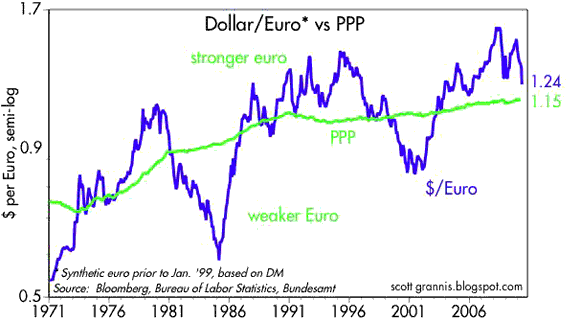

Calafia Beach Pundit points to purchasing power parity (PPP) levels, which are $1.15 in the Euro and $1.42 in the Pound. Both these currencies might get there, fast, and overshoot to the downside. The most over-valued currencies, however, may stay that way a while longer:

- AUD at 89c is way above parity at 68c, giving it a lot of room room to drop

- Yen at 121 per $1 also has a ways to drop from its current 93

Those two currencies are way above PPP due to the carry trade. The Yen is a major carry-trade currency, and the AUD is a major beneficiary of the carry trade in both Yen and USD. Per my recent post on the AUD, if the carry-trade unwinds due to the crash, both have a lot of room to drop vs the USD. Of course, any rate increase in Japan puts their country into a deep hole, given that interest on the debt (at very low rates) can hardily be covered by taxes.

Leave a Reply