As we wait for the results of the Italian election, Europe is heading for yet another period of uncertainty. Governments in key countries (Italy, Spain, Greece, France,…) do not have the support to continue the path that has been followed so far but there is still no real alternative and a strong sense of complacency: we will continue the same policies that we have followed so far.

According to the European commission recent forecasts, the Euro area will see negative growth rates again in 2013 and growth rates as low as 1.4 in 2014. This means an average growth of 0.16% in the period 2012-2014, assuming we do not end up revising downwards our views on 2014 – which is very likely. And this comes after Europe has gone through its worst recorded recession during the 2008-2010 years.

This is now worse than a double-dip (great) recession. What is really frustrating (maybe we should call it depressing, to match the economic situation) is the complacency with which some European politicians look at what is happening. When Olli Rehn (EU commissioner for economic and monetary affairs) commented on these negative forecasts produced by the EU commission, he called them disappointing but then he just said that current policies are finally paying off. The introduction letter to those forecasts, produce by Marco Buti, the Director General responsible for the forecasts, talks about several factors that are contributing to weak growth: the negative feedback between public finances, banks and the weak macroeconomy, lack of credit growth, uncertainty about policies,… These are all external factors (austerity is not even mentioned as a possible factor), so the best we can do is to continue the policy agenda “to ensure the sustainability of public finances”. There is no learning here, it does not matter how strong the facts are (I will not present again the facts here, see Krugman or De Grauwe for a recent analysis and a reaction to these forecasts).

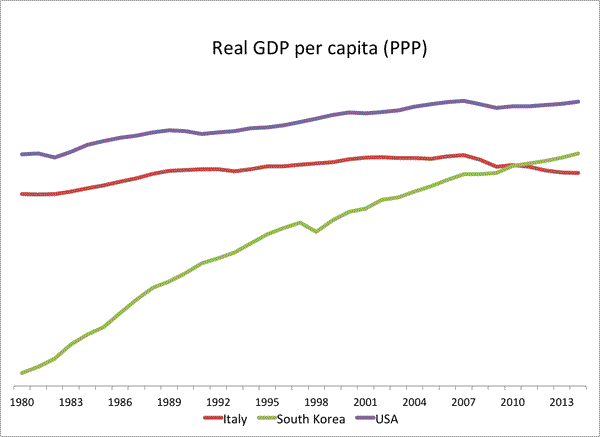

But let me look at some (depressing) data from Italy, where election results are expected by the end of the day. Below is the evolution of the Italian economy compared to the US and South Korea since 1980. Data is GDP per capita (in logs) from the IMF World Economic Outlook, including their forecast for 2013 and 2014.

After the Italian “miracle” of the 1960s and 1970s where Italy was growing fast and converging towards the other rich countries, the economy stagnated in the 80s and then started falling apart in the years that follow. Since 1990, not only Italy has stopped converging towards the US levels, it is now drifting down and away from the US level. If this trend continues, Italy will follow the path of Argentina in the 20th century when it went from one of the richest countries in the world to a middle-income country. As a comparison we see how South Korea continues its path of convergence towards the US and has recently passed Italy in terms of GDP per capita.

We talk a lot about the lost decade for Japan, but if there is an advanced country where the label lost decade applies is Italy during the last 10 (or 15) years. But, of course, we can always be optimistic (as Olli Rehn seems to be is), Italy still exists as a country, it is still a member of the Euro area and bond yields are not as high as the ones in Greece – although all this can change in a few hours if the election results end up being a (bad) surprise!

Europe can and should do much better than zero growth over a decade. If this is not understood by political leaders then the downward drift that some countries started 10 or 15 years ago will continue or even accelerate and this might drag all the other European countries with them.

Leave a Reply