How will the European crisis feed into the US outlook? I clearly recall JP Morgan making a recession call in the wake of the Asian Financial crisis, predicting a US recession on the back of a drop in net exports. While a drop in net exports did occur, domestic growth more than absorbed the impact. The US recession was delayed until the impact of tighter monetary policy, higher energy prices, and the popping of the tech bubble all came home.

I can see a similar pattern of events evolving now.

First off, I think it unlikely that an export demand shock alone is sufficient to push the US economy back into recession. Menzie Chinn tackled this issue back in 2007, arguing at the time it was unlikely a rise in exports would stave off a recession. The reverse logic holds as well; US recessions look to be driven by sharp declines in domestic absorption, not exports.

That is not to say that slowing exports would not crimp US growth. The rising Dollar not only stresses US exports to Europe, but China as well. As Calculated Risk notes, European exporters are now more competitive in China compared to their US counterparts. Moreover, the falling Euro may delay any eventual loosening of Chinese currency policy, as policymakers fret about the effects of one falling currency, let alone two.

Now, it is perfectly reasonable to be concerned about the implications of falling net exports for growth given the supposed fragility of the US recovery. The Wall Street Journal reports the Goldman Sachs analysis:

Estimates of how much the government’s spending is actually stimulating growth vary wildly — some economists contend it has no net effect at all. But if you believe the economists at Goldman Sachs, who have spent a lot of time poring over the details, the effect is quite significant: about two percentage points of annualized growth in both this quarter and the last. Indeed, if one subtracts that stimulus effect and the boost from changing inventories — also a temporary factor — there’s been no recovery at all. Growth in the first and second quarters of 2010 would be zero.

One can contrast this with a more optimistic assessment from Justin Weidner and John Williams at the San Francisco Federal Reserve Bank:

In the past, large output gaps, rapid growth of potential output, and real interest rates well below the natural interest rate have contributed to rapid V-shaped recoveries. These factors were much more muted in the recessions of 1990–91 and 2001, leading to U-shaped recoveries. Now they point to a moderate pace for the current recovery, somewhere between the U and V shapes of the past.

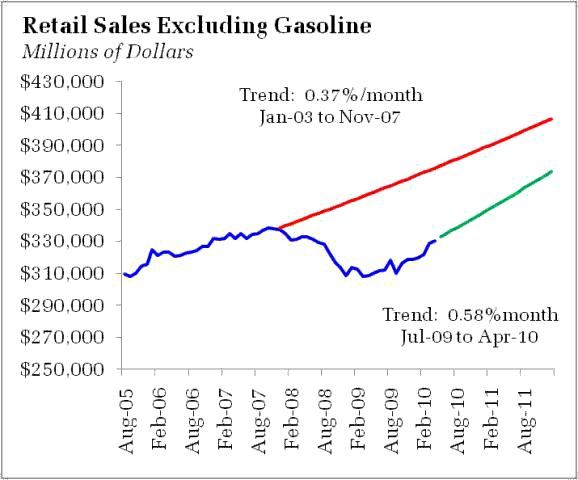

Yes, per usual, two economists, three opinions. In any event, one would have to consider the positive impact of the Greek crisis against any trade drag. And yes, there are positive implications. First, the weaker Euro has taken a bite out of oil prices, which fell back below $70 today. Make no mistake – keeping a lid on oil prices offers continued support for US consumers. And while we can all dream of a more balanced economy less dependent on household spending, for now it remains the best game in town. Although Phil Izzo at the Wall Street Journal tried to throw some cold water on the details, the overall trend in retail sales continue to look solid:

Consumers have a wind at their backs, unbelievably, and further job growth will only speed them further. Likewise, the rush to Treasuries is keeping a lid on US interest rates. And this is coming on the back of already surging demand for US assets. From Bloomberg:

Global demand for long-term U.S. financial assets strengthened in March to a record as investors from China to the U.K. purchased the most Treasuries since November, a Treasury Department report said.

Net buying of equities, notes and bonds totaled $140.5 billion in March, more than double economists’ projections, after net buying of $47.1 billion in February, the report released today in Washington showed. Including short-term securities such as stock swaps, investors abroad purchased a net $10.5 billion, compared with net buying of $9.7 billion the previous month.

Signs of a sustained economic recovery, including a rebound in earnings and stock prices, may increase demand for U.S. investments as concerns mount about the sustainability of government debt in Europe, economists said. The world’s largest economy has expanded for three consecutive quarters and added 573,000 jobs in the first four months of the year.

Add a lid on interest rates via a steady surge of capital flows to sustained job growth, and the odds of sustainable recovery look better every day. Moreover, we are still in a sweet spot with regards to monetary policy. The Fed was not inclined to tighten policy this year, expecting continued downward pressure on inflation via a persistent unemployment gap. The European crisis only adds to the willingness of monetary policymakers to hold tight. No, in the near term, the Fed is not likely to derail the recovery.

Of course, the European financial crisis remains a bogeyman via the possibility of financial contagion. Will the US banking system once again come under assault? On this point I think we can pull out the “too big too fail” card – images of the most recent crisis remain vivid in policymakers’ minds. They would likely swamp the financial system with cash if the crisis threatened to spread to the US, quickly pulling out all the tools they just put back on the shelf. And note that the inflows of capital helped the US whether the Asian Financial Crisis despite a few harrowing days on Wall Street (like that little thing called LTCM).

Bottom Line: The European crisis, by keeping US interest rates in check and oil prices low, may do more to help the US recovery than hurt it. In the process, however, we would expect the flip side of the resulting capital inflows into the US to emerge – namely, a rising external imbalance. Arguably, this simply shifts the ultimate adjustment to sometime in the future. Again.

Leave a Reply